Euphoric U.S.

Stock Market and Pandemic Plagued Economy in Total Opposition

By the Curmudgeon

Introduction:

The disconnect between the

euphoric U.S. stock market and struggling real economy has never been greater. Despite a pandemic that has killed more than

300,000 people, put millions out of work and shuttered businesses around the

country, the market is now somewhere between euphoria, nirvana, and utopia.

Institutional investors who

have been bullish for much of 2020 are ignoring what’s

happening in the real economy and continue buying stock because “the market is

going up.” They are comforted by the

Fed’s continued zero interest rate policy (ZIRP) and monthly buying of about

$80 billion worth of Treasury debt and $40 billion in mortgage-backed

securities. The Fed has indicated that

program will remain intact for an indefinite time period.

Individual investors have

piled into the market this year and are trading stocks at a pace not seen in

twenty years. That’s driving a significant part of the

market’s upward trajectory and is evident in recent frothy IPO prices,

which we described in this article. Brokerage houses say strong demand from

individual investors drove the surge of trading in Airbnb and DoorDash

– neither of which are profitable. Professional money managers largely stood

aside, astonished and in awe at the prices smaller investors were willing to

pay.

Let’s take a

deeper look at what’s happening in the markets and real economy and offer our

thoughts on same. In a companion piece,

Victor provides a Perspective

on Monetarism, Valuations and Manias.

Examples of High Valuations

and Speculative Excess:

· The

trailing 52 week price-to-earnings (P/E) ratio for S&P 500 index is

39.94 while last year it was 25.23 (source: Wall Street Journal). The last time that market index was at or

above that level was in 2000.

· The

current Shiller PE Ratio is 33.71, which is

more than double the median of 15.1 and the mean of 16.3. It’s based on

average inflation-adjusted earnings from the previous 10 years and is also

known as the Cyclically Adjusted PE Ratio (CAPE Ratio).

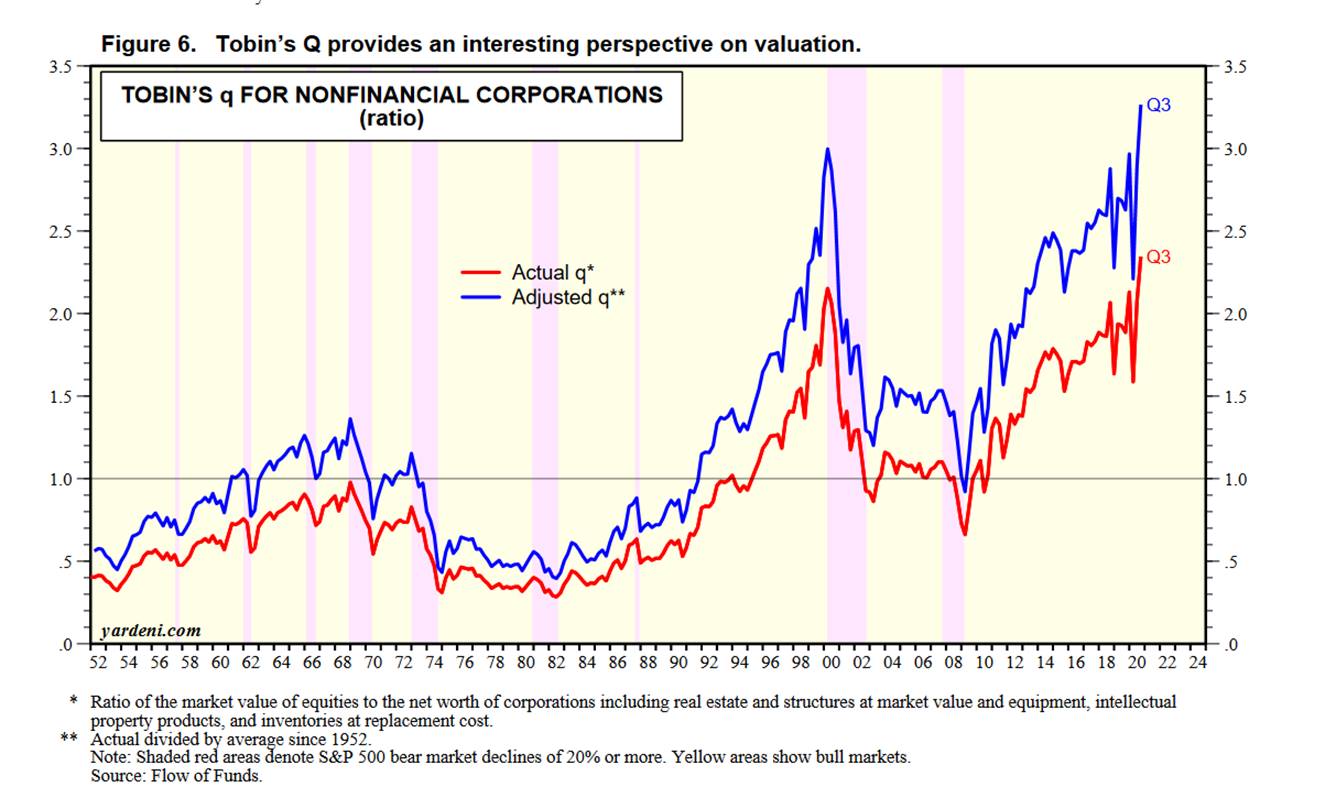

· The Tobin

Q ratio (the ratio of the market value of equities to the net worth of

corporations at replacement cost) is at an all-time high in both adjusted and

non-adjusted terms. Both measures are

above previous highs in 2000. Please see Tobin Q graph below.

· Russell

2000 (small) companies should be hurt more than large caps by the COVID-19

lockdowns, business closures, restrictions, etc. Nonetheless, Russell 2000

stocks have rallied like a rocket ship! The small cap index has gained 102% off

its March 18th low, only the second time it has doubled off its

bottom in its entire history. It was up

over 18% in November – a new record. All

that came with no corrections or backing and filling, let alone a test of the

March lows. According to the Biryani

Associates, the current FORWARD 12-month P/E for the Russell 2000 is 79.96. The trailing P/E cannot be calculated

since there was a cumulative loss (e.g., negative earnings).

· Individual

speculators have returned to the market in mass, for the first time

since the dot com bubble. For many, trading stocks started as

a way to indulge their speculative itch when other avenues, such as

sports gambling, were shut down. That

has continued unabated as stocks continued their inexorable trend higher this

year.

· Small

specs are throwing money at trendy, tech-focused companies, which are relatively

new and unproven. Their favorites include cloud computing software maker Snowflake,

the online surveillance company Palantir and the energy storage company QuantumScape, which is up 144% in December alone.

They also like Etsy, the online marketplace, which is up 330% this year.

Just over a week ago, 908 Devices — a maker of hand-held analytic

devices — rose about 150% in its trading debut.

· For IPOs

in December, shares on the first day of trading skyrocketed 87%, on

average, as of the week that ended Dec. 18. That’s the

highest since early 2000, when the dot com bubble began to burst.

· Tesla, a

darling favorite of retail investors (and panned by most hedge funds) joined

the S&P 500 on Monday. It’s up 691% this year, giving it a market value of

more than $600 billion and bloating its price-to-sales ratio to 22 from 3 at the

beginning of 2020.

· Options

trading exploded this year as individual investors flocked to the stock market. A

record number of options contracts have traded this year. An average of 29

million contracts changed hands each day this year, a 48% jump from 2019,

according to data from Options Clearing Corp.

The volume for U.S. call options also hit an all-time

record. The 20-day moving average of call volume just surged past 22.5

million contracts. That’s up 30% from the previous

quarter and more than twice last year’s volume.

· Citibank

Panic/Euphoria Model—which factors in a number of

metrics from options trading to debt—has reached the highest level since 2000

at the peak of the dot com bubble.

Citi’s Tobias Levkovich warned: “Current

euphoric readings signal a 100% probability of losing money in the coming 12

months if we study historical patterns.”

· Bank of

America’s December Fund Manager Survey was the most bullish of 2020

as vaccine hopes induced a strong “buy the reopening trade.” Positioning

continues its climb towards “extreme bullishness” with the BofA Bull & Bear

indicator up to 6.7 (“extreme bullish” level of >8.0). Cash levels fell to

4% and triggered the FMS “sell signal.”

· Margin

debt expanded to a record $722.1 billion through November, according to the Financial

Industry Regulatory Authority, topping the previous high of $668.9 billion

from May 2018. If collateral falls below a certain threshold, a margin call is

triggered. Margin speculators then have the option of either putting up more

money or selling the securities underlying the loans. That always exacerbates downside volatility.

· High

yield bonds have extremely low credit quality, and the yields are

comparatively very low. A record number of companies

have been rated CCC this year, and these are the bonds that have appreciated

most in 2020. Trying to evaluate junk

bond yields and spreads

to true default risk has

been rendered a useless exercise.

· The volume

of debt that U.S. companies have taken on this year has come to an

unprecedented $2.5 trillion and has pushed the debt-to-equity ratio to

record highs. The markets seem to be saying that corporate (and U.S.

Treasury) debt never has to be repaid.

SOURCE: Yardeni Research Inc.

…………………………………………………..

Don’t Fight

the Fed:

Fed Chair Jerome Powell said

on December 16th that the Fed would keep short term interest rates

at rock bottom (0 to 0.25% Fed Funds rate) and continue to buy Treasuries and mortgage-backed

bonds for the foreseeable future. That amounts to a powerful tailwind for the

stock market.

“You have this grand maestro

up in the front that’s conducting the orchestra,” Mike Lewis, head of U.S. cash

equities trading at Barclays in New York, said of the Fed’s easy money policy.

“And until they stop, the music is going to continue to play.”

That quote is reminiscent of

former Citigroup CEO Chuck Prince’s infamous quote in a July 2007 interview

with the Financial Times. He told the FT: “When the music stops, in terms of

liquidity, things will be complicated. But as long as

the music is playing, you’ve got to get up and dance. We’re still dancing,” he

said. Please see End Quotes and last

sentence of this post for more on the music still playing.

Economic Assessment and Market

Outlook:

Current pandemic lockdowns and

restrictions will continue. More will

likely be enacted this winter.

Consequently, adverse economic effects are likely during the 1st quarter

of 2021. Moreover, the sizable monetary impulse and fiscal stimulus did not

feed into the real economy.

Economic indicators, such as

loan demand, are contracting again. Consumer spending is weak, household income

is falling, and millions remain unemployed with unemployment insurance expiring

for many.

Yet the financial markets

ignored all of the chaos and suffering of this

dystopian present and are instead look forward to a utopian future. Indeed, U.S. equities are priced for

perfection and market participants are extremely bullish.

As per the B of A bullet point

above, sentiment gauges across the board are recording extreme bullish

sentiment, low cash ratios, and high equity exposure all at the same time. The

popular opinion is that nothing can take the equity market down if a pandemic

and the severest recession since the Great Depression couldn’t.

What could possibly go wrong

to derail the bullish trend? We don’t know, but as Victor has opined numerous times over the

years, it will be an event(s) that the Fed can NOT control.

Legendary Merrill Lynch

Technical Analyst said the public buys the most at market tops and the least at

the bottom. Here’s recent proof of that

maxim: Net inflows into U.S. equity

funds ballooned to $29.4 billion in the December 15th week. ETF

inflows have totaled $46 billion so far in December (and that follows $81

billion of net buying activity in November).

-->Remember that this is

the same group of investors that were busy redeeming in large numbers at the

March lows!

Main Street vs Wall Street:

It’s

important to note that most Americans have not shared in this year’s stock

market gains. About half of U.S. households do not own stock. Even among those

who do, the wealthiest 10% control about 84% of the total value of U.S. equity

shares, according to research by Ed Wolff, an economist at New York University

who studies the net worth of American families.

As detailed in almost every

news source, millions of Americans are without jobs or income, largely due to

the pandemic restrictions and business shutdowns. The Washington Post reports that they have been

inundated with messages and phone calls from people on the verge of losing

their homes and cars and going hungry this holiday who are stunned that

President Trump and Congress cannot agree on another emergency aid package.

Several broke down crying in phone interviews as they are about to be evicted

from their homes.

In no uncertain terms, the

year 2020 was a BEAR MARKET for humans! But helping people get jobs, have enough food

to eat and not be evicted from their residences isn’t

high on the market’s list of priorities.

It’s liquidity, QE, and ultra-low interest

rates that have ruled the market since March 2009.

This dichotomy between stock

market investors/speculators and the rest of the population has widened income

inequality to unprecedented levels and has created a whole new dimension of

haves and have-nots.

Conclusions:

The Federal Reserve’s efforts

to keep interest rates at unprecedented low levels (such that real interest

rates are negative across the maturity spectrum) squashed the returns available

in fixed-income markets, pushing investors into equities. The central bank

thereby incentivized risk-taking in financial assets (stocks, high yield bonds,

bitcoin, etc.) at a time when risk aversion was not only advised but

required—for everyday activities like simply going out to eat or a movie (you can’t do either of those - even outdoors- in Santa Clara,

CA).

The prevailing belief is that

stocks can’t go down and have somehow morphed into

riskless assets —throwing caution to the wind is the way to play the

market. Haven’t we seen that sort of

attitude before?

End Quotes:

“We are seeing the kind of

craziness that I don’t think has been in existence, certainly not in the U.S.,

since the internet bubble. This is very reminiscent of what went on then,” said

Ben Inker, head of asset allocation at the Boston-based money manager Grantham,

Mayo, Van Otterloo.

"I do think we're at a

moment in time where there's a lot of euphoria. I personally am concerned about

that. I don't think in the long run that's healthy. I

think it will rebalance over time as it always does," said Goldman Sachs

CEO David Solomon.

“The market right now is

clearly foaming at the mouth,” said Charlie McElligott,

a market analyst with Nomura Securities in New York.

“The stock market is euphoric

right now,” said James Angel, a Georgetown University finance professor. “A lot

of people are extrapolating from the recent past and going, ‘Wow, the market’s

gone up a lot and I think it’ll go up more.’ We’ve seen this play out before,

and it doesn’t end well.”

B of A Chief Equity Technical

Strategist Stephen Suttmeier says, “the only thing we

have to fear (in the market) is perhaps the lack of fear itself.” Nonetheless, he’s bullish equities, high yield and emerging markets for

2021.

And the beat goes on…. until

the music stops.

……………………………………………………………………………………………

Good health, stay calm and

safe, persevere under lockdowns and till next time….

The Curmudgeon

ajwdct@gmail.com

Follow

the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor

Sperandeo is a historian, economist and financial innovator who

has re-invented himself and the companies he's owned

(since 1971) to profit in the ever changing and arcane world of markets,

economies and government policies.

Victor started his Wall Street career in 1966 and began trading for a

living in 1968. As President and CEO of Alpha Financial Technologies LLC,

Sperandeo oversees the firm's research and development platform, which is used

to create innovative solutions for different futures markets, risk parameters

and other factors.

Copyright © 2020 by the Curmudgeon and Marc

Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).