Is the Stock Market Correction Over? Ask the Fed!

By the Curmudgeon with Victor Sperandeo

Market Review & Analysis:

The S&P 500 surged 4.12% this week, nearly erasing its October loss. The NASDAQ and other popular averages also rose strongly. The benchmark S&P 500 index is now only 2.33% from its record close on September 18th. Just seven sessions ago, the S&P hit a six-month low of 1,821 – below the level at which it ended 2013, and marking a 9.8% retreat from September’s record intraday high.

More stable market conditions were also illustrated by a sharp fall in the CBOE VIX volatility index from a three-year high above 31 at the height of the turmoil to 16.5 – well below its long-term average of about 20.

The chart below shows a percent-off-high calculation to illustrate the drawdowns greater than 5% since the trough in March 2009.

Chart Courtesy of Doug Short

As you can see from the above chart, the last 10%+ drawdown ended over three years ago. Hence, the Sept-Oct decline doesn't qualify as an "official" correction. Is it over now and has the bull market resumed? Were there any fundamental underpinnings to the market's advance off the October 15th lows?

We maintain that nothing has fundamentally changed from the time the correction began till this week's huge snap back rally. All the global economic and geo-political problems have not been resolved while fear of Ebola spreading is still a legitimate concern, especially in NYC. Let's now examine what others say about this issue.

Other Voices:

“Whether this is just a technical correction higher or a real turnaround depends on a number of issues, not least on how much the global economy is slowing down,” said analysts at Danske Bank. “This in effect will very much depend on how the U.S. evolves over the coming quarters.”

In an October 23rd note to clients, Philip Gotthelf reports that concern over deflation is rising in Europe and the U.S. At the same time, The Wall Street Journal reports that Argentina is rationing consumables including food. CNBC reports that the precipitous decline in crude oil and other energy products is problematic. The picture among analysts appears confused. Low energy is good for consumers, but bad for oil companies. Oil companies spend money and hire people. Base metals have eased because of supply-side overcapacity and demand-side saturation. None of that augurs well for future economic growth or corporate profits. While the stock market woke up and started to take notice of these trends in September through mid-October, it's now back to "all is well with the world."

Bank of America- Merrill Lynch global interest rates and currency strategists (via the WSJ): “In 2010 and 2011, the Fed stepped in following equity corrections of 11% and 16%, respectively. Given where the market now finds itself, it may take a further 10% decline from the recent lows” for markets to begin anticipating that the Fed will restart its bond buying (QE4) to buoy markets and help prevent the lost wealth from causing broader economic problems. That would replicate how the Fed acted following equity declines of 11% in 2010 and 16% in 2011.

Richard Russell on October 23rd in a note to Dow Theory Letter subscribers: "We know that: Germany is slowing down, that their GDP is slumping. China is slipping. The world is deleveraging and deflating. We know that the Federal Reserve is deathly afraid of deflation, and is worried that with all their QE they still can't create 2% inflation...Therefore, the ultimate question of the hour and the month and the year is -- in the face of the ongoing deleveraging and deflation, will the Fed actually end QE, possibly triggering a stock market slump and higher interest rates?"

Market Manipulation by the Fed?

Victor wrote in his comments last week, that the Fed is targeting the stock market, which has prevented a 10% correction since the last one ended (mysteriously) on October 3, 2011.

Meanwhile, the Curmudgeon has been writing about the Fed

put (AKA Greenspan/Bernanke put) for years. In an August 2007 post titled What is the Strike Price For the Fed Put? we wrote: "The

Fed wants to avoid a recession at all costs- even if it bails out mortgage

lenders, hedge funds, banks, and other financial institutions."

More recently, we've opined that the Fed wants to prop up the stock market to prevent the public from worrying about a pending recession due to sharply declining stock prices (i.e. most people believe the market is a good economic forecaster of recessions -- the S&P 500 is a component of the Leading Economic Indicators*). We believe that the Fed fears that even people who don't own stock might experience a negative wealth effect and cut back on spending if the market plunges.

*NOTE: The S&P 500 is considered a leading

indicator because changes in stock prices reflect investor's expectations for

the future of the economy and interest rates.

The Curmudgeon strongly disagrees and maintains there's an almost

total disconnect between the stock market and the real economy since March

2009, because the Fed has dominated the so called economic recovery and may be

manipulating the stock market.

The Fed’s willingness to directly (through policy statements and QE) or indirectly (through its dealers or foreign central banks that buy stock index futures or index ETFs) stem a market decline dates back to the October 19, 1987 stock market crash. The Dow fell 22.6% that day after being down significantly the previous week.

Greenspan’s Fed bought $17 billion worth of bonds (a lot in those days) and declared the central bank ready “to serve as a source of liquidity to support the economic and financial system.” There were also rumors that the Fed or a pre-cursor of the Plunge Protection Team (PPT) asked large investment banks to buy stock index futures on October 20, 1987. Late that afternoon, corporations announced stock buyback programs to support demand for their stocks. That stopped the decline and stabilized prices.

The market retested its lows on December 3rd and 4th of 1987 and then started an advance which recovered all of its losses within 2 years -- an unusually short time by historical standards.

Bianco Research on the Fed and Stock Market:

“They (the Fed) are definitely in the market-manipulation business, and nothing has changed,” said James Bianco, president of Bianco Research LLC in Chicago and a longtime student, and critic, of the Fed.

“The put option is back. If the market sells off enough,

they will give us QE4,” Bianco

told Howard R. Gold.

Bianco continues: “Three times they (the Fed) put down markers they were going to end QE. In all three cases, (resulted in) -- 20%, 17%, 10% down in the stock market -- they reversed (and resumed QE).”

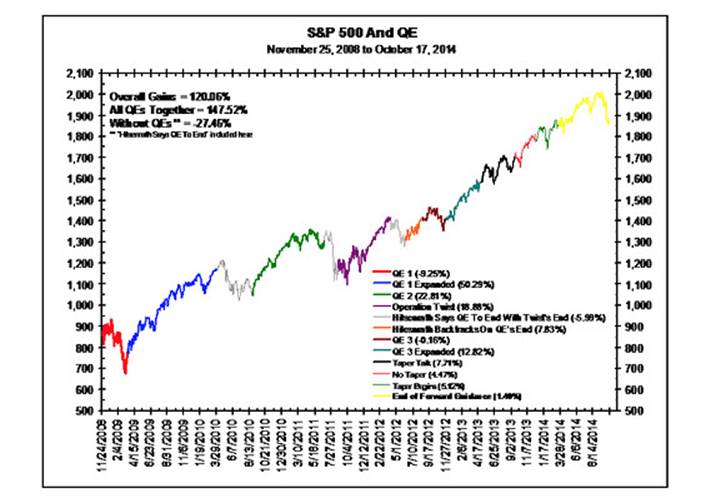

As the chart below illustrates, Bianco Research estimates

that during all the QEs, stocks rose by 147.5%. Subtracting periods of QE,

they lost 27.5%.

Chart Courtesy of Bianco

Research LLC

Bianco thinks the specter of the 1929 crash and subsequent depression still haunts the Fed. “They are afraid of the market going down and they will be blamed,” explained Bianco. If that means “guiding” the stock market, so be it, he added.

Curmudgeon's Comment: Yet the Fed does not have the authority to intervene directly or indirectly in the stock market. Its mandate is to "promote maximum employment, production, and price stability.” There's nothing that authorizing the Fed to prop up stocks or make statements like St. Louis Fed President James Bullard did on October 15th after the Dow was down more than 300 points shortly after the open. Bullard was interviewed by Bloomberg TV and said:

“If the market is right and it's portending something more

serious for the U.S. economy, then the committee would have an option of

ramping up QE [in December].”

Immediately after Bullard's October 15th comments, there

were unusually large orders to buy S&P 500 (IVV) and Russell 2000 (IWM)

ETFs, according to CNBC's Bob

Pisani…"There was a buzz on the floor at 9:45am (Eastern time) as the

rush of orders came, a buzz that is not often seen any more," Pisani

noted.

The market stabilized later that week with the Russell 2000 rising 1% or more each day. It rebounded strongly this past week with confidence rebounding without any fundamental economic catalysts.

NY Post Columnist John Crudele Adds Fuel to the Fire:

One well respected financial columnist is convinced the

Fed is intervening in the U.S. stock market.

Writing in the October 21st NY Post, John Crudele wrote:

"Maybe you’ll believe that there was some manipulation going on if you knew that a guy named Robert Heller, a member of the Federal Reserve’s Board of Governors until 1989, proposed just such a rigging as soon as he left the Fed...Heller wrote in an October 27, 1989 Wall Street Journal headline story: Have Fed Support Stock Market, Too:

“The Fed’s stock-market role ought not to be very ambitious. It should seek only to maintain the functioning of the markets -- not to prop the Dow Jones or the New York Stock Exchange averages at a particular level."

Curmudgeon Comment: Yet the last 10%+ correction ended very strangely in the last hour of trading on October 3, 2011 with no news to spark a very sharp rally in the market. We think the Fed or Plunge Protection Team intervened by buying stock index futures and/or index ETFs. There haven't been any official (i.e. 10% or more) corrections since then. That despite very weak U.S. and global economies with Europe flirting with recession, Japan still in a funk, and China's growth slowing precipitously. Oil, industrial metals and other commodities have been in a brutal bear market, indicating very weak demand for real things. So what's keeping the stock market up and seemingly invulnerable to a sustained decline?

Crudele continues:

"I've recently discovered that the CME Group, the futures exchange

in Chicago, has an incentive

program under which foreign central banks can buy S&P futures

and options contracts at a discount.

It’s not that these foreign banks need a break on the price of their

trading. But it does show that there is a back-door way — through foreign

emissaries — for the Fed and the US government to prop up stocks like Heller

suggested, and — maybe — not get caught."

Hedge Fund Honcho Comments on Difficulty of Short

Selling:

How does the Fed put effect the positions of long/short equity hedge funds? Commenting on the difficulty of short selling in what appears to be a rigged market, Third Point CEO Daniel S. Loeb wrote in an October 21st letter to its hedge fund limited partners:

"Amidst this volatility and performance dispersion, we struggle with our instinct that it is a good time to short stocks with the reality of the past few years of short-selling carnage. We were intrigued by investment legend Julian Robertson’s recent comments that, “we had a field day before anyone knew anything about shorting. It was almost a license to steal. Nowadays it’s a license to get hosed.”

"There is no doubt that the complexities around single name short selling have increased massively following 2008 – partly as a function of government regulation and intervention, partly due to negative rebates being the norm – but we have slowly been getting back in to the shallow end of the pool."

Victor on History of Fed Moving Markets & Technical

Analysis Revisited:

"ASK THE FED” is a very appropriate question. Since inception they have caused most of the events that have moved markets and the economy. Here's some background to prove this point:

"A prime architect of the Federal Reserve was German immigrant Paul Warburg. Arriving in America in 1902, he married into the family controlling Kuhn, Loeb and Company, which was America’s prime international banking firm. By 1907, he was earning $500,000 ($14,494,415 in today's dollars) annually. That was an enormously generous salary at a time when there was no income tax and inflation had not begun eroding the value of the dollar. When Paul Warburg left Kuhn, Loeb and Company to accept a post on the first Federal Reserve Board, he would earn only $12,000 yearly." (Source: The New American Magazine)

Warburg's willingness to take such a huge (98%) cut in salary is only one clue to the most important purpose of being on the Fed board. Paul M. Warburg was sworn in as a member of the first Federal Reserve Board on August 10, 1914. He was appointed vice chairman (called “vice governor” before 1935) on August 10, 1916. He resigned from the Board on August 9, 1918. From its inception, the acquisition of power, not wealth, was the goal of its creators, even though many opponents of the Fed down through the years have indicated the opposite.

Even though he was not a member of the Fed in 1929, Warburg's information was extremely telling as both London and the U.S. were raising interest rates. From the book How the City of London Created the Great Depression, by Webster G. Tarpley:

"The signal sent by the higher London Bank Rate was

underlined in March 1929 by the Anglophile banker Paul Warburg. This was once

again the scion of the notorious Anglo-Venetian Del Banco family who had been

the main architect of the Federal Reserve System. Warburg now warned that

the upward movement of stock prices was "quite unrelated to respective

increases in plant, property, or earning power." In Warburg's view, unless

the "colossal volume of loans" and the "orgy of unrestrained

speculation" could be checked, stocks would ultimately crash, causing

"a general depression involving the entire country." [Noyes,

p. 324] . . . .”

Why is the above tale relevant today? Warburg's spot on forecasting the cause of the great depression (7 months BEFORE the Oct 1929 stock market crash) is historical evidence that the FED is whom to ask...they control the show. Why do you think Warburg left his prestigious international banking firm for a job at the Fed with a salary of only 2% of his former pay?

In 1929 the Fed operated in complete secret. Today, the Fed uses "moral suasion" and the printing press to move markets as interest rates have been neutered for 5.8 years.

The gross manipulation of financial markets by the Fed, and the agenda of Central Planning the economy has made reading the markets impossible without knowing what the Fed Chairman and FOMC members are really doing. They seem to base their policies/agendas on politics and special interests, rather than the economy or the people. I say this as they haven't changed their policies in years or brought up (ineffective) fiscal policy as the real problem, so they just keep doing more of the same.

My strong belief, expressed in last week's Curmudgeon post (referenced above), was the Fed would not allow more than a 10% correction before the election. This was accomplished with words of St Louis Fed President James Bullard at a critical time in the recent market decline (as the Curmudgeon notes above, the S&P was down 9.8% intra-day from it's all time high on October 15th).

After the election, if the Republicans win control of the Senate, I feel they would be far more inclined to allow the markets to fall.

From a technical point of view, but far less dependable these days, the equity markets are classically topping. The market is rolling over in terms of the averages. That's analogous to an elderly man with a very high fever.

A very well-known book in the mid-1960's -- "The Stock Market Indicators" by William Gordon (Associate Editor Indicator Digest Inc.) --measured the 10 best stock market indicators back to late 1800's. The winner was a 200 TRADING day MA compounding at 18.5%. Dow Theory was second at 18.1%. Gordon tested many different versions, but the 200 day MA won with this simple rule:

"If the 200 day average line FLATTENS out following a previous rise, or is DECLINING, and the price of the stock (index) penetrates that line (MA) on the downside, this comprises a major selling signal." Vice versa for a major buy signal on the upside.

The virtual universal misunderstanding of this method is to sell when the index goes under the 200 day MA, while it is still rising, which is actually a buy signal. The misunderstanding comes from the plagiarism of these concepts, over time, and the fact is it got distorted.

We have tested this strategy using high performance computer simulations and it verifies Gordon's sell signal conclusion. A variation (due to the government's dislike for bear markets after 1981) basically adds to the performance by going flat stocks and into cash (30 day T-Bills) in lieu of short selling stocks or futures.

Bear markets used to be base building events. Now they are QE'd into a (bell ringing) buy signal as the FED prints fiat money.

Also the markets are now set up for many critical divergences. Most likely the S&P 500 and the breadth figures and/or small caps (e.g. Russell 2000 index) will not confirm each other at new highs. I don't think the Dow Jones Transports and Industrials will confirm new highs either.

The reality is that Fed money printing and their directly or indirectly buying stock index futures (or index ETFs) will always trump fundamental and technical analysis. The best approach is to think solvency and capital preservation over making the 8-10% (in capital gains) everyone talks about these days. The risk is very high today. Warren Buffett said: "Risk comes from not knowing what you're doing." Personally I always keep this in mind.

Till next

time......

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2014 by The Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).