Victor’s

Perspective on Markets, the Economy and the Fed

by Victor Sperandeo, edited by the Curmudgeon

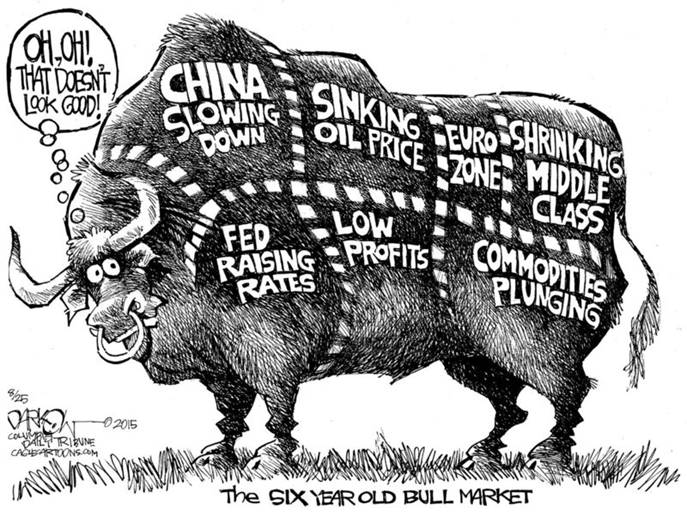

US Equity Markets:

The decline began on August 19th at the opening

after the WSJ reported that the IMF would "NOT" grant China

Reserve Currency status for at least one year.

Reuters ran a similar news story titled IMF

Defers Decision on Adding Yuan to Basket of Reserve Currencies. That

new reality caused the Shanghai Composite index to fall from ~ 3800 to 2850

from August 20th to 26th which was the catalyst for a

cascade fall in global equity markets.

Our July 12th Bear in a China Shop

post concluded:

"2. If China does not get the increased reserve

currency/ADR gift from the IMF, the payback for their U.S. hack attack and

their island building will be very expensive indeed.”

Indeed, the US told the IMF to "not “grant China

reserve currency privilege. Payback had been harmful to all equity markets –

until NY Fed President Bill Dudley expressed reservations on raising rates at

the September 16-17, 2015 FOMC meeting.

That remark sparked a huge rally in US stocks this Wednesday and

Thursday. It's important to note that

Mr. Dudley was a former VP at Goldman Sachs.

I wonder if Goldman made money when Dudley said raising rates

"looks less compelling?”

My view of the US equity markets is that they will stay

stable, with an upward bias, until the September FOMC meeting. I expect the Fed to "not" raise

rates at that meeting, which will then cause a rally that leads to lower 2015

highs for the popular stock market averages. My guess is that three days after

the Fed postpones the long talked about rate increase, the stock rally will

end.

That should start the 2nd bear market leg

down. Since 1896, the 2nd leg

of a primary stock market decline (according to my DOW THEORY classifications)

ranges between 20%-to-40%. If the Fed does raise rates, then the down leg will

start around that time without a "3 day" rally.

The US Economy:

On Thursday, US 2nd quarter GDP growth was

revised sharply higher to 3.7%. Why not?

That was only +61% -- above the 1st estimate! What's a slight miss within The Bureau of

Economic Analysis (BEA) - a government agency?

Shadow Stats' John Williams provides

some evidence its bunk by showing the stagnant activity in GDI (Gross

Domestic Income) - "the practical equivalent to GDP." The balance of Consumption (GDP) and Income

(GDI) was +3.75% versus +2.52% (or GDI quarterly +.63 x's 4). This certainly

reinforces the constant cynical (but realistic) belief of manipulated

government reporting across the board.

[Note: the CURMUDGEON couldn't agree more with that!]

Gold:

The yellow metal has come off its lows, but it's still in a

downtrend. The higher reported GDP 2nd quarter number, plus the big

2 day rally in stocks has capped the up move in Gold. The precious metals

will only become profitable when inflation returns (which is not visible in the

near term) and/or if real chaos becomes a constant. Something the Fed can't control or fix with

mere words by a prominent Fed official.

Side Comment: Think about the power to move $1 trillion or

more in markets on a “maybe” Fed comment that's pure rhetoric? Do you think our

Founding Fathers had this in mind when they went to war against King George to

create a nation of laws i.e. a Republic? But this is how the game is played

when you control a printing press with no laws. The endgame will be atrocious,

as manipulation has no fundamental foundation.

Bonds:

US Treasuries played their typical “flight to safety” role

and rallied in price as stocks tanked. However, bond traders did not pay any

attention to the +3.75% 2nd quarter GDP revision (because it was

created by the minions at the BEA). The

30 year T-bond yield declined from 3.24% on 6/24/15 (or 147.16 in price) to

2.72% (or 160.30 in price) on 8/24/15 for a 9.2% increase!

Side Comment: Bonds have fooled most economists,

market analysts and fixed income portfolio managers, as the Keynesian gambit

(US fiscal and/or monetary policies) has been a dismal failure in that it has

NOT stimulated economic growth. Yet

the US government or Fed policies don't change? It's not about economics,

but rather a POLITICAL AGENDA that is about changing America from a Capitalist,

free market, pro-growth country to a centrally planned Collectivist

society. The cost of this conversion has

not yet been paid, in my humble opinion.

The Dollar:

The greenback keeps bouncing off the DXY support at

93.5. Of course, the dollar moves up and

down based on what the Fed will do with interest rates. Since they haven't yet decided on a Sept.

rate rise (as per Fed Vice Chair Stanley Fisher at

this weekend's Jackson Hole WY Fed conference) the DXY will continue to trade

in a narrow range. It's moved between

98.00 and 93.5 since this past April.

The recent bounce in the dollar was likely due to the upward

revision in 2nd quarter GDP.

Evidently, currency market participants were impressed with the

incredible strength in the US economy? That

AGAIN raised the possibility of a Fed rate increase at their Sept 16-17

meeting, which would be BULLISH for the greenback. Hence, the dollar see-saw

goes up and down. The Fed will raise rates as soon as they are able to get away

with it, and therefore the DXY will trade in a fairly narrow range till it

does.

Crude Oil (Guest commentator Brent Berarducci):

The steep downtrend in crude oil (see chart in Monday's

CURMUDGEON post) was interrupted this week when Oct Crude Oil

futures rose an astonishing 16% in two trading days to close the week at

$45.22. While sharp rallies in bear

markets are to be expected, this was the largest move in years and occurred

with no meaningful change in energy fundamentals or the geopolitical

background. In a report to clients, I

examine if there are reasons to consider this move a trend reversal or just a

volatile upward correction in a continuing downtrend. Please email me if you are interested in the

report: brent@blacklioncta.com

The FED:

Recall the purpose and function of the Fed: it directly controls the US monetary system

to pursue two primary mandates: to 1] promote price stability and 2] ensure

maximum sustainable employment.

Price stability is usually interpreted as low and stable inflation. The impetus for this explicit objective was

the highly volatile inflation of the 1970s (Curmudgeon: thank you Paul

Volker!).

Permit me to quote from Fed elites via an August 28th

WSJ article titled: Central

Banks Rethink Inflation:

Central bankers aren’t sure they

understand how inflation works anymore. Inflation didn’t fall as much as many

expected during the financial crisis, when the economy faltered and

unemployment soared. It hasn’t bounced back as they predicted when the economy

recovered and unemployment fell.

The

conundrum challenges much of what central bankers thought they understood about

the world, as well as their ability to do their job. How will they know when to

raise or lower interest rates if they’re unsure what causes consumer prices to

rise and fall?

“There is definitely less confidence, a lot less

confidence” about how inflation works, James Bullard, President of the Federal

Reserve Bank of St. Louis, said in an interview here Friday."

This is a shocking surprise comment! The Fed's Bullard evidently sees the world in

a Keynesian vacuum. So now the Fed

admits they don't have a clue of how to do their jobs? Yet it is full speed

ahead!

Curmudgeon Comment: Not much attention

has been given to an August 18h WSJ editorial by Minneapolis Fed

President Narayana Kocherlakota, who is also a member

of the FMOC. In Raising

Rates Now Would be a Mistake, he wrote: “Given the prevailing economic conditions,

higher interest rates would push the economy away from the FOMC’s economic

goals, not toward them…The U.S. inflation outlook thus provides no

justification for policy tightening at this juncture. Given that outlook, the

FOMC should ease, not tighten, monetary policy by, for example, buying more

long-term assets or by reducing the interest rate that it pays on excess

reserves held by banks. Along these lines, the board of directors of the

Minneapolis Fed has for the past few months been recommending a reduction in

the interest rate that the Federal Reserve charges banks for discount window

loans.”

History Lesson:

Economist and philosopher Friedrich von Hayek explained why

Central Planning can NEVER be a success.

In a 1945 essay titled: The Use of Knowledge

in Society, he states:

"The peculiar character of

the problem of a rational economic order is determined precisely by the fact

that the knowledge of the circumstances of which we must make use -never exists

in concentrated or integrated form, but solely as the dispersed bits of

incomplete and frequently contradictory knowledge which all the separate

individuals possess. The economic problem of society is thus not merely a

problem of how to allocate "given" resources—if "given" is

taken to mean given to a single mind which deliberately solves the problem set

by these "data." It is rather a problem of how to secure the best use

of resources known to any of the members of society, for ends whose relative

importance only these individuals know. Or, to put it briefly, it is a problem

of the utilization of knowledge which is not given to anyone in its

totality."

This is why ONLY free markets can be the singular means to

efficient ends, as no one (especially not small cabals) have the KNOWLEDGE of

the many that make a market or the desires and wants of a population of a

nation. Those that attempt to do

otherwise (i.e. to circumvent free markets) are described by Hayek as: "Intellects whose desires have

outstripped their understanding."

Good luck and till next time…

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2015 by the Curmudgeon

and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).