Global

Earnings Recession and a Grinding Bear Market

by the Curmudgeon

Introduction:

This is a follow up to

Sunday’s Curmudgeon post which expands and amplifies the ongoing profits

decline. Various sources are cited but

no opinions are expressed, leaving it to the reader to form conclusions.

We repeat our quote from FactSet:

“For Q1 2016, the estimated earnings decline for companies in the S&P 500

is -8.5%.”

Yet the profit downtrend is not

just confined to the U.S. As explained

below, it’s global. That’s bad news for

the world economy and especially for equity markets, since P/E ratios are

already quite high, as noted several times by Victor.

Global Decline in Earnings Explained:

Researchers at the Institute of International Finance (IIF),

a Washington DC-based association that represents close to 500 financial

institutions from 70 countries, publish a monthly report titled "Capital

Markets Monitor." The April

issue attributes the global decline in earnings on poor productivity

growth, weak demand and a general lack of pricing power. U.S. companies also

are being squeezed by rising labor costs as they add employees to their

payrolls without any increase in output per man hour.

"In the past, if you had

poor performance at home, you could recoup and compensate for that with

overseas investment," IIF executive managing director Hung Tran said in an

interview

with Bloomberg.

"But if you suffer

declines in profits domestically and internationally, you tend to retrench,"

Tran added. He put the chances of a U.S.

recession within two years at around 30 to 35% due to the earnings slump, up

from 20 to 25%.

The prolonged downturn in

profits, which we highlighted in our previous post, makes Tran and his

associates skeptical that the recent rebound in global stock markets can last

as per this quote from the April Capital Markets Monitor report:

“After

falling sharply around the turn of the year and reaching bear market territory

in mid-February, global equity markets have staged a strong rebound, regaining

nearly half of the 20% decline between May 2015 and mid-February 2016. At this

juncture, it is important to judge whether the rebound can last. We remain

skeptical: in our view, this year’s market fluctuation represents a volatile

trading range against the backdrop of a slow and fragile global economy.”

From the graph below, we see

that U.S. corporate profits formed a double (or triple) top in 2014 and have

been declining ever since.

The forward earnings outlook, which seems to be always over estimated

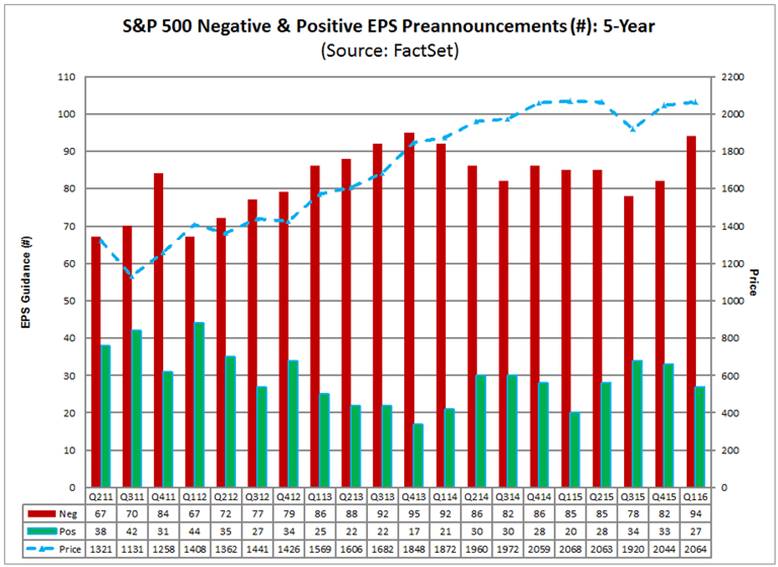

by stock market analysts, doesn’t look very good. During the current “earnings season,”

pre-announcements have been the second-worst over the past decade, as shown in

this graph:

Chart courtesy of FactSet

The Information Technology

(25), Consumer Discretionary (18), and Health Care (17) sectors have the

highest number of companies issuing negative EPS guidance for the first

quarter, according

to FactSet.

Slow Grinding Bear Market Rally:

Robin Griffiths, Chief

Technical Strategist at The ECU Group, thinks we’re in a bear market with a low

coming sometime in 2017. In an interview

with Financial Sense, he said:

“Everything suggests to me

that the world is in fact in a bear market and that what we're having is the

end of the first bear market rally… According to my work, the final low of the

bear market is not now—it's not even this year. It'll be next year and it will

be quite a bit lower than we are now in virtually all markets.”

Later in the interview,

Griffiths said global equity markets are in a slow grinding bear:

“The economies are cooling

down some more than others and Janet Yellen doesn't want to crash things so the

notion that we could have interest rates returning to what used to be normal

now or anytime soon is...well, it really can't happen. It's not going to be

allowed to happen. But because of valuation levels I use the expression of a

'slow-grinding bear'. I think that is the high probability. The possibility of

a crash is much greater from bubble territory but the broader market is not in

bubble territory—it's just expensive. And it's had a very long-lasting bull,

slightly kept alive on steroids of zero interest rates...”

………………………………………………………………….

Anomalies in U.S. Stock Market Rally:

In an April 4th

post (subscription required), Dow Theory

Letters’ Matthew Kerkhoff wrote:

“The

six-week rally that we find ourselves in has given way to a few interesting

developments. First, by not providing any type of meaningful correction, this

rally has refused to provide a pattern of higher lows and higher highs – the

telltale signal of a bullish trend.

Instead,

it’s been a one-way momentum push higher that’s resulted in the most recent low

being the lowest-low we’ve seen in quite some time, while the most recent high

(back at the end of February) was obliterated as the market soared higher.”

That said, Mr. Kerkhoff notes that market breadth has been bullish

recently. He said that that

participation in the current rally “has been very strong with the NYSE A-D line

soaring all the way back up to its previous highs.” That can be seen in the chart below:

Dow Theory Letters – Bear Still in the Box:

We conclude with a quote from

the April 6th Dow Theory Letters (subscription only):

“Based

on Dow Theory, the primary trend of the stock market remains bearish. The bear market

was confirmed last August when the Dow Jones Industrials and the Dow Jones

Transports both fell sharply, hitting new lows. Stocks then rebounded in the

last quarter of 2015. This was followed by another steep decline as 2016 kicked

off the new year.

In

January, 2016, the Dow Transports broke clearly below its August low. And in

February, the Dow Industrials followed, also closing below its August low,

thereby reconfirming the Dow Theory bear signal.

Okay,

but what about the big up-moves since then? So far, this has been a secondary

up-move within the primary bear market. This week the Dow Industrials hit a new

high for this up-move, but it was not confirmed by the Dow Transports. We'll be

watching to see if this divergence continues. If it does, it could be a sign

the market is indeed losing momentum. Plus, stocks are currently overbought,

suggesting the upside is limited for the time being.

We'll

soon see how this unfolds. But in the meantime, continue to maintain some

caution, keeping in mind that the primary trend is still bearish. And as we've

often pointed out, the primary trend is the most important.”

Good luck and till next time...

The

Curmudgeon

ajwdct@sbumail.com

Follow the

Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974

bear market), became an SEC Registered Investment Advisor in 1995, and received

the Chartered Financial Analyst designation from AIMR (now CFA Institute) in

1996. He managed hedged equity and alternative (non-correlated)

investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2015 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).