Are U.S. Stocks in a Bear Market or Just a Correction?

by the Curmudgeon

To answer this question, let’s look at several

reliable sources for guidance and direction:

1. As of

December 7th, Leuthold

Group’s Major Trend Index says “This Is a Bear Market.” Leuthold’s Chief Investment Officer &

Portfolio Manager Doug Ramsey writes:

The Major Trend

Index (MTI) fluctuated within its

negative zone throughout November before closing the month at a

decisively-bearish ratio of 0.76. Consistent with the high-risk environment

suggested by the MTI and other evidence, the Leuthold Core and Global Funds

remain positioned with net equity exposure of about 37%.

It’s notable

that the MTI improved very little in response to either of the two minor lows

of the fall correction, or to the two ensuing rallies. In the case of the former,

we expected more combined improvement in the MTI’s “countertrend” categories

(Intrinsic Value and Attitudinal); in the latter, a bigger reversal in the

Momentum/Breadth/Divergence work should have occurred (although that’s still

possible). If the rally that began the last week of November continues without

significant MTI improvement, we will move Core Fund net equity exposure to the

very bottom of its 30-70% guideline range. We won’t rule out doing the same in

the Global Fund, although in the wake of bear-sized losses suffered by many

foreign markets, we note the valuation profile of the Global Fund’s long equity

position is much lower than that of the Core Fund. (In fairness, foreign

equities were much cheaper than domestic stocks before those losses.)

Modest

improvement in the Economic/Interest Rates/Inflation category during the month

masked a major shift within key indicator groupings. Leading inflation measures

have faded sharply, with upgrades across the board in the commodity readings,

and (most recently) a big jump in the NOPE Index, which moved back into its

bullish zone with the ISM update for November. Gains in the inflation work,

however, have been offset by steady deterioration in the monetary and liquidity

measures—including interest rate momentum, money growth, and the yield curve.

That leaves us wondering whether the drop in inflation

pressures is even a bullish thing. Not every expansion ends with an “overheat.”

……………………………………………………………………………………………………………………………………………………

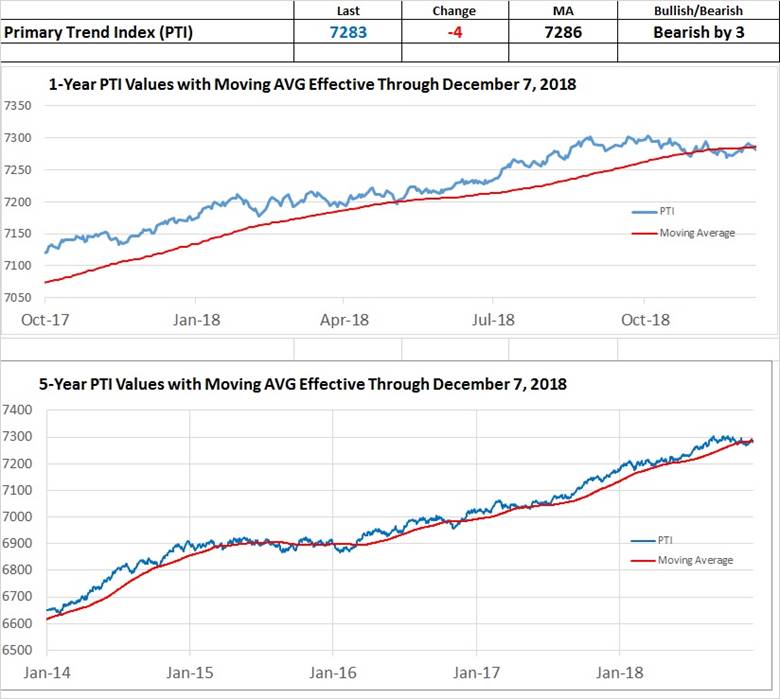

2. The late

and great Richard Russell of the now

defunct Dow Theory Letters developed

his proprietary Primary Trend Index

(PTI) for the U.S. stock market in the 1960s. It is composed of 8

indices, all geared to market action.

The PTI has been very reliable in identifying the major stock market

intermediate and long-term trends. Currently, it is just barely in the bearish

camp as can be seen from these charts:

Russell stated that the PTI works best when it was

decisively above or below its 89-day moving average. When above that average, the primary trend is

up and a bull market rise is in force. Below the moving average is a sign of caution

that the bull market could be stalling out.

A sustained decline below the moving average signals the primary trend

is down and stocks are headed lower.

The first chart above show that the PTI just entered

the bearish zone on Friday December 7th (-4 on the day puts the PTI

bearish by 3). The second chart

indicates that the PTI is right at its moving average, which is neither bullish

or bearish.

3. According

to the latest Aden Forecast, the Dow

Transports (now at 9,951.16) must close below 9905 to confirm a Dow Theory sell

signal (both the Dow Industrials and Transports must close below their last

respective correction lows). The Aden

sisters state that “If the markets now stay below 7275 for NASDAQ, 10550 Dow

Transportations and 2715 on the S&P500, then stocks will be headed lower.”

Here are recent stock market index performance

numbers:

Dow

Industrials daily change:

Monday: Up 287.97 points.

Tuesday: Down 799.36 points.

Thursday: Down 79.4 points (after a much larger

intra-day decline).

Friday: Down 558.72 points. [Dow Jones Transports were DOWN a whopping

407.54 points or -3.93%]

For

the Week:

Dow industrials were down 1149.51 points or 4.5%.

[Dow Transports were down 869 points or -8.03%]

Nasdaq composite was down 361.29 points or 4.9%.

S&P 500 index was down 127.09 points or 4.6%.

Year

to Date:

Dow Industrials

9.5% down

from the high of 26,951.81 on 10/03/2018.

4.5% up from the low of 23,344.52 on

04/02/2018.

Nasdaq

14.3% down

from the high of 8,133.30 on 08/30/2018.

5.1% up

from the low of 6,630.67 on 02/09/2018.

S&P 500

10.5% down

from the high of 2,940.91 on 09/21/2018.

4.0% up

from the low of 2,532.69 on 02/09/2018.

4. Russell Investments' Doug Gordon

told

CNBC 's "Trading Nation" on Friday:

“The first and

fundamental question: Is this a

correction or is this the start of the bear market? While you can certainly see a path that could

get us to a bear market, I think it's more of a messy correction. We could go a

little deeper."

Mr. Gordon believes the correction will span about

two to four months, citing the end of the 90-day trade war cease-fire between

the U.S. and China as an important marker.

"The sources of risk right now are really exogenous, meaning

they're hard to forecast. They're risks obviously tied to trade restrictions

and the tariff escalation," he added.

5. Ned Davis Research’s Ed Clissold

suggests

this is not a normal stock market correction.

He believes U.S. stocks have already entered a bear market.

"If you take this as a typical bear market, not

associated with a recession, it's going to take you down around 20 percent —

maybe a little bit more," the firm's chief U.S. market strategist told

CNBC's "Futures Now" last week. "That's what we need to be

thinking about over the next several months."

Mr. Clissold tweeted on Wednesday: “Reset your

clocks. Tuesday was a 21:1 down day, negating the 11:1 up day on 11/28…” He later clarified that by replying to a

question from a Twitter follower: “Advancing volume/declining volume. The

volume of all stocks that were up on the day vs the volume of all stocks that

were down on the day.”

6. Finally, we

quote from the always enlightening Credit Strategist (December

9, 2018 edition), written by colleague Michael Lewitt:

We are most

likely entering a bear market. Real interest rates are still negative, but they

are approaching positive territory as measured by official government

statistics. That still leaves them negative in the real world, but markets

won’t see them that way. Further, as Raoul Pal convincingly argues in his

invaluable Global Macro Investor, financial conditions tightened significantly

over the last 24 months. The housing market is starting to look green around

the gills, something to watch out for in 2019. Highly leveraged corporations

(much more highly leveraged than a decade ago) will focus on their balance

sheets in the year ahead as higher rates start to bite (skyrocketing Libor is a

particular problem) – we are already seeing big

outflows from bank loan ETFs and new syndicated loans are struggling in the

market. A bear market will spell big trouble for the credit markets (and low

oil prices will hurt as well) and corporate bonds do not offer attractive

risk-adjusted returns and should be avoided – short-term Treasuries are much

more attractive now. It has been a great time for idiots, but the time for

idiots is over. You better make sure you have someone smart managing your money

or you will have less of it when the smoke clears. From now on, thinking is

required.

As for recommendations, Michael writes: “I offer very

few long recommendations because I expect the market to drop double digits in

2019 and if that happens few stocks will do well.”

Curmudgeon

Comments:

We are actually very surprised by the timing of the

current stock market decline, which is happening at the most favorable

(BULLISH) seasonality of the year- from December 1st to January 10th.

We’ve twice written

that the period following U.S. mid-term elections has been extremely bullish.

Once again:

“Leuthold Group found that since 1942, the mid-term

election year’s six-month window,

beginning in November of the mid-term year and extending through April of the

pre-election year, has seen an average un-annualized S&P 500 total return

of +17.2%. Indeed, none of the 19 six-month windows in this study saw a

total return LOSS. That’s impressive!”

Expect a lot more rhetoric and outcries for the Fed

NOT to raise short term interest rates in 2019 after their expected December

2018 25 bps hike in the Fed Funds rate.

That might put a temporary floor under the market and stimulate a rally

which is likely to fail to make new all-time highs. For those so inclined, that would be a great

short selling opportunity!

Closing Points

to Ponder from Michael Lewitt:

Our colleague reminds readers that bear markets destroy

the profits gained during bull markets and cites FAANG stocks as examples.

In the December 2018 Credit Strategist, he notes that stocks are not as cheap as they

look:

“While the so-called forward earnings multiple on the

S&P 500 dropped to around 15x in November, this earnings number is inflated

by bogus non-GAAP adjustments that inflate them by 20-30%. The real forward

multiple is closer to 20x and renders stocks far from cheap by any measure. But

valuations don’t seem to matter much to investors these days since they remain

stunningly ignorant about what they own in their ETFs and other passive

strategies that relieve them of the trouble of thinking. The market was led by

FAANGs which rose by $1 trillion and fell by $1 trillion while the financial

media cheered and then wept. Earnings peaked in 2Q and 3Q18. Whatever is going

on in the market, it is no longer investing. And it ends in tears.”

………………………………………………………………………………………………………………………………

Good luck and till next time…

The Curmudgeon

ajwdct@gmail.com

Follow

the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2018 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).