No Place to Hide as

Energy Prices Soar and War With Iran Escalates

By the Curmudgeon with Victor

Sperandeo

Market Week

in Review:

As the U.S.–Israel war with Iran entered its third week,

global investors found little relief across all asset classes. Traditional safe

havens such as U.S. Treasuries and Gold offered no protection.

·

The U.S. 10 year note yield

hit a new 2026 year to date high of 4.391% (price at a 2026 low).

·

Gold experienced its worst

weekly drop since March 1983, falling by nearly -9% to -11%. Spot gold prices declined for eight

consecutive trading days, the longest losing streak since October 2023.

·

On Friday, the SPDR Gold

Trust (GLD) was -3.1%, while the iShares Silver Trust (SLV) -6.33%.

·

U.S. equities notched a

fourth consecutive weekly decline - their longest losing streak since 2023.

·

Cash, particularly in U.S.

dollars, was the only effective haven amid a backdrop of firm central bank

resolve. The Federal Reserve and foreign central banks signaled limited

willingness to ease monetary policy, even as geopolitical risks escalated.

Here’s a chart showing how Bitcoin (BTC), TLT, SPX,

and Gold futures have performed in March.

Only BTC shows a slight gain with others in the red.

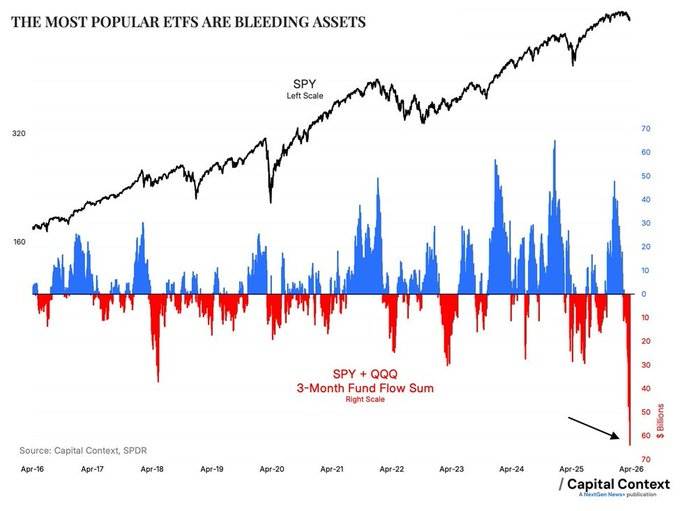

Global

Liquidity Declining; Stock Index ETFs Bleed Assets:

Michael Howell of Capital Wars states

"Latest readings reveal that liquidity had an absolute drop. This, despite

the U.S. Fed successfully injecting $170 billion through bill purchases using

the new RMP channel (Reserve Management Purchases) and the near-RMB2 trillion

(US $285 billion) pumped in by China’s People’s Bank ahead of the Lunar New

Year."

Overlooked by the financial press and mainstream media,

investors have recently been huge net sellers of U.S. stock market index

ETFs. The S&P 500 ETF (SPY) and the Nasdaq 100 ETF (QQQ) have seen combined

outflows of -$64 billion over the last three months, the most on record. Not

even the 2020 pandemic or the March-April 2025 sell-off saw such significant

outflows. It’s an extremely sharp reversal from +$50 billion in 3-month inflows

posted in November 2025.

Asset Class

Diversification Fails to Cushion Losses:

Stocks, bonds, gold, silver, and broad commodity indexes

(x-S&P GSCI which has ~60% to 70% energy weighting) were all down last

week. The agriculture commodity sector saw slight gains, with strength in

wheat, sugar, and cotton helping to balance weakness in soybeans.

àThere was really no place to hide other than being

100% in U.S. T-bills or short popular ETFs across asset classes.

The State Street

Bridgewater All Weather ETF (ALLW) is a great example of an

ultra-diversified, balanced portfolio that should lose less than the market

averages on declines, but didn’t.

The State Street®

Bridgewater® All Weather® ETF is an actively managed, diversified, global

multi-asset allocation ETF that seeks to be resilient across a wide range of

market conditions and environments, including economic contractions and

elevated inflation.

The SPDR Bridgewater All

Weather ETF (ALLW) invests based on a daily model portfolio provided by Bridgewater (founded by Ray Dalio),

ALLW’s investment sub-adviser, that is constructed based on the firm’s

proprietary All Weather asset allocation approach. The model portfolio provided

by Bridgewater allocates assets based on Bridgewater’s views of cause-effect relationships—specifically

how those asset classes react to shifts in growth and inflation. Based on

Bridgewater’s investment recommendations, SSGA Funds Management. Inc., ALLW’s

investment adviser, purchases and sells investments for ALLW. SSGA FM seeks to

implement Bridgewater's investment recommendations but may change ALLW’s

investment allocation at any time. ALLW may invest across a range of global

asset classes, such as domestic and international equities, nominal and

inflation-linked bonds, and commodity exposures.

On Friday, ALLW

closed at $28.04 or -3.11% that day. Its total return since the

Iran war started (March 2 - to - March 20, 2026) has been -7% vs the S&P

500’s total return of -5.37% during the same period.

….………………………………………………………………………………………………………

FOMC

Meeting, Federal Reserve Policy, and Foreign Central Banks:

The Federal Open Market Committee (FOMC) stood pat last week, holding the Fed Funds rate in their

3.50%–3.75% range as expected. Yet the decision, coupled with a steady outlook

for just one rate cut by year‑end, underscored how reluctant policymakers

remain to fight new fires with old tools.

Inflation risks due to the Iran war energy shock (“The

Straight of Disaster”) is very much a Fed focal point right now.

The U.S. central bank seemed to be acknowledging what

investors know all too well -- that the world has suddenly become a more

dangerous place—for policymakers, traders, and anyone trying to protect wealth

in real terms.

Federal Reserve Chair Jerome Powell stated that he will

remain as chair pro tempore after his term expires on May 15, 2026, until the

Senate confirms his successor. Powell also declared he will not resign from the

Fed Board of Governors until a Department of Justice investigation is

finalized, allowing him to stay on the board until 2028.

Sharply increasing oil and gas prices (WTI crude oil +48% in March) have reinforced

inflationary pressures, prompting markets to reassess the likelihood of

near-term rate cuts. By Friday, Fed

Funds futures that previously had anticipated two quarter-point (25 bps)

reductions before hostilities began on February 28th were instead

pricing roughly a one‑in‑three chance of a small rate hike by

year‑end. The two‑year Treasury yield—most sensitive to policy

expectations—rose 50 basis points to 3.89%, while the 10‑year yield

reached a new 2026 high of 4.39%.

Around the globe, that tone of central bank restraint is

spreading. The ECB, the Bank of England, and the Bank of Canada have all chosen

to hold steady, while Australia’s central bank tightened again to curb

inflation.

Recession

Risk of Rising Energy Prices:

The trigger for this new global central bank conservatism

(certainly not dovish but not yet hawkish) is the spike in crude oil

prices—Brent briefly hit $119 a barrel this week, reigniting the fear that

energy costs could undermine the fragile progress against inflation.

Yet there’s another, darker precedent: almost every major oil

shock since the 1970s has eventually tipped economies toward recession. We clearly depicted that risk in a chart

within last week’s Sperandeo/Curmudgeon blog post.

For investors, that’s the trap. Rising energy prices can fuel

inflation expectations, forcing central banks to stay hawkish—until growth

cracks and markets slip into something worse than turbulence.

Bank of America economist Aditya

Bhave notes that the Fed would only consider hiking again if the labor

market stays tight, input costs rise across supply chains, and longer-term

inflation expectations begin to drift higher. He pegs the danger zone at WTI

crude sustained between $80 and $100 per barrel. On Friday, WTI closed at

$98.32—uncomfortably close to that threshold, and up nearly 47% since the start

of the conflict.

Deutsche Bank economists warn that if crude holds above $100, the economy

could enter what they term a “nonlinear” phase—where inflation accelerates

while employment weakens, a toxic mix for both stocks and bonds. Markets, for

now, are betting the Fed can manage the balance: Treasury yields have surged,

with the 10‑year at 4.39% and the long bond approaching 5%, both

eight‑month highs. But for investors focused on wealth preservation

rather than short-term opportunity, the signal is clear: liquidity, quality,

and patience may once again outperform bravado.

Victor’s

Comments:

The global economy faces a

critical, systemic inflection point following President Trump’s 48-hour

ultimatum on Saturday for Iran to reopen the Strait of Hormuz (see map below), threatening to

"obliterate" Iranian energy infrastructure, including power plants.

With 20% of global oil and liquefied natural gas (LNG) passing through this

chokepoint, any further disruption could trigger an unprecedented global energy

shock.

My strong belief is Iran will not

obey any Trump threats, noting he often does not follow through on them (e.g.

the TACO mentality).

Summary of

Economic and Market Risks:

-Energy Supply Shock: A prolonged closure of the strait

or destruction of energy infrastructure (Iran/Qatar) could drive crude prices

to $200-$250/bbl, as supply constraints reach critical, irreparable levels.

-Systemic Financial

Risk: Retaliation by Iran,

including mining the Gulf or striking Qatari gas facilities, could cause a

collapse in regional infrastructure, creating a "doomsday" scenario

for energy supply that would take years to repair.

-Geopolitical Spillover:

China, as a major importer

of Iranian oil, may be forced to enter the conflict to secure its supply chain,

potentially elevating the crisis and endangering Taiwan's sovereignty and

regional tech manufacturing capacity.

-Manufacturing Supply

Chain Threat:

The disruption of helium shipments—crucial for semiconductor

manufacturing—through the Strait of Hormuz directly threatens the global

technology sector.

Victor’s

Market Positions:

I am still long 5-year Treasury

notes, gold and silver as long-term investments. Expect more volatility in all markets until

the conflict in the Middle East subsides.

Outlook for

the Week Ahead:

The coming week will test whether markets can sustain their

composure amid rising yields and ongoing geopolitical tensions. Several Federal

Reserve officials are slated to speak, and investors will parse every remark

for signs that the hawkish tone is hardening in response to the oil shock. The

Treasury will hold mid‑week auctions of two‑, five‑, and

seven‑year notes—each likely to gauge investor appetite for duration at

near‑cycle‑high yields.

Energy markets remain the wild card. Any further disruption

in Iranian or Gulf exports could push Brent firmly above $120, complicating

inflation math for policymakers and rekindling volatility across asset classes.

Equity traders will also be watching corporate guidance from

energy‑intensive manufacturers and transport firms for early signs of

margin strain.

Barring geopolitical escalation, the focus shifts to macro

data late in the week—personal income, spending, and the Fed’s preferred PCE

inflation gauge—all potential catalysts for repricing expectations on the

timing of the next policy move. For now, stability is a relative term, and

market discipline, not optimism, remains the safer trade.

….……………………………………………………………………………………………………………..

End Quote:

A Thought to Remember:

“The darkest places in hell are reserved for those who

maintain their neutrality in times of moral crisis.”

Dante Alighieri was an

Italian poet, writer, and philosopher.

His Divine Comedy, originally called Comedìa

and later christened Divina by Giovanni Boccaccio, is widely considered one of

the most important poems of the Middle Ages and the greatest literary work in

the Italian language.

….……………………………………………………………………………………………………………………………………………………………………………………………

Wishing you good health, success, and good luck. Till next

time.

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever-changing and arcane world of markets, economies, and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2026 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).