U.S.

Corporate Tax Cuts Boost a Market Dominated by New Era Thinking

by the Curmudgeon with Victor

Sperandeo

2017- An

Incredibly Good Year for Stock Market Bulls:

Barring any last week of 2017 sell-off, the MSCI World stock index is set to

record its first ever year of posting a positive total return in EACH and every single month this year. It has had a remarkable sequence of 14 months

of positive returns.

In the U.S.,

the S&P 500 is up 22.3% year to date and has gone almost 14 months since

the last 3% correction ended on November 4, 2016. [Credit Suisse noted that Tech and Internet

Retail stocks contributed more than 40% of the market's total return in 2017.]

Currently,

the S&P has a Shiller P/E

of 32.56, which is twice the historical median of 16.15.

The Russell 2000

trailing 52-week P/E is 123.89, despite a forward P/E forecast of 18.6

exactly one year ago.

The Russell

2000's current P/E is more

than twice what it was at the December 1999 and 2007 market tops (each

followed by a ~50% bear market decline).

-->That

implies that if the small cap index of 1989 stocks declined by 50% it would

still be HIGHER than it was at previous bubble market tops!

Analysis of

U.S. Corporate Tax Cuts:

How can one

account for this extraordinary up move in U.S. equities, with seemingly no

downside? Besides the excess liquidity

created by global central banks, the promise of corporate tax cuts has played a

huge role. Indeed, the U.S. equity

market has been propelled upward each and every day in

2017 there was talk or a bit of progress on tax reform. Finally, it came to be. This week, the GOP's hugely unpopular tax

bill was passed along party lines, with the corporate rate cut from a

(misleading^) headline rate of 35% to 21%.

^ It's

misleading because few U.S. corporations actually pay

the 35% top tax rate as noted in the analysis below.

…………………………………………………………………..

At first look,

this would imply a significant boost for U.S. corporate earnings. However, stock market bulls and cheerleaders

forget to note that actual U.S. corporate tax rates have been significantly

lower than 35%.

Top-down

numbers, compiled by Society General (SoGen)

bank, using actual tax revenue from the BEA national accounts, suggest that the

effective U.S. corporate tax rate actually paid is

already at 21% on average and much lower than that for large multi-national

companies. That confirmed SoGen's bottom-up calculations using cash tax paid from

company reports and account cash flow statements.

Note the SoGen analysis doesn't count the much lower (or zero) tax

rates U.S. corporations have on overseas profits (e.g. Apple has $252.3 billion

in overseas cash- up from $31 billion in 2010).

SoGen's Arthur Lapthorne:

“So are these tax cuts priced in?

We'd argue that every bit of good news looks priced in. Median U.S. stock

valuations have rarely been higher on both a forward PE and EV/EBITDA basis and

valuation dispersion remains tight in all but a few sectors. To argue for a

re-rating seems ambitious. But there has nonetheless been a clear spike in out performance in recent weeks in stocks with higher tax

rates. And perhaps this is the real story - one of rotation. But where to?

Value is not cheap and suffers from balance sheet risk. Growth stocks are clear

losers as they pay relatively little in tax and will have bills to settle...”

New York

Times: In

Tax Overhaul, Trump Tries to Defy the Economic Odds, by Patricia Cohen :

Goldman

Sachs projected that the GOP tax bill will add just three-tenths of 1 percent

of growth in the next two years, before its impact peters out. The firm’s annual growth estimate of 2.5

percent for 2018 matched the one issued this week by the nation’s central bank,

the Federal Reserve, while the latest median Wall Street forecast hovered close

by. And in 2019, growth is expected to drop to 1.8 percent, Alec Phillips,

chief United States political economist for Goldman, said Wednesday after the

Senate vote.

Trey Reik of Sprott:

We believe

the corporate focus of Trump tax cuts is misguided for two reasons.

First, lowering corporate tax rates will only exacerbate the economic

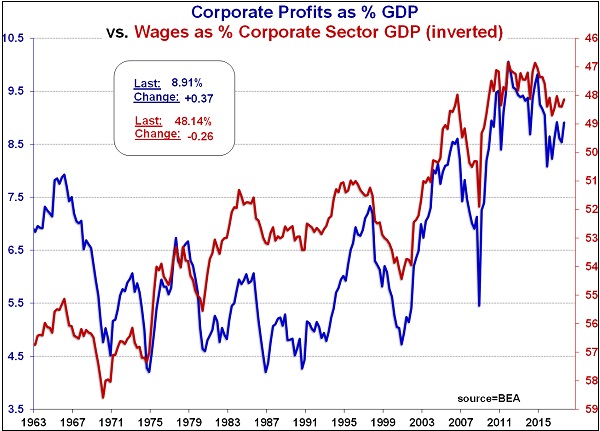

stratification already plaguing the U.S. economy. As shown in the graph

below, corporate profits as a percentage of GDP hover near all-time highs

precisely as wages as a percentage of GDP have dwindled toward historic lows.

Corporate Profits Hover Near All-Time

Highs (1963-2017)

Source:

Meridian Macro; Data from 1963-Q3 2017.

Given how far the economic pendulum has

swung in favor of capital-over-labor in recent years, is this really the right

time to pursue economic growth through tax cuts on record corporate profits?

Second, there is precious little

supporting evidence that reducing corporate tax rates and offering a tax

holiday on overseas profits will actually stimulate

either incremental capex or increased hiring. One particularly poignant

rebuke of the Trump administration’s tax-cut reasoning occurred at a gathering

of the Wall Street Journal CEO Council on 11/16/17. With White House Economic

Council Director Gary Cohn seated on stage, a WSJ editor asked a room of

100-or-so CEOs for a show of hands, “If the tax reform bill goes through, do

you plan to increase your company’s capital investment?” When virtually no

hands were raised, Cohn nervously blurted out, “Why aren’t the other hands up?”

This awkward scene quickly went viral as a vivid demonstration of how out of

sync the Trump tax plan is from common corporate priorities.

During the past eight years, zero

interest-rate policy (ZIRP) and related productivity declines have

decimated corporate capex in favor of debt-fueled share repurchase. From

the equity market lows of Q1 2009 through the first half of 2017, the corporate

sector had repurchased 18% of total U.S. equity market capitalization, while

institutional investors had liquidated 7% of total equity market cap. These stock

repurchases were funded almost entirely through the issuance of low-coupon debt

in a ZIRP world!

…………………………………………………………………..

A New Era

where the old investment rules no longer apply:

Meanwhile, we

continue to see market behavior characterized by “new era” thinking:

- “Buy high, sell higher.”

- “Buy higher still, never sell.”

- “Buy every dip, which is a blip in a never-ending

bull market.”

In our last

Curmudgeon post, we

reported that Savita Subramanian, Chief .U.S Equity

Strategist at BoAML no longer uses the Graham and Dodd value investing

textbook, which was her “bible” while studying finance at Columbia University

Business School.

There have been

many never ending, non-stop bull market remarks we've read from senior market

analysts. For example, “Bull

Market Is Continuing With No Sign Of A Major Top In Sight.”

“The stock

market (advance) might be slowing down, but there's no stopping in sight” [16

Amazing Stocks to Trade in This Unstoppable Bull Market.]

For good

reason, stock market analysts have been mesmerized by this seemingly never-ending

bull market grinding higher day after day after day. It's like an orgy that never ends.

While they may

be right for now, we submit the following counter quotes for the reader

to ponder and reflect on:

"The four

most dangerous words in investing are: 'this time it's different'" Sir

John Templeton

Curmudgeon

comment: But this time (from Feb 16, 2016 to date) the

equity market actually appears to be different--at

least anything I’ve seen in 55 years of market watching!!!

…………………………………………………………………..

“How does one

reduce the margin of error while recognizing that investments do, of course

go down as well as up? The answers are not absolutely clear cut but they certainly include refusing to compromise by

subtly changing a question so that it shapes the answer one is looking for”

Peter Cundill.

.

Curmudgeon

comment: Yet from the February 16, 2016 correction

low, stocks never have gone down by more than 5% and not even 3% since November

4, 2016.

…………………………………………………………………..

“High levels of

greed sometimes cause new-era thinking to be introduced by market participants

to justify buying or holding overvalued securities. Reasons are given as

to why this time is different from anything that came before. As the truth is

stretched, investor behavior is carried to an extreme. Conservative assumptions

are revisited and revised in order to justify even

higher prices, and a mania can ensue” Seth Klarman.

…………………………………………………………………..

"Some

grasp of history's abundant lessons becomes especially relevant in the

examination of the goings-on in the capital markets where emotions,

particularly at extremes, run high - and reason often is overwhelmed. Careful study of the past would suggest that

it's quite appropriate to argue that there are no "new eras" in

finance, only "new errors" Frank Martin.

…………………………………………………………………..

Often investors

invent a thesis to justify a trend: "Outsized returns can be realized by

purchasing growth stocks regardless of their PE ratios because their PE ratios

are not relevant over the longer term." Or "New Economy internet

stocks will continue to grow exponentially - and Old Economy stocks are dead

and should be sold." In my opinion, booms become particularly dangerous

when the theses that justify the booms generally become uncritically accepted

by investors. Then, investors are prone to become complacent and to accept the

excesses as new norms. History books are full of booms and busts, and booms and

busts likely will continue to occur because of the proclivity of humans to

become uncritical participants in trends and fads" Ed Wachenheim.

…………………………………………………………………..

"New eras

usually ride into town on the back of a horse mistaken for a golden stallion,

transformed momentarily by the brilliance of the afternoon sun. Incredulous onlookers (investors) are

thinking riches, when all that's left when the illusion fades is manure."

Frank Martin.

……………………………………………………………………..

Victor's Comments:

The major take

away conclusion from the last nine years (the so called “New Era”) is this:

Not a single asset

price in the world is honest or accurate.

This is due to global Central

Bank planning and manipulation, i.e. QE or printing vast amounts of paper

currency, negative short-term interest rates, and 5,000-year lows on long bond

interest rates (some are still negative!).

That has distorted all other asset prices and effectively means every

investible asset in the world is mispriced. That includes: Real estate,

Equities, Bonds (from governments to junk), Bitcoin (and other crypto

currencies), Art work (especially master paintings), etc. are not what they

seem.

Central Banks not only have

set-up the world for an Armageddon like bust, but in the process, they've

crushed many financial industries. For example, the hedge fund industry that

typically charges 2% management fee +20% (or more) incentive fee is now

becoming extinct. How can you justify paying 2+20% for a long/short equity

hedge fund when the shorts virtually never go down.

(Shorts often cause huge losses when they're covered). Very few short sellers are fundamental

managers who can win in this new game. The only way is picking frauds that go

out of business, which is very rare indeed.

The trend following commodity

(CTA and managed futures) business has been decimated. For the last 5 and 10 year rolling periods of

“economic recovery/growth” (ending in 2016), real U.S. GDP averaged 2.16% and

1.3%, respectively. [Note that the 2007-2016

period included the 2008-2009 recession].

-->Those are the lowest

economic growth numbers in the history of the U.S. from 1789.

Inflation, as measured by the

CPI, is highly correlated to commodities.

The CPI had the lowest 5 and 10 year rolling periods since 1961 at1.36%

and 1.81%, respectively. If you own a CTA managed account or managed futures

fund that uses a trend following program you have experienced a big

disappointment in performance, especially if the CTA program doesn't use stock

indexes.

[Curmudgeon comment: Many trend following futures funds have been down by double

digits annually the last few years. I

owned several that were liquidated due to severe drawdowns of 50% or more.]

In closing, it appears financial

markets are very calm and orderly today and the bull move in U.S. equities will

go on indefinitely (“no top in sight,” say the market analysts/pundits). And

that's independent of sky high valuations which keep going higher (just check

any graph of P/E ratio's). We think the bull move

will suddenly END one day without any classical topping action.

The excesses in many

markets will all be corrected very quickly when an unknown event (e.g. a

Saudi/Iran war?) upsets the ability of the central banks to CONTROL the

markets. At that point in time, every investment market

will become massively volatile and buy and hold forever will be a very bad

investment strategy.

Curmudgeon’s new email address: ajwdct@gmail.com

Good luck and till next time...

The Curmudgeon

ajwdct@gmail.com

Follow the

Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures markets,

risk parameters and other factors.

Copyright © 2017 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).