China’s

Stock Market Wild Ride Has Global Implications

by the Curmudgeon

Note: This is

the 1st of a 2 part Curmudgeon series on China's stock markets. The 2nd article was written by

Victor Sperandeo and edited by the Curmudgeon.

It can be accessed here.

Backgrounder:

China’s combined stock markets in Shanghai and Shenzhen rank

second in the world in market capitalization behind the New York Stock Exchange

(NYSE), and in the top 10 in terms of number of listed companies. So what happens there has huge implications

for global equity and commodity investors (China has been the #1 demand driver

of commodities for many years).

Trading volume on the Chinese stock market is four times

bigger than on the NYSE, with 3% of the market by value turning over every day.

On the NYSE, that number is 0.3%.

Despite their large size and huge volume, China’s two stock

markets trade like the wildest emerging markets characterized by huge

volatility spikes and big boom/bust cycles, which are driven by fast-trading

individual speculators and heavy involvement (pro and con) from the government.

Unlike every other major stock market in the world, China’s markets are almost completely

closed to foreign investors.

According to the Economist:

“China’s repressed financial system helped inflate the bubble by pumping money into the stock market. Banks pay interest rates well below the level that would be expected without regulatory caps, and China has yet to develop alternatives for savers looking to park their cash elsewhere. The hunt for good returns has over the past decade sparked investment frenzies in property, stamps, mung beans, garlic and tea. Steps to give investors better access to foreign markets and to free up bank rates all aim in the right direction but progress has been halting. Equities were as ripe for a bubble in 2015 as they were in 2007, the last time China experienced a stock market frenzy.”

Chart Courtesy of the Economist.com

As market participants are well aware, China had a big

blow-off/ spike top on the upside and then sharply reversed into a violent bear

market. At the low, the Shanghai stock exchange was down more than 32% and

Chinese “investors” (mostly individuals rather than institutions) were in panic

mode.

How bad was China’s stock market crash? By the end of July 7th,

trading in over 90% of the 2,774 shares listed on Chinese exchanges were

suspended or halted. Shares have fallen by a third in less than a month, wiping

out some $3.5 trillion in wealth, more than the total value of India’s stock

market.

Chinese government officials have been instituting all sorts

of gimmicks in an effort to halt their stock market decline. For instance,

large investors who owns 5% of a stock are not allowed to sell that stock. They also banned short selling, froze all new

IPOs and told state owned companies to buy stocks. For the last two days, the Chinese authorities

have been able to stop the decline as their markets rallied Thursday and

Friday.

On Thursday, the Shanghai Composite rose 5.8% to 3709.33,

after losses in eight of the previous 10 trading days. It advanced 4.54% on

Friday. The smaller Shenzhen market rose

3.8% on Thursday and 4.1% on Friday. The

small-cap ChiNext board, which has shed some 38% from

its June highs, rose 3% and 4.1% on Thursday and Friday, respectively.

Even with the two day rebound, $3.1 trillion in market

value, (much of it financed with borrowed money) has been erased since

mid-June. Many worry about the damage to the Chinese economy, particularly if

stocks continue to fall. Consumer confidence could suffer, weighing on the

country’s growth and on economies elsewhere that depend on exports to China.

Going forward, if China stocks are in a primary bear market,

no amount of government interference will turn the tide to bullish. There's a legitimate concern that China’s

sickness will be contagious and global stocks and commodities will follow in

their own major bear markets.

According to an article in Saturday's NY

Times, China is the world’s

largest importer of commodities like crude oil1 and copper2,

making many developing countries dependent on China’s continued economic

health. China is also the largest market for cars, flat-panel televisions and

Apple iPhones

…..............................................................

Notes:

1. Time Magazine and the Financial

Times each state that China is now the #1 importer of crude oil in

the world, surpassing the U.S.

2. Copper hit a six

year low this week on concerns China's stock market meltdown would adversely affect

their economy.

…..............................................................

What Makes China's Stock Market Different?

There are at least three items that make China’s markets

unique.

- The government plays a heavy role

in the market.

- Small investors ultimately control

the trading.

- The Chinese stock market has

TOTALLY decoupled from the Chinese economy (at least in the last two years

when the stock market soared while the economy weakened).

Isabel Hilton of the UK Guardian newspaper wrote:

“It has been a traumatic month for China’s small investors,

two-thirds of whom, according to a survey last year, have not finished high

school. These are largely people who have prospered modestly in the past

three decades. Some are retired, others straddle the uncertain worlds of petty

trading, agriculture and seasonal migrant labour.

Some will still be in credit, but others, especially those who invested in

hard-hit ChiNext, China’s equivalent of the Nasdaq, will have lost heavily. Many more have lost

confidence.”

Short seller Jim Chanos told the

Wall Street Journal: “I have no idea

where equity markets will trade, but the Shanghai market is not the best

barometer” of the declining health of the country, he says. The Chinese

economy “has been on a five-year glide path downward” that he expects will

continue. “The omnipotence of the

Communist party has taken a hit and that’s a real cost,” he says.

“The stock market problem is a heart attack (for China's

leaders),” said Dong Tao, the chief Asia economist at Credit Suisse. “For the

time being, their overwhelming priority is to stop the bleeding and control

systemic risk.”

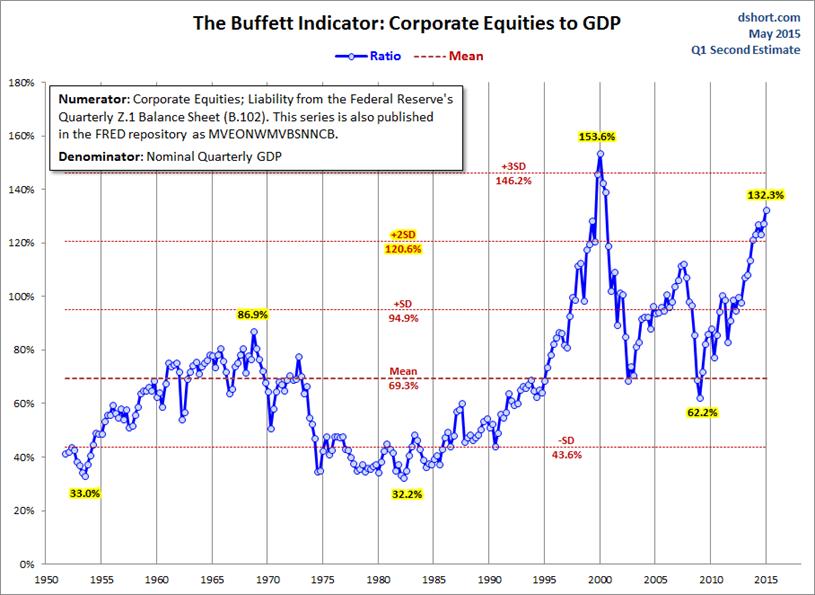

Chinese Stock Market vs China's Economy:

Despite its huge size, the stock market still plays a small role in China's economy. The free-float value of Chinese market (the amount available for trading) is just about a third of GDP. Compare that with more than 100% in developed economies and 132.3% in the U.S. according to this graph.

Chinese shares tend to rise and fall on sentiment and

government actions, rather than economic fundamentals, and despite all of the well-publicized

drama they create by trading shares, a relatively small proportion of China’s

vast population actually “invests” in the market. Yet China's economy has been deteriorating

for several years and a primary bear market in equities could certainly worsen

that decline.

China’s corporate and local government debt totals an

extraordinary 280% of GDP, and has been growing twice as fast as the economy

for more than a decade. The property market is depressed and overstocked, and

confidence is fragile. China’s future depends on the Communist party’s capacity

to make its state capitalist model leaner and more efficient.

China’s authoritarian regime is fearful that stock market

distress will lead to economic problems which might fuel political unrest. They haven't forgotten the Tiananmen Square

protests of 1989.

Shared Risk and Parallels with the Past:

Again we quote Isabel Hilton: “In a world that has come to rely on China to

keep the global economy ticking over, China’s risk is now everybody’s

risk. The current regime has turned its

back on political reform, tightening internal security and promoting a new

insistence on socialist dogma. Ironically, China’s success will hinge on how

well it can play the next round of the capitalist game. After this week, the

odds may have to be adjusted.”

The Telegraph's

Jeremy Warner notes that China today, like America 90 years ago, is

rapidly urbanizing with a growing middle class. In the 1920s, middle-class

Americans discovered margin trading, propelling the stock market to dizzying

heights reached in 1929.

“The parallels with 1929 are, on the face of it, uncanny.

After more than a decade of frantic growth, extraordinary wealth creation and

excess, both economies – America in 1929 and China today – are at roughly

similar stages of economic development. Both these booms, moreover, are in part

explained by extremely rapid credit growth. Indeed, China’s credit boom dwarfs

that of even the “roaring Twenties”. Borrowed money, or margin investing,

played a major role in both these outbreaks of speculative excess.”

Extreme Danger of Markets Propelled by Margin Debt:

Of course, we don't have to go back to the 1920s to observe excessive

margin trading in U.S. stocks. Current

data from the NYSE suggest that margin debt is higher than ever before! As the table

shows, NYSE margin debt reached $507,153 in April 2015 before

declining slightly to $499,143 in May.

Even more important is that margin debt levels are higher

than ever when compared to free cash balances in margin accounts. For several

years, the Curmudgeon has warned of the dangers of high margin debt as per this

post.

Conclusions:

1. On the dangers of excessive margin debt:

U.S. stock market pullbacks of 10% or more (which used to be

called “corrections”) could trigger serious U.S. margin calls. That might cause a stock market decline to

feed on itself and turn into a true bear market. China, Greece, or some other external event

could easily precipitate such a scenario.

2. On Gold's

recent dismal performance:

We must express profound and EXTREME disappointment that

gold (and especially gold mining shares) have DECLINED during the China stock

crash, which has been accompanied by rising geopolitical tensions and

heightened financial uncertainty (Grexit soap opera, ISIS attacks spreading

outside of Iraq and Syria, Iran nuclear talks, Puerto Rico debt crisis, etc.).

Gold's horrible performance was clearly the take-away of a

Friday WSJ article titled: No

Gold Rush as Greece and China Troubles Roil Markets.

The Curmudgeon is perplexed, astonished, flummoxed, and

blown away by Gold's poor performance in light of all the chaos and threats to

the global economy. But it's reality,

whether we like it or not!

Till next time...

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development platform,

which is used to create innovative solutions for different futures markets,

risk parameters and other factors.

Copyright © 2015 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).