Earnings

vs. Stock Prices and Will a Trio of Warnings Fall on Deaf Ears?

by the Curmudgeon

Introduction:

In consideration for readers’

time and interests, we’ve partitioned the weekend blog post into two

parts:

1.

Earnings vs Stock Prices & Will A

Trio of Warnings Fall on Deaf Ears?

2.

Easy Money Policies Encourage Financial Risk Taking; NOT Capital

Investment

Part 1 (below):

We first provide an update on corporate earnings growth, which two rating firms

now forecast to be negative for Q3-2016.

Selected conclusions from a Leuthold Weeden

Capital Management (LWCM) analysis of future returns based on stock market

valuations are also presented.

A trio of financial market

warnings this week was little noticed by the mainstream media. Moody’s, BofA Merrill Lynch (BoAML), and

hedge fund titan Ray Dalio of Bridgewater Associates all said that financial

markets were at an inflection point and that the limits of central bank easy

money policies were close to being reached.

Part 2 (to be separately posted): Victor’s

directly related and incisive comments on why extraordinary easy money policies

have NOT led to capital investment or formation of new businesses.

Update on Earnings and

Stock Prices:

Let’s revisit one of our

earlier vital themes: “Do earnings matter for stock prices?”

·

We

noted in a September 9, 2016 Curmudgeon blog post that FactSet

reported S&P 500 corporate earnings were down in the Q2-2016, making it the

fifth consecutive quarter of negative earnings growth. Analyst earnings estimates were also

lower.

·

In

a September 28th Curmudgeon blog post FactSet forecast

a 2.3% profit contraction in Q3-2016 (from the year-earlier period).

·

That

number was slightly revised as of September 30th: “For Q3 2016, the

estimated earnings decline for the S&P 500 is -2.1%. If the index

reports a decline in earnings for Q3, it will mark the first time the index has

recorded six consecutive quarters of year-over year declines in earnings since

FactSet began tracking the data in Q3 2008.”

·

This

Friday, October 8th, Thomson Reuters I/B/E/S reported: “Third

quarter earnings are expected to decline 0.7% from Q3 2015. In the S&P 500, there have been 80

negative EPS pre-announcements issued by corporations for Q3 2016 compared to

35 positive EPS pre-announcements. By dividing 80 by 35 one arrives at an N/P

ratio of 2.3 for the S&P 500 Index.”

With respect to earnings and

stock prices, the best valuation metric is the P/E ratio. Leuthold Weeden

Capital Management did an investigation based on the Curmudgeon’s

inquiry1 and reported results in a recent report (client’s

only). Here are a couple of takeaways from

their findings (bold font added for emphasis):

1. Since stocks rank in the worst valuation

decile today and bond yields are near rock bottom, it’s not surprising that

our forward-looking return graph stands at a paltry 1.9% against a

long-term median of 7.2%. The median return strikes us as representative of the

returns actually earned over the last 60 years, but today’s record low rates

are discouraging for asset accumulators looking to build future wealth in a

balanced portfolio strategy. (The peak expected return in 1991 was driven by

the combination of a 7.6 P/E ratio and a 15.3% bond yield… like shooting fish

in a barrel.)

2. As for market valuations and interest rates, today’s

conditions sadly lead us to expect returns well-below median in coming years.

P/E ratios would need to fall and bond rates would need to rise (both to a

substantial degree) before investors could anticipate earning historical

long-term returns once again.

Note 1. The Curmudgeon

has owned Leuthold

Core Investment Fund (LCORX) and

Leuthold

Grizzly Short (GRZZX) mutual funds since their inception in 1996 and

2000, respectively.

……………………………………………………………………………………………………….

A Trio of Warnings by

Respected Authorities:

1. Moody’s - Liquidity Buoys Credit (related to

negative profit growth):

Quoting directly from the

report (client’s and subscribers only):

The extraordinarily

accommodative monetary policies of the world’s major central banks help to

explain why the downgrade share of US high-yield credit rating revisions

plunged from 82% for the 1st quarter of 2016 to 54% for the third

quarter. The latter was the lowest since Q2-2015’s 52%.

The

ultra-low benchmark interest rates of stimulatory monetary policies have encouraged

risk taking, which has benefited the performance of both high-yield debt and

equities. From 2016’s 1st to 3rd quarter, the US

composite high-yield bond spread narrowed from 776 bp

to 551 bps. Recently, the high yield spread narrowed to 497 bps for its

thinnest band since July 2015. The rally by high-yield debt was closely linked

to recovery by share prices, where the market value of US common stock was

recently up by nearly 20% from its low of February 2016.

Stable

credit quality ultimately requires profits growth (see related

section above on Earnings and Stock Prices?). The support from cheap

money may wear thin if profits continue to shrink. The avoidance of another

surge by high-yield downgrades vis-a-vis upgrades demands the widely

anticipated upturn by operating profits. In the event operating profits sink

for a third straight calendar year, the default outlook will worsen,

spreads will swell, and recession risks will become material.

2. BoAML - Peak Everything & Reversal of

Bullish Trends:

"We are convinced that

policy is decisively shifting in a direction that is less positive for

'deflation assets' and more positive for 'inflation assets,'" the BoAML

team, led by Chief Investment Strategist Michael Hartnett, wrote. This year and

next, investors face a reversal of "bullish" trends that have

buttressed globalization and liquidity in recent years, they argue. BoAML says it's time for investors to

consider a new normal for equity and fixed-income markets.

"A reversal of these

trends, together with a shift toward fiscal stimulus and higher interest rates

strongly argues that the excess returns from stocks and bonds in the past eight

years are also likely to reverse."

Key bullet points from their report (client’s only):

- Peak Liquidity, Globalization, Inequality…Peak Returns

- "Peak liquidity": the era of excess liquidity

is ending

- "Peak globalization": the era of free trade,

capital & labor mobility is ending

- "Peak inequality": as electorates demanding

"War on Inequality" via fiscal stimulus

- We are long stocks & commodities, short bonds; we

expect slim returns from bonds & stocks in coming quarters; but

double-digit upside likely for "ZIRP losers" in 2017

- Positioning, policy & profits to deliver a 2016/17

"flip" from "deflation" to "inflation": from

"ZIRP winners" to "ZIRP losers"; from Wall Street to

Main Street

- Positioning…few positioned for it; Policy…peak

liquidity, peak globalization, fiscal stimulus; Profits…US consumer, China

producer, inflation up

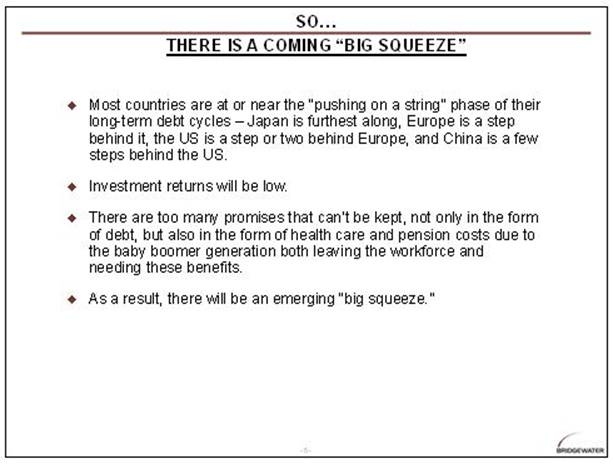

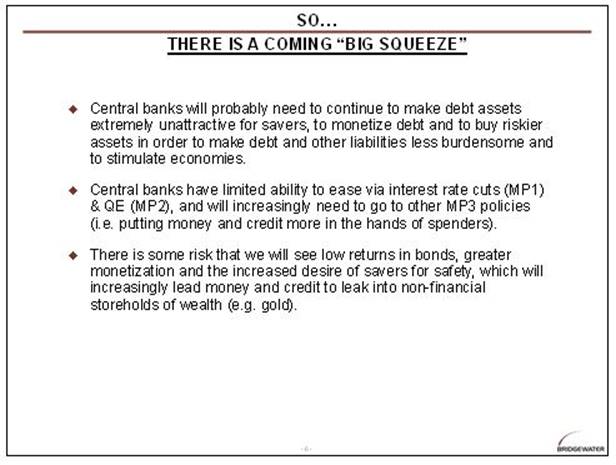

3. Ray Dalio, Bridgewater Associates: “There is

a coming big squeeze”

From a transcript

of Dalio’s speech at the Federal Reserve Bank of New York's 40th Annual Central

Banking Seminar on Wednesday, October 5, 2016:

Where

does that leave us now?

1)

Productivity growth is slow, though properly accounting for it has never been

more difficult

2)

The short-term debt/business cycles as measured by GDP gaps are closer to their

mid-points than to their extremes, and

3)

The long-term debt cycles are approaching their very late-stages as debts can’t

be raised much and central banks are approaching “pushing on a string”

limitations to their effectiveness.

The

biggest issue is that there is only so much one can squeeze out of a debt cycle

and most countries are approaching those limits. In other words, they are

simultaneously approaching both their debt limits and central banks’ “pushing

on a string” limits. Central banks are approaching their “pushing on a string”

limits both because interest rates are approaching their maximum lows, and

because the effectiveness of QE is approaching its limits as the risk premiums

and spreads are compressing.

Curmudgeon’s Conclusions:

Fixed

income investors have long been under the misguided belief that they can’t lose

in a zero (or negative) interest rate/ “QE forever” world. The very well respected authorities cited in

this article think that may soon change.

If central banks were the reason for so much yield chasing, it stands to

reason they can also be the reason for yield fleeing as soon as short or long

rates rise. That encompasses past

winners from US Treasuries, high grade corporate bonds, junk bonds, dividend

stocks, REITs, etc.

The

stock market reaction to this change will depend if it tips the US and other

developed nations into a full-fledged recession as Victor is predicting for

early 2017. Yet if one extrapolates

from the recent rise in stock prices during six consecutive quarters of

negative earnings growth, a recession

might be good news for stock bulls?

While

some may now believe in perpetual bull markets, we wonder if they have studied

the physics of its cousin- the perpetual

motion machine.

Good luck and till next time...

The

Curmudgeon

ajwdct@sbumail.com

Follow the

Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been

involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2016 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).