Complacency

and Confidence Soar as Central Banks Ignore Surging Asset Bubbles

By the Curmudgeon with Victor

Sperandeo

Introduction:

Stock market sentiment,

complacency and confidence has remained elevated for a very long time. That’s

the subject of this week’s Curmudgeon post.

We don’t know when excessive

bullishness will diminish, but we’ve never seen anything like it before. Victor and I don’t think it will end as long

as the Fed keeps its “printing press” rolling.

Our End Quote from

GMO’s Jeremy Grantham sums up our thesis on the Fed persistently ignoring asset

bubbles.

A Rising Tide Lifts All Boats:

The Wall Street Journal notes

(emphasis added):

"The

frenzied stock-buying activity that may have saved AMC Entertainment Holdings

Inc. from bankruptcy is opening up a potential escape hatch for other

troubled borrowers as well.

More

companies with steep financial challenges are seeking a lifeline from equity

markets, eager to capitalize on the surge of interest in stock buying from

nonprofessional investors.

But

equity markets now are more open to supporting troubled issuers, in large part

because of risk-hungry individual investors eager to speculate,

according to bankers and investors following the trend."

According to Bloomberg

data, there have been 254 profitable companies issuing secondary or add-on

shares over the past 12 months. But there have been 748 unprofitable companies

doing the same, for a net differential of more than 500 companies. That’s a 3 to 1 ratio in favor of money

losing companies!

This chart, courtesy of Sentiment Trader says it all:

All of this issuance amounted

to more than $27 billion worth of offerings that have been priced. That, too,

is a record amount dating back 40 years.

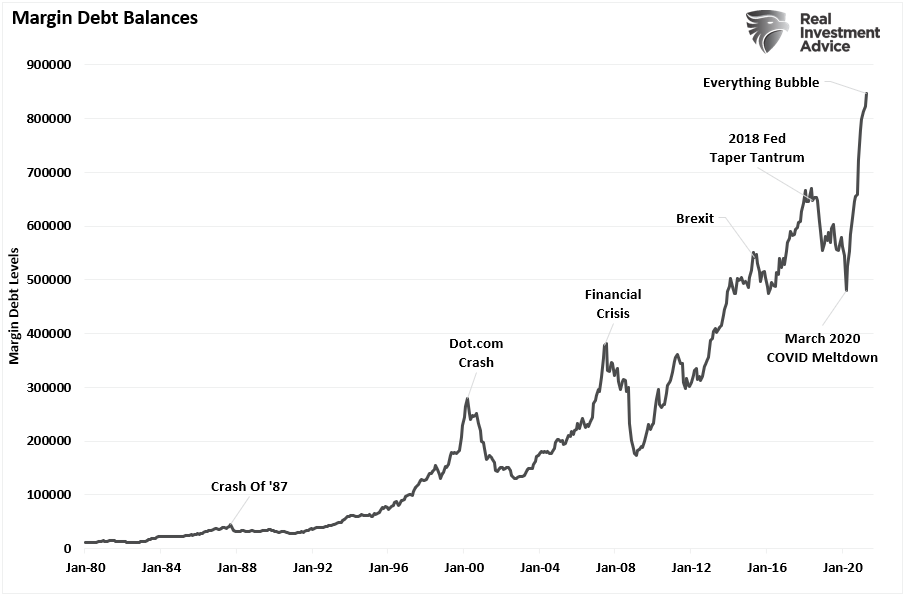

Bullishness in Spades:

We have never seen market

sentiment so BULLISH for so long. The

extraordinary amount of BULLISH exuberance can be visualized by record margin

debt levels as per this Exhibit 1 chart from Real Investment

Advice:

Exhibit 2 is a new survey from Natixis which shows a clear

example of “recency bias” at work. Here

are a few excerpts:

“Despite the economic impact

of the pandemic, investors report average investment returns of 12.5% above

inflation in 2020. Now, with the reality of effective vaccines and unmasked

economies, investors expect to revel in a long run almost three times what

financial professionals say are realistic.”

“Wealthy Americans are pretty

optimistic about their long-term investment returns, expecting to earn average

annual returns of 17.5% above inflation from their portfolios. That’s according to a new survey from Natixis

that surveyed households that have over $100,000 in investable assets in March

and April of 2021.”

There’s also a “moral hazard” factor with the belief the Fed will continue to support

markets indefinitely.

Complacency and Confidence:

With respect to “investor” complacency, the CBOE

Volatility Index (the VIX), tumbled to pre-pandemic levels this week. It closed Friday at 15.62 vs a 52-week high

of 41.16.

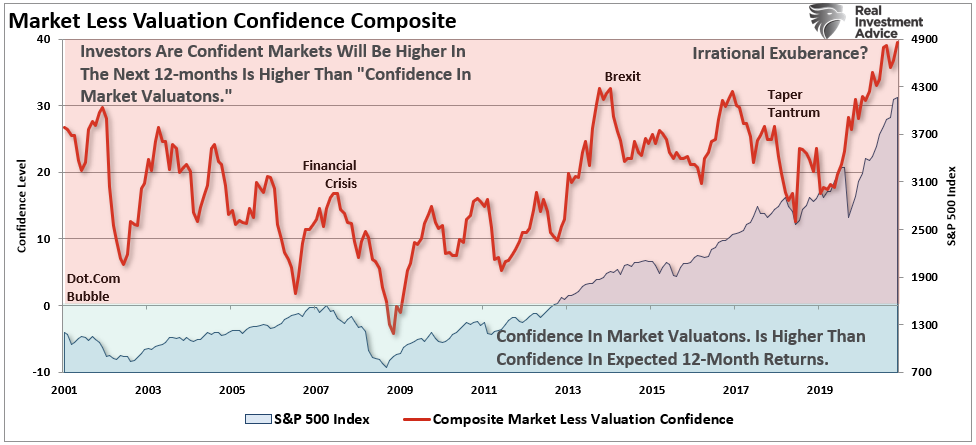

Let’s look at the Bespoke “irrational exuberance” indicator. It subtracts the “Valuation Confidence

“from the “One Year Confidence” survey data. Recently, this reading has exploded

higher for both institutional and individual investors.

When the reading is positive, it means confidence that the market will be

higher one year from now is higher than confidence in the valuation of the

market. The opposite is the case when the reading is in negative territory.” –

Bespoke

The key takeaway is that “investors

simultaneously believe the market is over-valued but likely to keep climbing.” Why? Because the “Fed has investor’s backs.”

Once again, this week, Sentiment

Trader’s Dumb Money Confidence index is very optimistic and Smart

Money Confidence is neutral.

Sentiment Trader concludes by saying:

“We've been in the Enthusiasm phase of a Typical

Sentiment Cycle for more than six months now. The phase usually exhibits all of

these factors:

· High optimism

· Easy credit (too easy, with loose terms)

· A rush of initial and secondary offerings

· Risky stocks outperforming

· Stretched valuations

We need to be on the lookout for internal divergences and

warnings among technical indicators during and after these phases.”

Sky High Valuations:

The 52-week trailing P/E of

the S&P 500 at 45.48 is now greater than the 2000 Dotcom bubble peak and

the second highest of all time. That’s depicted in this chart:

The Buffett Indicator

(named after Warren Buffett, who claims this is his favorite macroeconomic

indicator) is the ratio of total U.S. stock market valuation to GDP. It

is currently at 236%, which is 89% (~2.9 standard deviations) higher than its

historical trend line, indicating the market is currently Strongly

Overvalued.

……………………………………………………………………………………………………….

Conclusions:

Equity markets around the

world are in uptrends, because central banks, acting in unison as a globalist

entity, have shown a willingness to “print” an unlimited amount of paper/fiat

currency to keep this counterfeit, fictitious game going.

The value of fiat money

is derived from the relationship between supply and demand and the stability of

the issuing government, rather than the worth of a commodity backing it as is

the case for commodity money. Fiat money

gives central banks greater control over the economy because they can control

how much money is printed.

In this recent Curmudgeon

post we noted that all fiat currencies have lost all their value

over time due to inflation. In

particular, we wrote:

The

statistics of paper currencies are like that of Socialist Countries --they ALL

lose. Since 1900 to the end of 2010 — 450 paper currencies — DIED! Some like

zombies, return in another name, then die again. The Brazilian Real paper

(monopoly game) currency has been reborn eight times, with a small valuation

change each time.

Governments/global central

banks will always use budget deficits and printing presses (aka “keystroke

entries”) rather than go bankrupt. The

bureaucrats want to save their careers. As long as they can spend more than

what they take in, and “print” fiat currency, the public does not object and

the financial spin game goes on.

In the U.S. it’s a recirculating

Ponzi scheme: 1) federal government runs huge budget deficits, 2) U.S.

Treasury Dept auctions more bonds and notes to finance the budget shortfalls,

3) Fed buys most of those bonds/notes from its dealer banks, 4) those Fed

member banks then deposit some of the proceeds back at the Fed where they earn

10bps of interest. However, most of the

money created by the Fed flows into financial assets rather than the real

economy.

Today, U.S. stock market

valuations are worthless as a standard of measure, when the goal seems to

be to overturn the Constitutional Republic towards a Marxist/Socialist

government with excessive money creation and free handouts. So, if nothing

changes, expect stocks and inflation to continue to higher levels. (Victor)

End Quote (emphasis

added):

“All four chairmen

post-Volcker have underestimated the potential economic damage from inflated

asset prices, particularly housing, deflating rapidly. The role of higher

asset prices on increasing inequality also hasn’t been considered. Asset

bubbles are extremely dangerous.

This current event is

particularly dangerous because bonds, stocks and real estate are all inflated

together. Even commodities have surged. That perfecta and a half has never

happened before, anywhere.

The pain from loss of

perceived value will only get more intense as prices rise from here. In short,

the Fed since Volcker has been pretty clueless and remains so. What has been

more remarkable, though, is the persistent confidence shown towards all of

these four Fed bosses despite the demonstrable ineptness in dealing with

asset bubbles.”

Jeremy Grantham,

financial historian and co-founder of the investment firm GMO in an interview with Bloomberg.

…………………………………………………………………………………………….

Celebrate a return to normal

and take advantage of the many places reopening. Stay healthy, take care of yourself and each

other, and till next time……

The Curmudgeon

ajwdct@gmail.com

Follow

the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor

Sperandeo is a historian, economist and financial innovator who

has re-invented himself and the companies he's owned (since 1971) to profit in

the ever changing and arcane world of markets, economies and government

policies. Victor started his Wall Street

career in 1966 and began trading for a living in 1968. As President and CEO of

Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and

development platform, which is used to create innovative solutions for

different futures markets, risk parameters and other factors.

Copyright © 2021 by the Curmudgeon and

Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the original

posted article(s).