The Fed’s

Massive Credit Market Intervention Fuels Junk Bond Mania

By the

Curmudgeon

Introduction:

In our quest to chronicle the

extent of the unprecedented mania and speculative excesses in financial markets

(also crypto-currencies, art, real estate, etc.) we focus today on the “high

yield” (junk) bond market. This post

complements yesterday’s Curmudgeon on the super-hot market for IPOs.

During the 1st

quarter of 2021, U.S. companies raised a record $140 billion in the junk

bond market, according to data from Refinitiv. That beat the previous record

set during the 2nd quarter last year when companies scrambled to

issue debt in a bid to raise cash during the start of the coronavirus pandemic.

The three biggest issuance quarters in history have been set in the past year

with the biggest of all in this year’s 1st quarter.

Indeed, the Fed's

extraordinary intervention in the credit markets last Spring (including buying

junk bond ETFs) enabled investment-grade and non-investment-grade companies to

issue $1.9 trillion and $442 billion of debt, respectively, in 2020. They

already raised a fifth and a third of these amounts so far this year, according

to data compiled by Bloomberg.

And there’s a lot of corporate

debt outstanding! Average total

debt, weighted by market capitalization among large and small companies that

make up the Russell 3000 Index, probably is a record $47 billion, or $4

billion more than a year ago and $16 billion greater than it was at the end of

2015, according to the latest corporate filings compiled by Bloomberg.

Let’s take a closer at high

yield debt and high yield credit spreads in this article.

The Bond Market Conundrum:

Investment grade bonds

(Barclays Global Aggregate Index) and 30-year Treasuries experienced significant

declines during the 1st quarter of 2021 of -4.5% and -15.66%,

respectively. It was the worst

performance for the 30-year T-bond on record (data going back to

1976). And that’s despite the Fed buying

$80 billion of Treasuries each month!

The junk bond market looked the other way as total returns were positive

in the quarter.

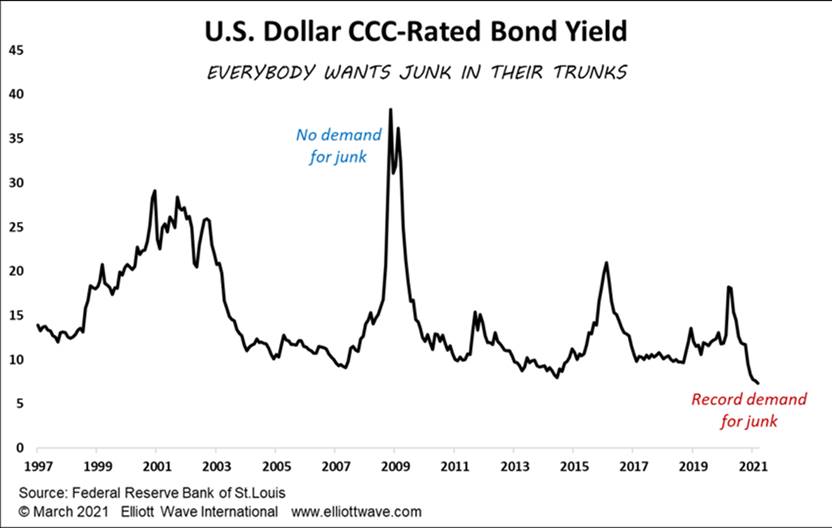

The lowest quality junk bonds

advanced at more than a double-digit annualized rate in the 1st

quarter. CCC rated high-yield bonds,

usually the lowest-graded bonds that trade, gained +3.58% year-to-date,

according to Bloomberg Barclays index total return data.

It’s been a flight to the

junkiest of junk! What me worry?

“The lower quality trade still

has some legs,” said Scott Kimball, co-head of U.S. fixed income at BMO Global

Asset Management. “Investors typically look to high-yield securities,

particularly CCCs, when yields are on the rise. Now, we see record positive

revisions for U.S. growth by economists being further boosted by record fiscal

stimulus expectations,” Kimball added.

Speculative “investor” demand

is helping CCC rated companies tap investors for plenty of cash. Here are a few examples:

· American

Airlines Group Inc. sold a total $6.5 billion of bonds in March at yields 20%

below the rates prevailing six months earlier, according to data compiled by

Bloomberg.

· Carnival

Corp, the Miami-based owner and operator of cruise ships to global vacation

destinations, sold $3.5 billion of bonds in February at an initial yield of

5.9% that subsequently declined to 5.2% as investors snapped up the offering.

Similar securities sold by the company earlier last year yielded 6.8%.

· Cetera

Financial Group Inc. is expected to complete a $400 million bond offering on

Thursday to help finance its acquisition of a Voya Financial Inc. financial

planning business. The deal is rated Caa2 by Moody’s Investors Service

and an equivalent CCC by S&P Global Ratings.

· Michaels

Cos. launched a $2.3 billion junk bond deal to fund its buyout by Apollo Global

Management, with investor calls through April 8.

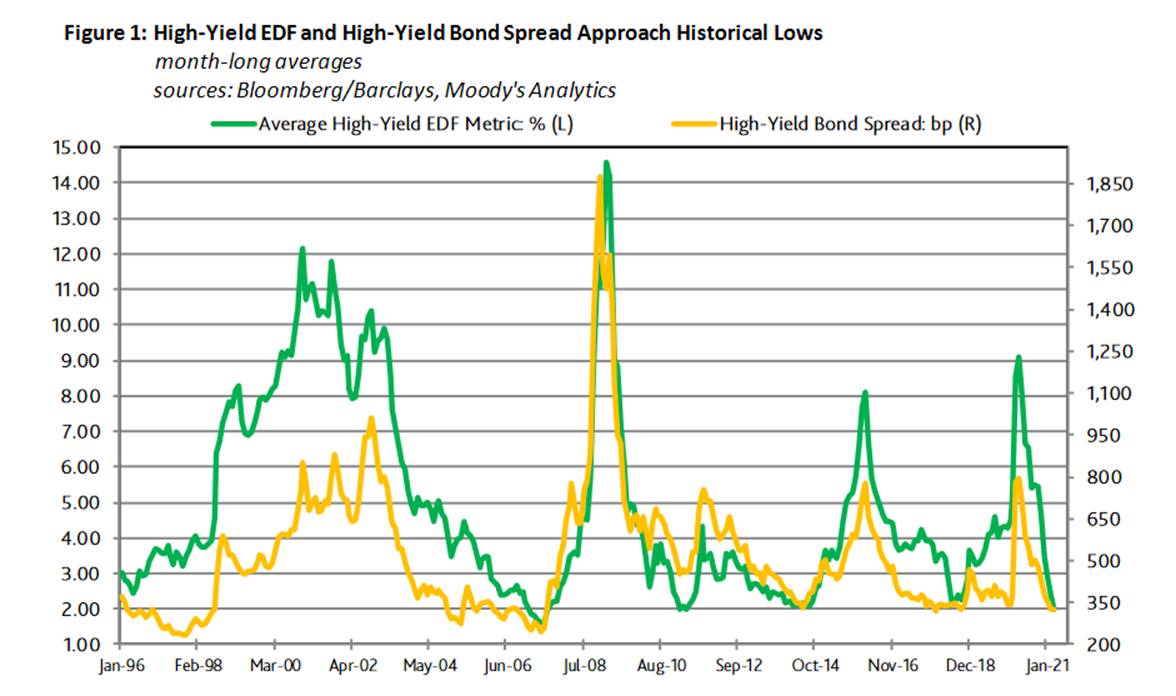

No Fear (or Risk) in High

Yield Credit Spreads:

As one would expect from the

junk bond out performance noted above, “high yield” credit spreads [over

the equivalent maturity Treasury bond] declined over the last three months to

historic lows, as per this chart:

Today, Moody’s John Lonski forecast that High-Yield Bond credit spreads would

decline to under 300 bps by the end of the week. That’s from around 684 bps one year ago!

The high-yield bond spread has

only been below 300 bps twice before – in 1997 and 2007. According to Moody’s, it rose from December

1997’s 277 bps to calendar-year averages of 389 bps for 1998, 485 bps for 1999

and 614 bps for 2000 as the perceived default risk rose accordingly.

The rise was even greater from

the July 1, 2007 low of 242 bps till the 2009 great recession peak around 1860

bps, as default percentages rose to over 13%. For more on the latter junk bond

meltdown please refer to this academic paper. For a more generic reference, check out The History of High-Yield Bond Meltdowns.

The riskiest entities are

being rewarded with 52% more credit upgrades than rating downgrades, as demand

for exchange-traded funds with high-yield junk bonds climbs to new highs. In

today’s credit markets, anyone raising money can do so on the easiest terms of

a lifetime.

Evidently, there are

widespread expectations of very rapid profit growth and low default

risk which have, in turn, narrowed corporate bond yield spreads.

Confidence in the Fed’s

continued suppression of Treasury bond yields has also been a factor.

Earnings Forecasts Rise along

with Junk Bond and Stock Prices:

The JP Morgan Forecast

Revision Index -- a gauge of how much economic forecasts change in a

quarter -- posted its biggest upward move in history this past quarter as

economists raced to upgrade their economic outlooks.

“Since last June, 10-year

Treasury yields have increased by 100 basis points (from 0.7% to 1.7%), leading

many investors to question the sustainability of these elevated stock multiples

(P/E ratios),” Credit Suisse strategist Jonathan Golub wrote in a note

last week to clients. “With (P/E) multiples stable, the market’s entire advance

can be explained by improving earnings.”

Investor appetite for the

riskier junk bonds is attributed partly to improved S&P ratings for 178

“high-yield” corporate debt securities compared to 117 downgrades. Moody’s also

issued about 2.3 upgrades for each downgrade, its highest ratio in the past

decade.

Conclusions:

Risk ON has never been

greater. In past columns, we’ve shown a

voracious appetite for IPOs (many of which have no earnings), penny

stocks & margin debt, SPACs,

bulletin

board inspired stocks (GameStop and AMC), and high flying mega

tech stocks.

Of course, the biggest

speculation of all is in Bitcoin, but Victor and I don’t comment

on it because we believe it has no intrinsic value. Yet it is the poster child

for the all-asset financial mania/ mega bubble that’s existed for years.

In this piece we’ve discussed

the mania in high yield bonds of the lowest quality and narrowing credit

spreads. Readers should ask themselves if it is worth the credit risk to buy a

“high yield” bond paying under 4%, especially with Treasury and higher grade

bond yields rising.

End Quotes:

“You tend to see these levels

(of low junk bond yields and narrow credit spreads) towards the end of a credit

cycle, and we’re clearly there,” said Guy LeBas,

chief fixed income strategist, Janney Montgomery Scott LLC. “We’re much

closer to the end than we are to the beginning.”

“The emergence of more

transmissible variants of the coronavirus is a reminder that even with vaccines

in hand, the evolving virus could have more unhappy surprises for the world

economy (and financial markets). If forecasts don’t pan out, there’s lots of

room for junk bonds to sell off. Companies that have borrowed heavily to

stay afloat during the pandemic could be dragged down by that debt,” excerpt of an article by Jack Pitcher, Carolina Gonzalez, and Paula

Seligson of Bloomberg.

………………………………………………………………………….

Stay calm, be well, hope for

the best, and till next time…...

The Curmudgeon

ajwdct@gmail.com

Follow

the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor

Sperandeo is a historian, economist and financial innovator who

has re-invented himself and the companies he's owned (since 1971) to profit in

the ever changing and arcane world of markets, economies and government

policies. Victor started his Wall Street

career in 1966 and began trading for a living in 1968. As President and CEO of

Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and

development platform, which is used to create innovative solutions for

different futures markets, risk parameters and other factors.

Copyright © 2021 by the Curmudgeon and

Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).