Geopolitical Risk and European Elections May Undermine

Fed

By Victor Sperandeo with the Curmudgeon

Introduction:

The Fed and the Markets:

After 134 years

of the real economy being the major driver of stock prices, the past few years

have shown that is no longer the case.

Since at least 2010, the U.S. stock market has not been correlated to

economic fundamentals. What has changed is the Fed's money printing (QE) and

zero short term interest rates (ZIRP).

To a lesser extent, the same is true for Europe and Japan with their

ultra-easy monetary policies with assertions of more of the same (see ECB head

Draghi's comments below).

Many now

believe that owning stocks when the Fed wants you to own them removes the risk

of a bear market or even sharply falling stock prices. Exploding margin debt is one symptom of that

thesis. Risk takers believe the Fed

(and the ECB) will prop up the market "no matter what it takes." Hence, they're using lots of leverage to

magnify potential gains on their long stock positions. The bond market has also benefitted from

ZIRP, QE and "operation twist."

It seems Mayer Amschel Rothschild was right when he said, “Give me control

of the nation’s money and credit and I care not who makes the laws." Apparently, nothing else matters to the

market at this point in time. Indeed, a

counterfeiter (the Fed) can turn a weak economy into a booming stock

market. But what could possibly go

wrong?

Geopolitical

Hotspots Pose Uncontrolled Risk:

We think the

potential risks in the market are geopolitical hotspots that can boil over into

something that could have very negative fallout for the global economy and

financial markets. Historically, markets

don't discount war until it is happening.

World War I and II are two great examples of that thesis.

An erupting

geopolitical hot spot can cause a significant decrease in global trade, which

might even precipitate a trade war. That would be horrendous for the world

economy. The Fed (or foreign central

banks) won't be able to stop or control such geopolitical eruptions--even if

they print more money.

Specifically,

we think that energy /oil prices could dramatically increase as a result

of hostilities in Ukraine. Russia could

decrease or stop exports of liquid natural gas to Europe. They could control oil prices too, despite

Saudi Arabia acting as the swing OPEC producer and the U.S.

producing more oil.

[Note: Russia’s

net crude oil export revenues amounted to approximately $290 billion in

2012 and therefore were more than four times as high as net natural gas exports

in the same year. Energy Information

Agency (EIA) data show that in 2012, Russia exported approximately 7.4 million

barrels per day of total liquid fuels.

The majority (79%) of Russia’s crude oil exports were to European

countries (including Eastern Europe).]

There are

numerous other geopolitical risks we'll examine later in this article. While the probability of any one causing

economic damage and financial fallout is low, it's quite high when all the

hotspots are taken into account.

The Russian

Federation:

Russia is the

highest risk to the global economy and the markets. Moving into Ukraine might be just the first

stop on their agenda of reconstructing a "greater Russia." As a leading oil and gas supplier, Russia

might be able to raise energy costs either directly (by raising prices) or

indirectly (curtailing supplies by cutting off energy supplies to Western

Europe).

Let me

state emphatically that no one can stop Russia -no matter what it wants to

do. Their military strength is superior to any

country.

·

Russia's

nuclear arsenal totals 8,500 total nuclear warheads, of which 1,800 were

strategically operational. The nuclear

weapons of all other countries combined together totals 8,800. The U.S. nuclear

warhead count is 7,700. (Source: "World Nuclear Stockpile Report,"

January 7, 2014)

·

Russia

has a total military force of 3,250,000 (766,000 active military, 2,035,000

reserves, and 449,000 para-military). In

contrast, Germany has a total military of 326,927 with only 182,927 on active

duty.

·

Perhaps

Vladimir Lenin's quote explains how easy Russia can march into most places in

the world. "One man with a gun can control 100 without one." There are only a few nations that allow gun

ownership and few of these nations have anything you would call an army.

Who can stop

Russia? Aside from China, which Russia would not invade because they are

ideological "comrades." If Russia puts boots on the ground in Ukraine

and (later) other countries in Eastern Europe would President Obama be able to

stop him? No chance! I'm not saying Russia intends on doing this -

my point is Putin could do so with little risk of U.S. troops interfering.

Also, Putin

might force Europe to buy oil in Rubles, which would severely damage the U.S.

dollar. That tactic could spread and cause

other countries to trade in their currencies.

We've previously hinted that China wants to make the Yuan

the world’s reserve currency. That

could be the death knell for the dollar, which would've likely crashed a long

time ago if it were not the world's reserve currency and currency used to

buy/sell OPEC oil.

Economic

Sanctions are Ineffective:

In a joint

statement on May 10th, Germany's Chancellor Merkel and France's President

Hollande warned Russia that it would face tough sanctions if it did not

help defuse the crisis in Ukraine, including taking “visible steps” to pull

back its troops from Ukraine’s border. Last week, President Vladimir Putin said

he had already done so, but NATO and Western leaders said they had seen no

evidence of a withdrawal.

Sanctions

are laughable as a deterrent, in my humble opinion. They've

done nothing to stop Russia's aggressive involvement in Ukraine or their

support for the Assad regime in Syria.

Do you think sanctions on Cuba have worked? The Cuba embargo/sanctions are 52 years old,

but the Castro brothers are still in total control of that island nation. They couldn't care less about changing their

totalitarian version of communism to benefit the people who live there.

We think sanctions

may even be counter-productive. As payback for European sanctions, Russia

could cut off natural gas shipments to Europe.

That would be a disaster in winter time, because natural gas is used for

heating homes and commercial buildings.

Shortages of gas and higher energy prices might even cause the Euro to

breakup, as leaders are voted out of office and more nationalist politicians

take their place. See Elections in

Europe - May 22-25, 2014 below for more on this important topic.

In the end, we

think sanctions don't have much impact, other than to anger the target country

into responding in a way that might hurt the global economy.

Iran and

Israel:

Iran's uranium

enrichment program is thought to be part of a master plan to develop nuclear

weapons. Iran and the five permanent

members of the UN Security Council – the United States, France, Britain,

Russia, China – plus Germany have been holding talks aimed at reaching a

comprehensive deal on the Islamic Republic’s nuclear energy program. The two

sides sealed an interim deal in the Swiss city of Geneva on November 24, 2013,

which went into force on January 20th.

Under the Geneva agreement, the six countries undertook to provide Iran

with some sanctions relief in exchange for the Islamic Republic agreeing to

limit certain aspects of its nuclear activities during a six-month period. But the monitoring of Iran's nuclear reactors

has been very difficult, so compliance is in doubt.

Israel's

Netanyahu has repeatedly stated that Iran must not be permitted to possess a

nuclear bomb. Many foreign affairs

experts have speculated that Israel would launch a pre-emptive strike on Iran's

nuclear reactors to prevent them from obtaining nuclear weapons. This has been

on the front burner for a long time now and many people feel it won't

happen. But what if it does?

It's my opinion

that Israel cannot allow Iran to develop nuclear weapons that can kill 20 - 30%

of its population in one fell swoop.

Then there'd be radioactive fallout that would kill even more

people. Israel--the homeland for the

Jews--is a very small country. 7.7 million people live

on 8,019 square miles of territory. Could the Jewish state survive such a

catastrophe? I don't think so.

Therefore, I

believe that at some point in time Israel will be forced to attack Iran's

nuclear facilities, which could lead to oil prices spiking to $150 to $200 a

barrel. Such an "oil shock"

would likely crater world stock markets.

Like Russia's invasion of Ukraine, it would be another unanticipated

event that neither the Fed nor foreign central banks would be able to control.

Other

Geopolitical Hotspots That Might Erupt:

A few other

geopolitical problems worth mentioning are the following:

·

China

vs Japan over a territorial dispute

in the five uninhabited Islands. The

Japanese call them the Senkaku Islands. The Chinese

call them the Diaoyu Islands. Japan controls the

islands, but China wants them. While international law favors Japan, many say

that China will attempt to take them over.

Since the early 1970's, China has argued that Japan seized the islands

in violation of international law.

Whether Japan should resist or retreat is a military and political

question, not a legal one. No one knows

if China’s ambitions extend only to these tiny unoccupied islands in the South

China Sea or if this is the first step in a larger march of conquest of

territories in Asia. Don't forget that

China and Japan are the world's number two and three economies, respectively.

Japan becomes a significant problem if they can’t peacefully settle their

disputes with China. Japan's stated debt

to GDP ratio is 227.2% - the highest in the world. Any increase in Japan's budget deficit (e.g.

for military spending), at this high risk level, could cause a meltdown of

Japan's economy.

·

China

vs Vietnam over oil

drilling rigs 200 miles off Vietnam. Chinese

ships have been ramming into and firing water cannons at Vietnamese vessels

trying to stop Beijing from putting an oil rig in the South China Sea. This is a dangerous escalation of tensions

over waters considered a global flashpoint.

·

Civil

War in Venezuela--a full

blown Statist government, Venezuela's economy is in shambles. There are food scarcities and now water

rationing. The government has started

to issue cards to track families' purchases of food. Critics say it's another sign the oil-rich

Venezuelan economy is headed toward Cuba-style dysfunction. If its economy deteriorates further, that

could instigate a people's revolt or even civil war. There have already been a series of

protests, political demonstrations, and civil unrest throughout Venezuela. Those protests could worsen into a full blown

civil war.

Venezuela produces an estimated 2.9 million barrels of oil a day (as of

February, 2014). Any civil war or

internal fighting (like in Syria) could cause Brent crude oil to move towards

$130 per barrel. That would certainly be a significant risk to the

global economy.

·

North

Korea Threats--nuclear

armed North Korea has long been seen as a threat to both South Korea and

Japan. These tensions cannot be

overlooked as their leader -Kim Jong-Un - is an unpredictable, calculating

ruler. Some say that Mr. Kim, who has

proved to be more ruthless, aggressive and tactically skilled than anyone

expected, most likely has a psychological disorder?

Elections in

Europe - May 22-25, 2014:

Ukip of the United Kingdom and the National

Front of France are gaining more momentum leading up to elections later

this month. That could spell trouble for

European economies and the Euro.

Ukip has been accused of hypocrisy and double

standards for paying

Eastern Europeans to distribute their election leaflets, despite the

party's leaflets warning that immigrants from the EU pose a threat to British

jobs.

The National

Front (or FN) is an

economically protectionist, socially conservative nationalist political party

in France. The party was founded in 1972, seeking to unify a variety of French

nationalist movements of the time. It

has been the unrivalled major force of French right-wing nationalism force of

French right-wing nationalism since 1984.

If the NF party wins or gets a significant vote in the French elections,

it may be the end of the Euro. (At least

that would be a bloodless resolution.) It's looking more and more to me that

the Euro is going to lose its place as the single currency of the Euro-zone.

France's

President François Hollande says he won't run for re-election if unemployment

remains high (it was 19% as of April 2014).

Hollande visited the Michelin plant on Friday where he made a shocking

announcement during a lunch with employees:

If unemployment continues to plummet between now and 2017, Hollande said

he will have “no reason to be a candidate” for a second term. Meanwhile, the French president's approval

rating -now at 18% - has hit a new record low (as of March 2014).

State of the

Markets and Monetary Policy:

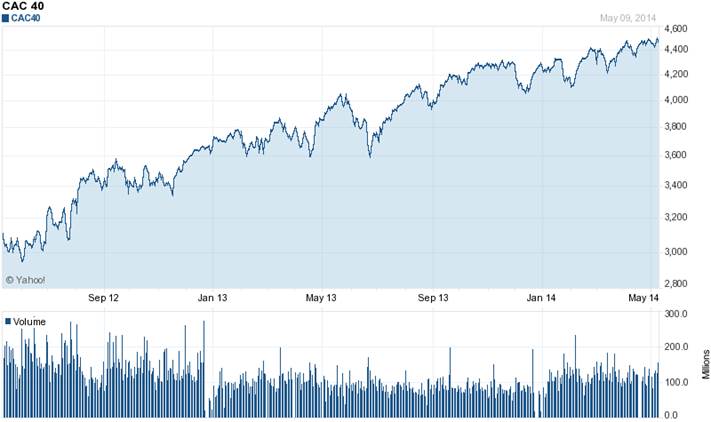

Yet despite a

very weak economy, sky high unemployment, and President Hollande's horrible

approval rating, the French stock market (as measured by the CAC 40) has been

in a steep uptrend for the last two years.

The steep up move is quite evident in the chart below:

That strange

market reaction is hardly an exception. The

stock markets in Japan, Europe, the U.K. and U.S. are up strongly and are at or

near all-time/recovery highs for only one reason: Central Banks easy monetary

policy--holding short term interest rates at virtually zero for five full

years, coupled with the Fed's QE buttressed by ECB head Draghi saying he'll do

"whatever it takes...." And he

may actually follow through with that next month!

In a statement

earlier this week, Draghi hinted the Eurozone economies could see the emergence

of negative interest rates as early as this June. He told reporters that the ECB has room

available to use various monetary policy tools available to them and that the

24-member ECB Governing Council is “comfortable with acting next time.” He said policy makers discussed all tools

available, including extending the offer of unlimited central-bank cash against

collateral. Other possibilities include long-term loans to banks and halting

the sterilization of liquidity created by crisis-era bond purchases.

We think

anticipation of such ECB easy money action is preventing European stock markets

from falling, which would otherwise be expected considering the weak economies

in the region (with the possible exception of Germany).

As bizarre as

it seems, the evidence suggests that weak economies and high unemployment is

actually bullish for equity markets. Why? It makes the Fed and/or other central banks

print more money which then flows into financial markets. Stock market correlation with QE has

certainly been true for the U.S. and Japan. Draghi hints that the Euro-zone is

next to experience QE and possibly negative interest rates.

In reality,

that's a monetary policy only a counterfeiter would love. Credit is created by central bank money printing to buy debt issued and/or

already sold by the Treasuries of the countries using QE. As the CURMUDGEON has repeatedly pointed out,

the Fed's QE is a Ponzi

scheme of the highest order. QE does

nothing to promote the welfare of ordinary citizens that don't own stocks.

Meanwhile,

corporations are hoarding cash rather than investing in new plant, equipment or

hires. Wages are contained due to

economic uncertainty and lack of collective bargaining power of employees. Workers are afraid of losing their jobs so

they are more cautious with their purchases.

The velocity of money has been dropping precipitously, so there's been

no inflation to speak of at this time.

Therefore, some say the Fed/ Central Banks should do more QE? Its insanity, but it keeps going on....

Conclusions:

Under normal

conditions the Fed has some ammunition to act as a safety net to prevent or at

least contain an economic/financial crisis.

Having already pinned interest rates to zero for five+ years and

augmenting that with massive amounts of QE (which has not worked to stimulate

the real economy), the Fed has no magic bullets left.

This will be an

issue that is dependent on the type of crisis that boils over. For example, if oil increases to $150 per

barrel how could the Fed justify additional QE, which logically would drive oil

prices higher and weaken the U.S. dollar?

Institutional

money managers and pension funds "invest" money on behalf of

others. They don't seem to appreciate

the risks in the market as they are not paid to worry about geopolitics or

other threats. Yet they can't afford to

be left behind, holding cash or short positions in a rising market that's

independent of economic fundamentals.

The end game of

bull markets with weak economies will not be pretty. It's highly likely that one or more

geopolitical events or unfavorable elections will end the party for the bulls. We think that the catalyst for a steep stock

market decline will be some type of geopolitical risk or other unanticipated

event that neither the Fed nor foreign central banks will be able to control. The markets will be caught by surprise, but

don't say we didn't warn you!

Till next

time........................

The Curmudgeon

ajwdct@sbumail.com

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2014 by The Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

url of the original posted

article(s).