Does July’s Strong Job Report Mean Happy Times are Here

Again?

by the Curmudgeon with Victor Sperandeo

Analysis of Jobs Report (Curmudgeon):

The BLS reported on Friday

that US employers added 255,000 non-farm payroll jobs last month, Job gains

occurred in professional and business services, health care, and financial

activities. Employment in mining continued to trend down. June’s gain in non-farm payrolls was revised

upward by 5,000 jobs, and May's by 13,000.

Wages for private-sector workers were up 2.6% over the

last 12 months. That matched the

strongest annual pace of wage growth in seven years. More Americans joined the labor force in

July, keeping the jobless rate steady at 4.9% and the number of unemployed

persons was essentially unchanged at 7.8 million. Both measures have shown

little net movement since August 2015.

Yet other measures of the labor market suggest that

underlying joblessness is higher than the official 4.9% unemployment rate (also

see John Williams' comm entary

below). The broadest measure of

unemployment calculated by the Labor Department, which includes workers who

want full-time positions but cannot find them, stood at 9.7% in July.

In addition to the 7.8 million currently counted as

unemployed, there are more than 50 million Americans above the age of 55 who

say they don’t want to work and are, for the most part, retired. It also takes

into account 13.5 million Americans age 16 to 24, most of them in school, and

millions of women who have chosen to stay home to care for their young

children. None of those

people are considered unemployed by the Labor Department.

According to the above referenced BLS report (did the

reporters/commentators read all of it?):

Both the labor force

participation rate, at 62.8%, and the employment-population ratio of 59.7%,

were little changed in July. The number of persons employed part time for

economic reasons (sometimes referred to as involuntary part-time workers) was

little changed at 5.9 million in July. These individuals, who would have

preferred full-time employment, were working part time because their hours had

been cut back or because they were unable to find a full-time job.

In July, 2.0 million persons

were marginally attached to the labor force, about unchanged from a year

earlier. (The data are not seasonally adjusted.) These individuals were not in

the labor force, wanted and were available for work, and had looked for a job

sometime in the prior 12 months. They were not counted as unemployed because

they had not searched for work in the 4 weeks preceding the survey.

Reconciling Strong Jobs Report with Anemic GDP (and

declining Productivity):

The July increase in payrolls stands in sharp contrast to

data released just last week showing disappointing US economic growth of only

1.2% in the 2nd quarter of 2016.

According

to Saturday's NY Times, a big reason for the difference is that parts of

the economy are still suffering from the continuing fallout from low oil prices

as energy companies cut back on investment. Government spending also has been

weak and many companies have deferred investment in new plant and equipment

that would increase their efficiency and production output.

The Curmudgeon emphasizes that US business (capital)

spending has been incredibly weak, which does not bode well for future economic

growth. American companies, dogged by

shrinking profits (five or six consecutive quarters of down earnings –

depending on the source), have cut investment for the third straight quarter. Alongside steady hiring, that’s led to slumping

labor productivity growth.

……………………………………………………………………………………..

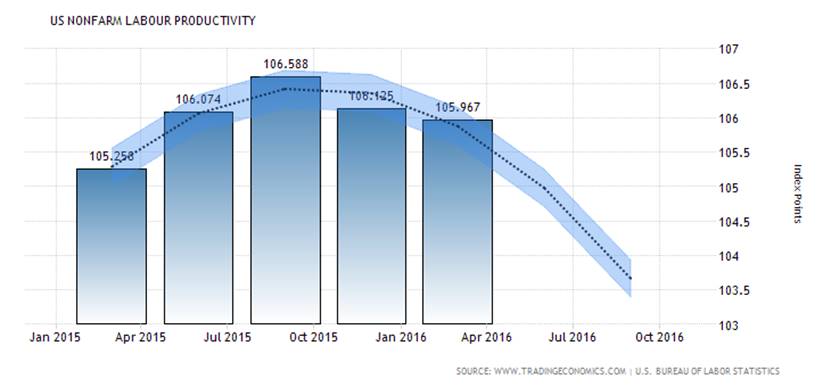

Sidebar:

Productivity is a key

to rising living standards. Steady gains

in productivity are needed to support higher incomes without sparking

inflation. On June 7, 2016, BLS reported that US

non-farm business sector labor productivity decreased at a -0.6% annual

rate during the 1st quarter of 2016.

[Labor productivity, or output per hour, is calculated by dividing an

index of real output by an index of hours worked of all persons, including

employees, proprietors, and unpaid family workers.].

Chart Courtesy of Trading Economics.

Bottom Line: An economy can't grow with GDP

at 1% and productivity DECLINING!

……………………………………………………………………………………..

Also, the economic outlook is weak outside the US,

representing another potential drag on the US economy (e.g. US exports and

repatriated earnings abroad). The International Monetary Fund (IMF) last

month downgraded

its forecast for global economic growth after Britain’s vote to leave the European

Union weighed on consumer confidence and investor sentiment.

“This apparent inconsistency— a willingness to absorb the

high cost of labor, yet completely shut down business capital spending—illustrates

how cautious CEOs remain given the uncertainties about the US election, the

fallout from Brexit, and the health of the global economy,” said Bernard Baumohl, chief global economist at the Economic Outlook

Group consultancy.

If business and government investment continue to lag,

that could undermine the long-term ability of the American economy to be more

productive and raise living standards for most workers.

“The question at this point remains, which data point is

more telling of the underlying momentum in the US economy: an average 1% GDP or

an average of 200,000 payrolls (for the 1st half of 2016),” said

Lindsey Piegza, chief economist at Stifel

Fixed Income.

John Williams' ShadowStats Opinion:

In letter

number 824, John writes:

·

Month-to-Month

Unemployment Data Remained Meaningless, Nonsensical and Heavily Skewed by

Inconsistent and Not-Comparable Seasonal Adjustments

·

Heavily

Bloated by Seasonal-Factor Distortions and Add-Factors,

·

Annual

Payroll Growth Effectively Held at a 29-Month Low

·

July 2016

Unemployment: U.3 Held at 4.9%, U.6 Notched Higher to 9.7% and the

ShadowStats-Alternate Rate Rose to 23.0%

From John's commentary (subscribers only- and we strongly

recommend readers subscribe!):

·

In

Continued Misreporting, Payroll Activity Remained Massively Overstated; Monthly

Unemployment Details Remained Not Comparable.

·

Underlying

reality for July 2016 US labor conditions was in the realm of a 23.0% broad

unemployment rate, with the actual monthly payroll-employment change likely on

the downside of flat.

·

The

“unchanged” headline U.3 unemployment at 4.9% in July was continued nonsense,

simply reflecting not-comparable and meaningless month-to-month changes in the

Household Survey data.

·

Consider

that headline Household Survey detail showed the number of employed increasing

by 420,000 in July 2016, while the number of unemployed declined by only 13,000

(-13,000)? This general pattern was seen repeatedly earlier in the year.

Normally, large swings in the count of the employed have some meaningful offset

in the count of the unemployed, going either way. That did not happen here,

because the seasonally-adjusted June and July data were not reported on a

consistent basis and simply were not comparable month-to-month.

·

The

gimmicked, headline payroll gain of 255,000 more realistically should have come

in below zero, net of built-in upside biases. Discussed in the

Birth-Death/Bias-Factor Adjustment section in the Reporting Detail, subsequent

to the downside payroll-benchmark revisions of February 2016, the usual,

excessive monthly biases added into the headline monthly payroll detail by the

Bureau of Labor Statistics (BLS) were revised to the upside.

·

This

less-obvious use by the BLS of the Birth-Death Model (BDM)3

artificially has inflated headline month-to-month payroll gains with

meaningless add-factors that currently are well in excess of 200,000 jobs per

month. Such is separate from the constantly shifting seasonal adjustment

patterns that can boost headline data in a given month (as in May 2016), with

no prior-period offset accounting.

Note 3. Victor has many

times called out the BDM as an extraordinarily phony tactic the BLS uses

to artificially increase non-farm payroll gains. You can read about it in Note 2. of

this post and in the

sub-head Phantom Jobs Created by "New Companies" Which Don't

Really Exist in this one.

……………………………………………………………………………………..

Victor's Analysis of the non-farm payroll numbers and its

impact on the markets:

This is the second month in row where the "highest

estimates" of the consensus predictions of the payroll jobs number has

been under estimated. Let's take a

closer look at the job numbers. The payroll number propaganda is weighted to

the number of jobs, not what kind of jobs.

·

Retail

jobs (minimum wage paying) with less than 30 hours a week was +289,000 year

over year (YoY).

·

Leisure

and Hospitality, also very low paying added +421,000 YoY.

·

Business

services +550,000 YoY, and

·

Health

Care + 476,000 YoY - the highest paying jobs of the bunch.

·

Government

jobs for the MONTH were the highest of the year at +38,000.

The market’s reaction was mixed:

·

The

increase of 255,000 new jobs caused the S&P 500 and the Nasdaq 100 to close

at new all-time highs. The US equity markets no longer appear to be concerned

about a Fed rate increase.

·

Other

markets were definitely worried that the Fed might raise rates at the next

(September 20-21st) FOMC meeting. The US dollar rallied, Treasury bonds &

notes sold off, while gold and silver declined -1.90% and -3.51%, respectively.

→My strong view is ZERO chance of this with 48

days before the next Presidential election.

Ironically, the stock market seems to be saying: if the

Fed raises rates that's “good," because it means the economy is finally

breaking out of its 2.07% record low growth rate from June 2009 to date1

and only 1% in the first six months of this year.

Note 1. The current economic “recovery/expansion" is the

lowest in history (NOT from just 1949 as reported by the WSJ last Saturday,

July 30th).

Conversely, when the jobs numbers are worse than expected

(many times over the past 12 months)2, equity buyers presume that

the Fed will not raise rates, and that is also "good” and so bullish for

the stock market!

Note 2. On May 6, 2016 BLS

reported that the US economy added only 11,000 jobs (way below analyst

estimates). The S&P 500 dropped to

2,039.45 intraday, but then rallied to close at 2,057.73 - up 7 points on the

day.

→So the markets theme is apparently: either heads

or tails, you win by being long stocks!

Lastly, the markets are looking at the well-respected

Atlanta Fed GDP NOW forecasts, even though it was dead wrong on 2nd

quarter GDP prediction of +2.3% one day before the number was released to

actually be only 1.1%. The Atlanta Fed GDP NOW is predicting 3rd quarter GDP to

be +3.8% as of Friday. Perception is reality until the recognition comes.

The US stock market is very expensive, based on P/E

ratios (and other metrics also). The S&P 500 has a

current 12 month rolling P/E of 25.26 and the S&P Industrials is at 29.88.

Even the DJ Utility Average P/E is 26.38.

→So whatever causes the end of the old bull market,

and economic expansion, the results will be awesome.

Jobs, the Economy and the Presidential Election (Victor):

The obvious reasoning from most market thinkers is the

party which controls Presidential power wants to retain that power. But

sometimes it doesn't work out that way:

·

After the

GOP (or the "Stupid Party" as Pat Caddell

calls them) permitted the markets to crash by letting Lehman Brothers go

bankrupt, Democrat Barrack Obama won the 2008 Presidential election.

·

The

mother of all administration blunders was led by the dumbest President of all

time -the GOP's Herbert Hoover (1929-32), whereby both market declines were

associated with the "Great Recession" and "Great Depression

"which caused a 100% loss of government power to the Democrats.

You can certainly see why the current Fed, and everything

else the Democratic administration controls will attempt to influence the

November elections such that the Democratic party will be victorious. Such

control is especially true for the markets and the economy.

This is not your ordinary election. the Neo-Con

GOP/libertarians, and the Progressives/ Liberals/ Democrats all hate Donald

Trump because he can change the system (which is a racket), and that is the

greatest fear of the establishment. Therefore, more media propaganda and by

hook or crook tools will be used in an attempt to get Hillary Clinton elected

as our next President. This includes economic fabrication, including the polls.

Victor's Conclusions:

Can two consecutive months of strong jobs reports (a

lagging economic indicator) compensate for sub-par economic growth? OF COURSE NOT! However, traders don't care as they have very

short term mentalities and so they trade the headlines. I believe the Fed manipulates stock prices to

its desires and personal goals, but that has nothing to do with the politics of

power.

The current administration has the power. They are doing a hell of a job to make people

believe things are good. Does the government actually believe itself? See this 30

second video of a State Department spokesman and then decide for yourself!

Statements from the Fed and virtually all government

agencies, bureaus and officials are now largely “spin.” Which means, according

to Criss Jami:

"Just because something isn't a lie does not mean

that it isn't deceptive. A liar knows that he is a liar, but one who speaks

mere portions of truth in order to deceive is a craftsman of destruction."

That leads to our current political/economic/financial

state of affairs. The reality of the consequences of this “spin” is the oldest,

truest quote known to man:

"La plus belle des ruses du diable

est de vous persuader qu'il n'existe pas."

Translation: "The devil's finest trick is to

persuade you that he does not exist."

From -Le Spleen de Paris-

a collection of poems by Charles Baudelaire.

Good luck and till next time...

The

Curmudgeon

ajwdct@sbumail.com

Follow the

Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2016 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).