Low Consumer

Sentiment and Price Pressures Put Fed Rate Cuts on Hold

By the Curmudgeon with Victor

Sperandeo

U.S. Consumer Sentiment at All-Time Low:

Consumer sentiment from the University

of Michigan fell sharply in its preliminary April reading dropping from

53.3 to 47.6. The Overall Index and

Current Conditions Index fell to the lowest levels on record, while the Future

Expectations Index has only been lower in late

1979 and early 1980, just before the double dip recession.

In addition to record low sentiment, this report also showed

inflation expectations for the year ahead, increasing to 4.8% from 3.8%. While

much of this month’s move is likely due to the Iran conflict, Consumer

Sentiment was near historic lows prior to the start of the war, and it will

take time for consumers to feel confident in their personal finances again –

especially as they grapple with rising prices.

Respondents reported the weakest perception of their

personal financial situation since 1951—surpassing the pessimism seen

during the Great Financial Crisis and other historic shocks, including the

Vietnam War, Black Monday, and the double-digit inflation era of the early

1980s.

Joanne Hsu, University

of Michigan Survey of Consumers Director wrote:

"Demographic groups across age, income, and political

party all posted setbacks in sentiment, as did every component of the index,

reflecting the widespread nature of this month’s fall."

Importantly, the April data were collected before the

announcement of a temporary ceasefire in the Iran war. Sentiment may improve if

geopolitical tensions ease, but confidence had already deteriorated prior to

the conflict, signaling broader structural concerns. Households continue to

cite persistent inflationary pressures and declining asset values as key

headwinds—factors that could restrain consumption.

Since consumer spending represents roughly 70% of U.S. GDP,

sustained weakness in sentiment poses downside risks to near-term economic growth

and equity market performance.

Hot Inflation Readings:

To add to U.S. consumer miseries, inflation is increasing and

likely to get worse.

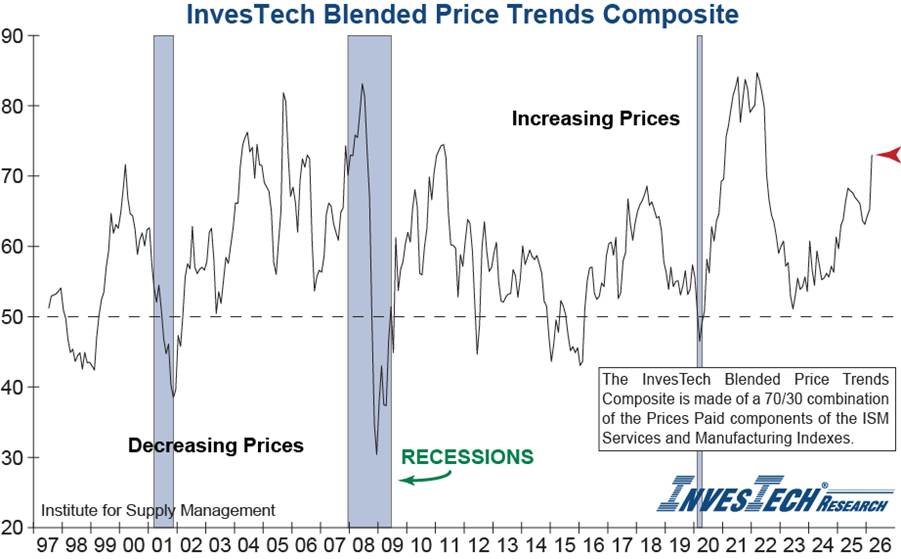

Two Institute for Supply Management (ISM) surveys, released in the first week of April,

showed that both manufacturing and services sectors have experienced accelerating

price pressures. Executives noted steep cost increases that could

foreshadow an increase in inflation, which is already above the Federal

Reserve’s 2% target. Should inflationary trends intensify, the Fed will likely

focus more on price stability, limiting the prospects for rate cuts in the

coming months (more below).

Meanwhile, the March CPI rose 0.9% monthly, hitting

3.3% annually due to surging energy costs. The February PCE, the Fed’s

preferred inflation gauge, rose 0.4% (2.8% annually), with "core"

PCE (excluding food/energy) up 3.0% annually, indicating continued

inflationary pressure.

To make matters worse, elevated energy prices stemming

from the Iran conflict and the effective closure of the Strait of Hormuz introduce

additional inflationary risk.

Cartoon Courtesy of Hedgeye

This combination of geopolitical volatility and resurgent

cost pressures could prompt the Fed to consider rate hikes later this

summer or fall, challenging market expectations for easing and potentially

tightening financial conditions across the yield curve.

From a financial market perspective, weak consumer sentiment often

results in softer consumption and lower economic growth. The

high and “sticky” inflation numbers indicate a pressured consumer that may

cause sentiment and spending to deteriorate further.

Such a “stagflation” scenario increases the odds that the Federal

Reserve will focus more on its price-stability mandate, which would delay rate

cuts and keep yields “higher for longer” than most expect.

The CME

Fed Watch Tool shows the majority of 30 day Fed Futures traders expect the

target Fed Funds rate to remain at 350-375 bps through the July 28, 2027 FOMC

meeting! A sizable number of traders

expect a RATE INCREASE before then.

Victor’s Comments:

Consumer sentiment is like a stock’s P/E ratio, because it

reflects the true psychology of the people.

Very low sentiment depicts a negative view of what the public thinks of

current economic conditions, without interference from White House hype or news

media propaganda machines.

Fearful consumer views of the future are well founded in light of the UNEXPECTED U.S. WAR WITH IRAN AND ITS

EFFECTS ON OIL PRICES.

Also, the Fed is not likely to backstop the negative

consequences of a deteriorating U.S. economy due to the feud with President

Trump, who has repeatedly threatened the Fed’s independence by urging them to

lower rates.

There are many more U.S. economic problems that are being

“swept under the rug:”

l Private Credit issues are much more negative than reported

due to a lack of transparency and huge losses.

l The labor market is showing clear signs of deterioration with

a declining labor force participation rate.

l Weakness of the U.S. bond and fixed income markets which are

the foundation of the U.S. economic and fiat currency system.

l Gold markets are foreshadowing a “deflationary, recessionary

story.”

-->Mark my words:

the U.S. is already in recession.

Victor’s Market Positioning and Conclusions:

What’s holding up the U.S. equity markets are strong earnings

forecasts which are not being lowered. They will be shortly in my view!

I am still long 5-year notes and gold +silver as an investor,

I also have a small number of U.S. equity market puts.

President Trump’s on again, off again war with Iran is

whipping markets around to such a degree that all but day traders are going to

be forced to the sidelines. It’s best to

NOT trade during Trump’s whimsical and narcissistic mental conditions.

Good luck to America…………………………

End Quote:

"People are supposed to fear the unknown, but ignorance

is bliss when knowledge is so damn frightening.” - Laurell K. Hamilton

Laurell K. Hamilton is the author of two major book series,

spin-off comic books, various anthologies, and other stand-alone titles.

….………………………………………………………………………………………

Wishing you good health, success, and good luck. Till next

time……………

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever-changing and arcane world of markets, economies, and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2026 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).