Fed in “Check” Status Now; Faces Imminent

“Checkmate” Day of Reckoning

By Victor

Sperandeo with the Curmudgeon

Introduction:

If the interaction between the U.S. economy and the Federal

Reserve Board (the Fed) were a game of chess, the economy just made a

recessionary move that said: “Check.” If the Jerome Powell led Fed ignores that

warning it will soon hear “Checkmate” from the economy!

U.S. Economy Snapshot:

Last week’s U.S. economic numbers were worse than expected

and considerably worse than the previous month’s reading. Here are a few:

·

Consumer confidence index

June: 98.7 vs 103.2 in May

·

Expected business conditions

were the weakest since 2009 while average expected inflation over the next year

rose +0.5% from May, to 8.0%—the highest reading in the survey’s 35-year

history.

·

Q1 Real Gross Domestic

Product revision: -1.6% vs -1.5% prior

·

PCE inflation (monthly) May:

0.6% vs 0.2% in April

·

Real disposable income May:

-0.1% vs 0.2% in April

·

Real consumer spending May:

-0.4% vs 0.3% in April (revised downward)

·

ISM manufacturing index June:

53.0% vs 56.1% in May (lowest reading since 2020) -see discussion and graph

below.

·

Construction spending

May: -0.1% vs 0.8% in April

On Friday, the Atlanta Fed’s GDP Now projection for the 2nd quarter

2022 (just ended) was reduced to -2.1%. If that projection is anywhere near accurate,

then the U.S. will have experienced two consecutive quarters with negative real

GDP.

Note: The working

definition of a recession is two consecutive quarters of negative economic

growth as measured by real GDP (although he National Bureau of Economic Research (NBER), the official arbiter

of U.S. recessions and expansions, doesn’t always agree with that metric. NBER classified the COVID pandemic

induced 2020 recession as being only one month in duration).

EPM Macro

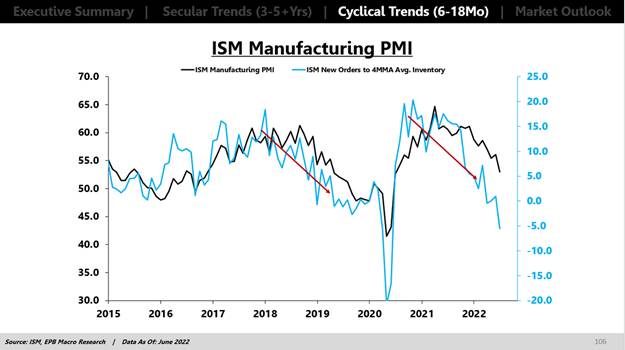

Research - Spotlight on ISM Manufacturing Index:

The ISM Manufacturing PMI is one of the most widely

watched and trusted measures of manufacturing activity and overall economic

health. It is highly cyclical and

captures the "growth rate cycle" quite well. A reading above 50 signals an expansion or positive growth, while a reading below 50 signals

contraction or negative growth.

On Friday,

the ISM PMI for June showed a more significant than expected decline, falling

from 56.1 in May to 53.0. More importantly,

the new orders component fell into contraction territory with a reading of

49.2 for June.

The spread

between the new orders and inventory readings is a reliable leading indicator

of the overall ISM Manufacturing PMI.

This makes sense because if new orders are falling faster than

inventory, then companies must cut production in the future to combat a

building imbalance.

The spread between the ISM new orders and inventory

sub-components crashed in June, which is a strong warning sign that future

declines in the overall ISM Manufacturing Index should be expected.

Given that the ISM Manufacturing PMI holds a very strong

correlation to earnings estimates, credit spreads, and more, the probability

that we see further declines should be a warning sign that more turbulence is

ahead in cyclical risk-assets.

Comment and Analysis:

What happened to the “strong

economy” that Fed Chairman Jerome Powell used as an excuse for last month’s

out-sized Fed Funds rate increase of 75 basis points (bps)? Fed Chairman Powell’s June 15th statement

(which we analyzed in two Curmudgeon blog posts): “Overall economic activity appears to have picked up after edging down

in the first quarter.” In our classic “Welcome to the Greatest Show on Earth – Presented by Jerome Powell,”

I said that “one must conclude he (Powell) is a fool, grossly incompetent, or a

liar.” Which one do you think he is?

Please let us know!

The Curmudgeon and I strongly believe that Powell is a disgrace to the institution

that everyone bows down to (the Fed). He substitutes a fantasy story for

obvious facts and ignores that the odds of a recession have been increasing for

months. While investment banks and economists raised their recession forecasts

last week, we forecast a recession months ago in these columns, starting in this Curmudgeon post: “My historical analysis of bear markets

concludes that those which are “fundamentally caused” (like the current bear

market) result in a recession.”

Last week, I stated the U.S. is already NOW in a recession

(not in 2023)!

Tom Porcelli, chief U.S. economist at RBC Capital Markets,

says this “may be the most anticipated recession ever.” Google searches for “recession”

and related terms are as high now as they were in March 2020. Yet Fed

Chair Powell still thinks the U.S. economy is “picking up?”

For the last several weeks, every (short lived) rally in the

equity market had a cockroach FOMC

member coming out of the woodwork to say the Fed was going to raise rates

50 or 75 bps at the next meeting, with multiple rate

increases to bring Fed Funds to 3.25-3.5% by year-end 2022.

As we’ve repeatedly stated in these Curmudgeon blog posts, we

don’t agree that the Fed’s “reverse wealth effect” monetary policy will

stop rising prices (it will not end the war in Ukraine or supply chain

bottlenecks or product shortages). Instead, it will cause tremendous collateral

damage. It’s already making anyone that

owns stocks and/or bonds MUCH poorer.

Certainly, the economic data surrounding the Atlanta Fed’s

-2.1% GDP projection for the 2nd quarter supports the conclusion

that the U.S. is already in a recession.

While the monthly Non-Farm Payrolls report (next one

is on Friday July 8th) hasn’t been weak yet, it is a lagging

indicator.

Also, there are anecdotal reports of widespread tech industry layoffs and hiring

freezes due to a soft economy. Here’s a recent example:

According to Reuters, Facebook/ Meta Platforms

CEO Mark Zuckerberg has cut plans to hire engineers by at least 30% this year,

he told employees on Thursday, as he warned them to brace for a deep economic

downturn. “If I had to bet, I'd say that

this might be one of the worst downturns

that we've seen in recent history," Zuckerberg told workers in a

weekly employee Q&A session, audio of which was heard by Reuters.

"I have to underscore that we are in serious times here

and the headwinds are fierce. We need to execute flawlessly in an environment

of slower growth, where teams should not expect vast influxes of new engineers

and budgets," Chief Product Officer Chris Cox wrote.

Zero

Hedge had this to say: “One month ago we showed that while the BLS still

revels in its seasonally-adjusted statistical nonsense to divine the monthly

level of payrolls, the real world is seeing a wave of mass layoff the likes of

which have not been seen since the COVID crash…When even the most profitable

tech companies are bracing for mass layoffs, the bottom is about to fall out

(of the economy).”

The Fed’s Dilemma:

If the Fed continues raising rates while the U.S. is ALREADY

in a recession, it could produce the worst economic downturn since the

depression in the 1930s.

In addition to the weak economic statistics noted above, we

pointed out in last week’s

post that commodity markets have turned down and Copper is in a bear market.

This week, U.S. Treasury yields dropped significantly in anticipation of an

economic downturn.

The yield on the two-year Treasury note,

the maturity most attuned to future Fed moves, slid by 22 bps this past week,

to 2.83%, the biggest drop since the March 2020 pandemic market crisis, and 60

bps below its mid-June peak. The benchmark 10-year T-note’s yield fell

24 bps, to 2.88%, and is down sharply from nearly 3.50% in mid-June.

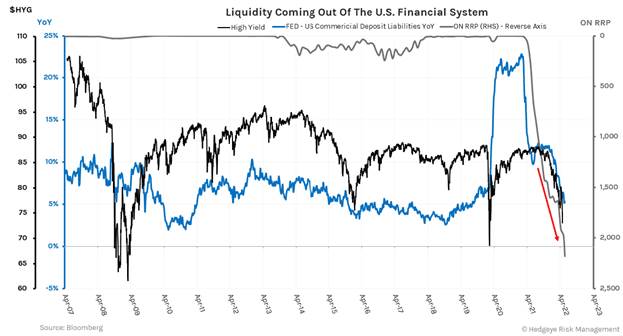

Charts of the Week:

Source: Hedgeye

……………………………………………………………………………………………………………

Point of Order:

Professor Steve Hanke is an expert on the history of

hyperinflation. In a recent interview

with Wealthion, the Professor was asked “Why does the Fed

get it wrong all the time?”

Reason: The Fed has ignored Milton

Friedman’s Quantity Theory of Money

to guide their monetary policy. Hanke

forecast a 9% inflation/CPI high for 2022 (vs actual 8.6% YoY CPI in his last

interview over a year ago on Wealthion. It was based on the Fed ignoring the

strong growth in the M2 money supply and monetary base and continuing with QE

and ZIRP.

“Of the approximate 400 economists at the Fed and or 700

economists and staff at Fed headquarters in Washington DC the “Democrats

outnumber the Republicans 48.5 to 1,” according to Professor Hanke.

Like everything in America these days, the Fed is all about

politics!

Cartoon of the Week:

Image Credit: John Darkow - politicalcartoons.com

…………………………………………………………………………………………………..

Curmudgeon’s Conclusions:

Victor and I are strongly convinced that the U.S. is already

in recession. In all of U.S. history we are not aware of any time the Fed has

increased rates when a recession was on going. Let alone more than doubling the

Fed Funds rate as voiced by so many Fed heads.

Having created the “all asset bubble” and 42-year high

inflation rate via its egregious “ultra-QE - free money party” the Fed is now

trying to over compensate by aggressively raising

rates while consumer confidence and the ISM PMI index are crashing, while

financial liquidity is vanishing (see above charts).

If the Fed follows through with its stated Fed Fund rate

rises, the credit markets will freeze up, the U.S. economic recession will deepen,

and U.S. equities could lose another 30% or more.

Victor’s Conclusions:

What will the Fed do? Or timelier what will they say? This is now crunch time! What is the

Fed’s plan? We will see, but it I don’t think it will be good, as the Fed is

now a 100% political institution.

“Check Mate” End Quotes:

“The laws of Chess do not permit a free choice: you have to

move whether you like it or not” Emanuel Lasker

“I am convinced, the way one plays chess always reflects the

player’s personality. If something defines his character, then it will also

define his way of playing.” Vladimir

Kramnik

………………………………………………………………………………………………..

Be well, stay healthy, try to find

diversions to uplift your spirits, wishing you peace of mind, and till next

time……

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever changing and arcane world of markets, economies, and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2022 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).