Stock Buybacks Exposed: Record Year, Outlook and Examples; Lower

Growth=Lower P/E?

by the Curmudgeon with Victor Sperandeo

Record

Year for Buybacks in 2018:

Fueled by corporate tax cuts from the Tax Cuts & Jobs Act (Dec. 22,

2017), U.S. companies bought back their shares at a record pace in 2018. According to data from S&P Dow Jones

Indices, stock buybacks by companies in the S&P 500 index climbed to $720.4

billion in the 12 months ended in September 2018, with about $203 billion in Q3

2018 alone. For the first nine months of

2018, buybacks are up 53% to $583.4 billion, which is 1% below the previous full-year record of 2007.

While end of the year figures have yet to be

finalized, S&P’s Howard Silverblatt says it was a

record year. Investment research firm TrimTabs says U.S. companies spent $1 trillion on buybacks.

Michael Schoonover, portfolio manager of the Catalyst Buyback Strategy

fund, told Barron’s that 2019 buyback announcements were at $1.08 trillion. That

number is greater than the gross domestic product of 166 countries!

Schoonover said that nearly half concentrated in 19

companies, which account for $460 billion of the total. Despite the

record-setting buyback authorization levels, 2018 has been an unusual year in

that fewer companies are accounting for the total buyback dollars spent.

The Curmudgeon has written extensively about how

stock buybacks artificially boost stock prices by reducing the number of

outstanding shares which artificially boosts increasing Earnings Per Share

(EPS) and also puts more cash in stockholders’ pockets

to be used for other stock purchases. In

other words, the supply of stock shrinks but the potential demand

increases. Please refer to this early post and this later one.

“Corporations have been a large, incremental buyer

(of their own stock). That’s had a very large impact on equity market returns

over the last few years,” said Wasif Latif, head of global multi-asset

investing at USAA Asset Management. “It seems like that large upward pressure

is going to continue to be there.”

”Companies have used their tax savings to push up discretionary

buybacks and boost earnings per share through significantly reduced share

counts,” said Silverblatt.

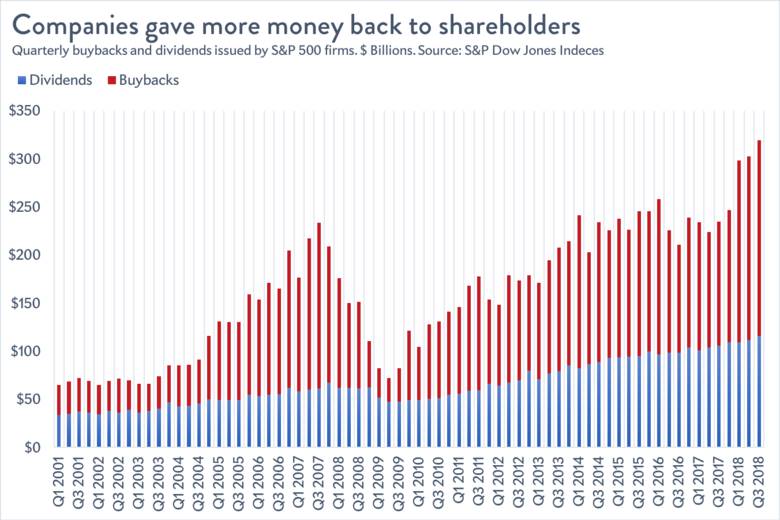

That can be easily seen in this chart, courtesy of

Slate:

Who’s

Getting Rich from Buybacks?

Jesse M. Fried and Charles C.Y. Wang wrote in the

July 6, 2018 WSJ (on-line

subscription required):

The

real problem is that buybacks, unlike dividends, can be used to systematically transfer value from shareholders to

executives. Researchers have shown that executives opportunistically use

repurchases to shrink the share count and thereby trigger

earnings-per-share-based bonuses. Executives also use buybacks to create

temporary additional demand for shares, nudging up the short-term stock price

as executives unload equity. Finally, managers who know the stock is cheap use

open-market repurchases to secretly buy back shares, boosting the value of

their long-term equity. Although continuing public shareholders also profit

from this indirect insider trading, selling public shareholders lose by a

greater amount, reducing investor returns in aggregate.

Executives

can use repurchases to enrich themselves because disclosure requirements are

woefully inadequate. When executives trade personally, they must publicly

disclose the details of each trade within two business days. The spotlight

created by such real-time, fine-grained disclosure helps curb trading abuses by

executives. By contrast, the SEC only requires a firm to report, in each

quarterly filing, the number of shares repurchased in each month of the quarter

and the average price paid per share. Investors see this filing a month or so

into the next quarter, one to four months after the buybacks occur. And they

never see individual repurchases, just aggregate transaction data. Researchers

can detect the existence of buyback abuses across a large sample of public

firms, but investors cannot easily identify the particular

executive teams using repurchases to line their own pockets.

As Victor notes in his comments below, not all

buybacks work to keep the stock price high.

Former DJI AAA rated General Electric (GE) is a great example. Former

CEO Jeff Immelt spent $21 billion in 2016 buying back GE shares at an average

price of $30.30. Currently, GE shares are trading around $8 per share on the

NYSE - about 75% off its $33 high set in July 2016.

A surprise loser of recent buybacks was Apple. Apple lost about $9 billion in 2018 as a

result of buying its own stock, according to the WSJ (again, please refer to

Victor’s comments below). That loss was increased on January 3, 2018 when

Apple's slashed earnings outlook took the iPhone maker's stock down 10%.

Democratic Senators Chuck Schumer of New York and

Tammy Baldwin of Wisconsin have introduced legislation to “rein in” corporate

stock buybacks. The bill would give the Securities and Exchange Commission

authority to reject buybacks that, in its judgment, hurt workers. It also would

require boards to “certify” that a repurchase is in the “best long-term

financial interest of the company.” Sen. Baldwin has introduced another bill,

co-sponsored by Sen. Elizabeth Warren (D., Mass.), that goes even further: It

bans all open-market repurchases.

Outlook

for Buybacks in 2019:

Silverblatt estimates that the dollar amount of stock buybacks

will be similar to 2018 or ~ $1 trillion. As long as the tax structure remains the same and the

economy doesn't fall apart, he expects companies will have the cash flow to

fund the buybacks.

Schoonover says 2019 is poised to be another strong

year for buybacks, especially if some of the market headwinds subside.

Goldman Sachs forecast $940 billion worth of buybacks

for 2019, while JPMorgan looks for ~20% fewer dollars spent on buybacks this

year. The investment and commercial bank

recently estimated $800 billion worth of buybacks will take place in 2019.

Joseph P. Quinlan, head of market strategy at Bank of

America, said last year's record share repurchases are likely to be a one-time

event. Instead, he sees lower stock buybacks as a result of decreased

repatriation cash flows. "As the cost of capital continues to rise,"

he said, "firms will probably resort to more holding of cash/capital (in

2019) vs. doling it back to shareholders via buybacks and dividends."

Instead of investing in future growth by increasing

capital expenditures, companies have been buying back their own stock and

increasing dividends. However, Economist

Robert Soloff worries that the decline in investment, especially since the 2008

financial crisis, has taken on a new urgency.

He wrote in the book What

Would the Great Economists Do?:

“…the stimulation of investment will favor intermediate run growth through its

effect on the transfer of technology from the laboratory to the factory.”

Victor’s

Comments and Provocative Opinion:

In the not too distant past, when a company bought

back its stock, it meant the company was going private. Yet the original

purpose of Wall Street was to help companies go public in order to raise

capital by selling shares to the public.

Investment bankers also manage secondary offerings, where companies sold

additional shares to expand operations through increased capital

investment. Raising capital (risk money)

to create businesses for the profit motive is the essence of capitalism. The company’s business and their intended use

of the capital obtained by selling shares to the public are detailed in the IPO

(Initial Public Offering) Memorandum and Prospectus, which are mandated by law

and overseen by the SEC. Generically,

these are referred to as “Disclosure Documents.”

With these basic principals in mind, if a company is

buying back stock, they don’t need any such documents or permission from the

SEC. However, I think a disclosure

document should be provided to shareholders in this case. Why? Because the

purpose the stock was sold to the public was to raise capital to grow the

company by building real products or providing services.

In recent years, buying back stock (with QE created

“free money,” zero/very low interest rates, borrowed money, corporate tax cuts,

or profits) is an effort to NOT to grow the company! Instead, it is an accounting trick to boost

the PRICE of the stock by reducing the float, which artificially increases

Earnings Per Share (EPS). Such

manipulation enables the company insiders, officers, and board of directors to

sell their stock and/or stock options at a higher price.

If a company is buying back stock what are the risks

to the investors? As an example, let’s

briefly analyze Sears. The company

spent a reported $6.2 billion buying 21.7 million shares of stock, and then

eventually went bankrupt. Evidently, the

purpose of the buyback was to hold up the stock price, not to increase

profits. Sadly, Sears plans to hold an

auction on Monday January 14th for the company's assets. The company

has already closed hundreds of stores in recent years, including dozens in

recent weeks. Ask yourself if that was

not immoral or (in my view) illegal?

The purpose of the company changed, because the

fundamentals of store/mall shopping changed consumer preferences. That was largely due to the rise of on-line

shopping and retail innovations like Amazon.com. I firmly believe Sears shareholders should

have been fully notified that the company had no ideas on how to create

profits, much less grow the company.

Moreover, the officers did not want to return the $6.2 billion (spent

buying back shares) to the stock holders, as the fat cat majority owners would

not make any money on such a deal.

It seems ironic that when a company sells stock,

rules and regulations require the company fully disclose risks, but if a

company uses the capital or profits for a NEW AND DIFFERENT purpose the SEC

does not require a disclosure of that along with the new risks?

There were an estimated $1 trillion in stock buy

backs in 2018. Since all stock indexes were down for the year, perhaps 99% of

all those buybacks are losers. Apple was

one such casualty of stock buybacks at high prices. The 12/28/2018 WSJ (on line

subscription required) reported that Apple stock buybacks lost the company more

than $9 billion! Apple spent most of

2018 ravenously buying back its own stock on the open market, fueled by a large

corporate tax cut windfall. Through the

first nine months of 2018, Apple spent $62.9 billion on share buybacks, a

record-breaking and staggering sum that happens to be exactly equal to Apple's

revenue in the quarter that ended in September.

Apple and companies like Wells Fargo, Citigroup Inc. and Applied

Materials, etc. re-purchased their own shares at high prices, only to see their

value decline sharply. In effect, the

stock market has told them they overpaid by billions of dollars.

Obviously, reducing the shares outstanding increases

earnings per share, all things being equal (which increases the bottom

line). But revenues will be lower, or

flat most of the time (which lowers the top line). As such, the logical deduction for investors

of a company buying back shares should be to

reduce the P/E!

Most investors don’t get this as they (like the

insiders) believe buying back stock increases the stock price. But the reason

for investing in stocks is to earn profits at a growing continuous rate. That

is the basis for the P/E! If a company

grows its earnings it is worth more and can and thereby increase dividends

without increasing the coverage ratio.

To purchase the stock of a company that is buying back its own shares

without a declining P/E is irrational in my opinion, as the future of the

company is shrinking, not growing.

Also, the accounting of earnings before, and after,

buybacks should be stated or taken into account. Obviously money spent on buybacks cannot be used to pay

dividends. This puts insiders and shareholders at odds, or in a conflicted

position. Those who have stock “options” don’t get dividends, so these officers

only care about stock price appreciation. This is another conflict which is not

obvious. How important?

End

Quote:

To quote an American forensic accounting scholar and

Professor of accounting:

“Accounting (measuring financial data with a

depreciating currency) is much like looking at a bikini on a beautiful

girl. What it reveals is interesting,

but what it conceals is vital.” -Abraham J. Briloff.

Good luck and

till next time………………….

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been

involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor

Sperandeo is a historian, economist and financial innovator who

has re-invented himself and the companies he's owned (since 1971) to profit in

the ever changing and arcane world of markets, economies and government

policies. Victor started his Wall Street

career in 1966 and began trading for a living in 1968. As President and CEO of

Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and

development platform, which is used to create innovative solutions for

different futures markets, risk parameters and other factors.

Copyright © 2019 by the Curmudgeon and

Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).