Review, Comment and Analysis of a Volatile Week in the

Markets

By the Curmudgeon with Victor Sperandeo

Curmudgeon's Review & Comments:

After multiple triple digit up and down

moves during the last six trading days, stocks fell on high volume Friday, as

"investors" lightened holdings across the board. Declining Issues

outpaced advancing issues by 3.7 to 1 on the NYSE. The benchmark S&P 500 index lost 1.15% to

finish at a multi-month low of 1,906.13.

Meanwhile, the FTSE All-World share index

ended down 2% on Friday, while Eurozone shares fell to their lowest since late

2013. The FTSE 100 index of leading UK stocks fell 1.4% to 6,339.97, its lowest

close in a year. However, with the

exception of a few indices (e.g. Russell 2000), we're not even in correction

territory as the declines have been <10%.

The % declines of various stock indices

from their peaks are as follows:

·

DJIA: – 4.3%

·

S&P

500: –5.2%

·

NYSE

Composite: -7.0%

·

Nasdaq: -7.0%

·

DJ

Transportation Avg: -9.0%

·

Russell

2000: –12.8%

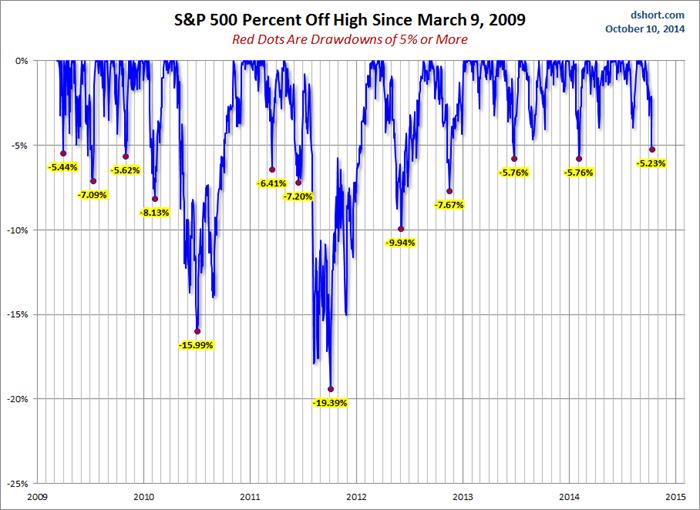

So far, the decline in the S&P 500 is

quite modest. The chart below, courtesy of Doug Short, incorporates a

percent-off-high calculation to illustrate S&P drawdowns greater than 5%

since the trough in 2009. There have

been four larger drawdowns since the last 10%+ correction ended in October

2011.

Chart Courtesy of Doug Short

But other sectors of the market (besides

the Russell 2000) are already in correction territory. An Oct 9th Bloomberg piece titled: Stealth

Bear Markets in U.S. Stocks Are Hiding in Bushes notes that:

·

SPDR

S&P Oil & Gas Exploration & Production ETF (XOP), a $1.1 billion fund, is down 24%

from its June record, setting a new 13-month low.

·

Microcap

technology shares have

lost ~ 22% from their March record.

·

Market

Vectors Gold Miners ETF

(GDX) is down 23% from its high this year and has plunged 67% from its record

in 2011. Note that GDX was down an

additional 2.12% on Friday.

As stocks and commodities have fallen,

bond prices have risen (yields dropped). The yield on the 10-year Note ended at

2.31% -- a 2014 low and the lowest yield since the 2.20% close on June 18,

2013. That could be a harbinger of a recession in

2015.

“There is a lot of nervousness. People

think economic growth will disappoint and central banks are not responding

quickly enough. Investors think Europe and emerging markets will drag down the

US,” said Mislav Matejka,

JPMorgan equity strategist.

That nervousness was apparent as $47B

flowed into money market funds last week -- the highest net weekly inflow for a

year, according to funds data provider EPFR.

In a further sign of unease, the VIX index of implied US share price

volatility – known as the Wall Street “fear gauge” – hit its highest level

since February.

In his Friday Comment of the Day to subscribers, David Fuller wrote about the greatest

risk for the market. It's what the

Curmudgeon and Victor have been pounding the table about for over one year:

"The biggest risk for Wall Street, in

my opinion, is not the corporate outlook and valuations; nor is it the bad

economic governance from the Obama administration, from high corporate taxes to

outsized fines for the banks, which deter lending; it is not even global

concerns from the war against 'Islamic State' to sanctions against Putin, or

the spread of Ebola, all of which drain capital. No, the biggest current

risk on Wall Street is leverage, also called margin debt."

"The amount of leverage that could

be unwound in a selloff would produce a significant correction, and even

cyclical bear markets of over 20% for some U.S. indices. This would also

drag many other stock markets lower, given Wall Street's influence. China would

probably be least affected because the mainland's bull market has barely

started."

Victor Analyzes Market Moves, Causes &

Effects:

In last week's Curmudgeon post, we

provided a case analysis surrounding the US Dollar (DXY is the symbol for the

U.S. $ Index). After a long rally, DXY

spiked up 1.12 cents on 10/3/14 (a huge one day move for the greenback index)

to close at a rally high last Friday. This set-up for an over-bought minor

correction of 1.43 cents Monday through Wednesday. The dollar rally then resumed, but up only +0.63,

and modestly down for week at -0.80%.

I believe that statements and comments

from the Fed and European Central Bank (ECB) leaders were largely responsible

for the big market moves last week, while raising questions about the effectiveness (or lack of

same) of their long term standing monetary policies.

The Federal

Reserve September meeting minutes, released 2pm EST on Wednesday

10/8/14 caused the S&P 500 to rally + 1.75% after being down Monday and

Tuesday for a total of -1.67%. So the

S&P was about even for the week after Wednesday.

Wednesday's big rally was likely caused by

a statement in the Fed minutes acknowledging the U.S. dollar strength, but

undermining the universal assumption that Fed Fund rates would begin to rise

from zero in the middle of next year (after 6.5 years). The Fed emphasized that any future rise in

short term rates would be "data dependent," rather than

pre-scheduled. Wall Street breathed a

sigh of relieve that rates might not rise till the second half of 2015. The Fed minutes also expressed concern over

the rise in the dollar slowing U.S. economic growth and lowering the inflation

target set by the Fed of 2%.

Are they acknowledging that being a

central planner is not easy? Or saving

the world and not harming U.S. economic growth is the meaning of having your

cake and eating it too?

Those minutes were somewhat confusing in

light of NY Fed President William Dudley statement on Monday

10/6/14. "If the economy evolves as

most people are hoping over the next year, hopefully we can get to a point

where we can raise interest rates in 2015 and I would be delighted

if that would be the case," he said.

Dudley has a permanent vote on Fed policy and is among the Fed's core of

decision-makers in the FOMC. His

message of "delight" carries the assumption of a strong economy (?),

which the Fed has predicted year after year ever since March 2009. Yet it still hasn't occurred!

The "data dependent" phrase in

the Fed minutes might also include economic data coming out of Europe. German industrial production was down

this week and exports dropped almost 6 % in August - the biggest drop since the

financial crisis several years ago. Last

week the IMF forecast a 38% probability of a recession

in the 18-country Euro-zone in the next year.

NBR Correspondent Bob Pisani

said: "The head of the European Central Bank,

Mario Draghi, again reiterated that there could be NO RECOVERY (emphasis

added) in Europe without structural and economic reforms. But a lot of

experts are increasingly doubtful that the European leadership will be able to

re-enact those reforms and get Europe back on the growth track."

Notice the change in the bottom line of

Draghi's remarks of "needed structural and economic reforms," rather than”

we got the EU covered."

A NY Times editorial on October 10th

parrots Draghi's remarks. In a piece

titled "A

Global Economic Malaise" the NY Times editorial board

states:

"Other European countries, like Italy

and Spain, need to do more to encourage companies to invest and create jobs, in

PART BY REFORMING LAWS THAT MAKE IT HARD FOR ENTREPRENEURS TO SET UP NEW

BUSINESSES." (emphasis added). Also saying “...Japan (officials) meanwhile,

have hurt that economy by raising a sales tax too fast."

Attention government officials: remember to boil the frog slowly by raising

taxes slower next time! Or “how"

you do what you do is critical not "what" you do.

I have repeatedly said that

"Socialism" is the issue holding back global economic

growth. [Please refer to The Trend Towards

World Socialism as THE Economic Problem of our Times!] It seems Draghi and the NY Times editorial board are talking in somewhat

opaque ways about that same problem.

Draghi saying there could be no European

economic recovery without reforms is quite different than his earlier promise

of "doing whatever it takes to save the Euro." Effectively, it means the ECB will NOT

be able to prevent a recession in the Euro-zone.

With a total of 28 countries in Europe,

which don't co-ordinate fiscal policies, do you really think reforms will

happen now? If it doesn't, one might

conclude all of Europe may go into recession (Italy is already there). If the EU reforms can't be accomplished,

economic growth can only be delivered by an effective devaluation of the Euro,

which would increase Euro-zone exports.

If the U.S. does not help this process, then the EU economies will

suffer, which will have negative impact on the U.S. That's because, more than ever, it’s a global

economy! However, if we allow the

dollar to rise, U.S. exports will be hurt and that will slow our economy. Message to U.S. policy makers: it's time to

pick your poison!

The realization that without enacting

effective reforms, Europe will likely drag the U.S. and rest of the world into

a global recession could've been the catalyst that caused the dollar to rally

Thursday and Friday, while the S&P and other stock indices resumed their

big sell-offs.

For a very long time, the Curmudgeon and I

have stated that stock market risk was and is

very high and that low volatility would not last. However, with the "Centrally

Planned" economy of the U.S., it seems logical that the Fed will

attempt to protect the stock market from a crash before the November

elections.

Therefore, there's a strong possibility of

a short term rally before a meaningful 10%+ correction occurs. If the September stock market highs are not

exceeded on the next serious rally (lasting weeks to months), then high risk

will become a reality, all things being the same as today.

Victor Evaluates the Risk of the Ebola

Virus in the U.S.:

On a separate but related note, which is a

moral rather than a pure political issue... The outbreak of the Ebola virus if

it spreads will cause havoc in the U.S., and the economy could crash.

A potential nightmare view of what could

happen if Ebola spreads is the movie "Outbreak," with Dustin

Hoffman. It is based on the Ebola virus,

although it's called "Motaba" in the

movie. It mutates (as all virus do in

some form) into an airborne version, and that is the end of times potential.

The reason this is a moral issue is the reason the U.S. is not banning travel

via flights or passport ID from the countries of Liberia, Sierra Leone, and

Guinea among others is because "we might offend those countries."

The ethical theory of

"altruism," from Emmanuel Kant, sacrifice for the greater good, or

compassion for strangers has been taken to a new low. The new mantra seems to be: sacrifice

yourself, your family, and loved ones for "political

correctness." Even Ayn Rand (author of Atlas Shrugged) did not

foresee this amazing low view of life.

The point is a pandemic which is here -

and if it mutates - will cause unimaginable disruption and death in the U.S.

and the world. Ebola is a level 4 category disease (the highest rated) or the

most deadly in the world today.

Breaking

News: The health care worker who contracted Ebola

in Dallas, TX was "wearing full protective gear." That means the worker wore “a gown, gloves,

mask and shield” while providing care, notes the Associated Press.

Victor's Conclusion:

The U.S. government's view of life,

combined with the ineffective way we're negotiating with Iran on nukes, dealing

with ISIS (with no ground forces we can rely on), and the failure to secure our

borders leads me to the conclusion that the powers that be are believers in nihilism.

Radical Professor Cornel West wrote

in the Cornel

West Reader:

“Nihilism is a natural consequence of a

culture (or civilization) ruled and regulated by categories that mask

manipulation, mastery and domination of peoples and nature.”

Let’s hope this conclusion is 100%

incorrect and that the powers that be will be more effective in dealing with

the world's problems.

Till next

time......

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2014 by The Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).