2024

AI Fueled Stock Market Bubble vs 1999 Internet Mania?

By the Curmudgeon

It’s the AI way or the

Highway:

The run in Artificial

Intelligence (AI) stocks this year has many analysts making comparisons to

the 1999 “Dot.com” bubble. AI poster child

Nvidia’s (NVDA) market cap is about

$2.2 trillion. Nvidia currently enjoys 75% gross profit margins and has an

estimated 80% share of the Graphic Processing Unit (GPU) market.

Voracious demand has outpaced production

and spurred competitors to develop rival chips. The ability to secure GPUs

governs how quickly companies can develop new artificial-intelligence systems.

Tech CEOs are under pressure to invest in AI, or risk investors thinking their

company is falling behind the competition.

Tech stocks are punished if they can’t produce any AI infused products

that are in demand.

That’s

exactly what happened to Apple (AAPL) in the last few weeks. Despite a

+1.02% pop on Friday, AAPL has declined almost 12% this year, erasing over $300

billion in market capitalization. Questions linger over Apple’s AI initiatives,

while Microsoft and other tech behemoths deliver tangible earnings growth tied

to AI technology.

The markets

concern about Apple’s lack of successful AI products was underscored by

Tuesday’s report that the company is abandoning its decade-long electric car

project – an undertaking Apple CEO Tim Cook had called the “mother of all AI

projects” in 2017. Investors have sold

AAPL in droves in the last month due to a lack of credible AI initiatives from

the company such that AAPL has way underperformed the tech heavy NASDAQ 100

(QQQ ETF).

Nvidia (2024)

vs Cisco (1999):

History tells

us that the valuations investors currently pay for companies like Nvidia

(35x Price-to-Sales) are unsustainable.

In 1999,

Cisco Systems (CSCO) was the “belle of the ball,” with investors believing the

“internet would change the world.” The thinking at that time was that the whole

internet would run on Cisco routers at

50% gross margins. Just as in 1999, extrapolated valuations rarely play out

in reality.

As shown in

the chart from TheMarketEar

below, Cisco’s valuation at its peak of the “Dot.com” mania was at 33x sales.

CSCO investors lost 85% of their money when the stock price troughed in

October 2002. Over the next 16 years, as investors waited to break even, the

company grew revenues by 172% and earnings per share by a staggering 681%. Over

the last 22 years, CSCO buy and hold investors earned only 0.67% per year!

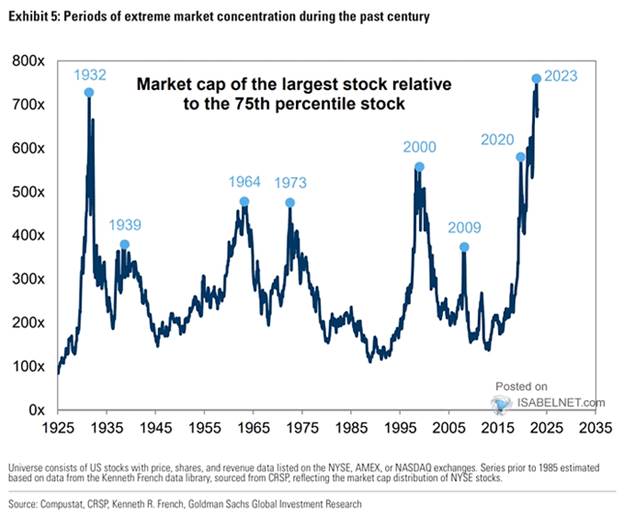

Market Concentration is a Concern:

"Despite

the strong returns, many clients have expressed anxiety about the extreme

current degree of market concentration relative to recent history,"

says a team of equity strategists at Goldman Sachs led by Ben Snider.

The 10

largest stocks now account for 33% of the S&P 500 market cap, well

above the 27% share reached at the peak of the tech bubble in 2000, and 25% of

earnings, according to Goldman. The

chart below shows that stock market concentration is at an all-time high.

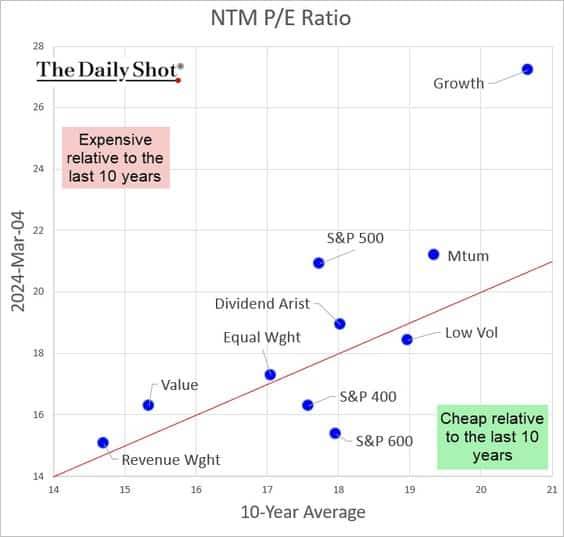

Market

Valuation of Growth Stocks:

The

valuations of the market's growth sector are trading at astronomical

levels relative to its 10-year average while low volatility defensive stocks

are cheap. That’s shown in the chart

below, courtesy off the Daily Shot:

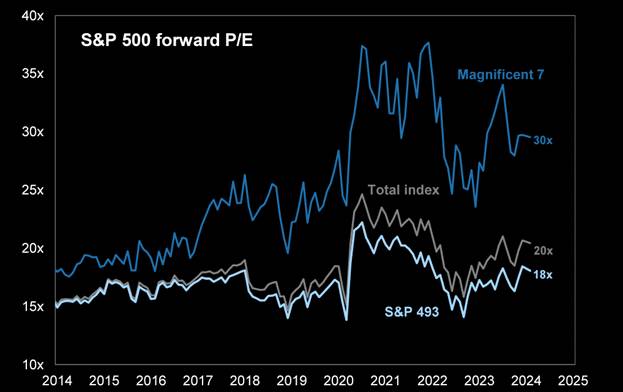

Finally,

consider the forward P/E of the “Magnificent 7” (even with

the decline of AAPL) versus the rest of the S&P 500 as per this chart:

Chart

Courtesy of Real Investment Advice

…………………………………………………………………………………………………………

Conclusions:

Despite ultra-high

valuations, we advise AGAINST shorting the market or selling large

amounts of stock/ETFs/equity mutual funds you now own. John Maynard Keynes once said, “Markets

can remain irrational longer than you can remain solvent.”

There may be

more upside ahead as the stock market advance has recently broadened. According to Bloomberg Intelligence, the

share of S&P 500 stocks at all-time highs in the past month has risen,

reaching the highest since early 2022. Yet less than a third of stocks are at

record highs. In contrast, by the time the tech bubble was about to burst in

early 2000, the ratio of stocks at historic highs was decreasing, from around

60% at one point in 1997 to 20% in 2000.

Nonetheless,

the Curmudgeon believes the U.S. stock market is in an AI and liquidity fueled

bubble. History shows that once a bubble inflates, it will remain inflated

until some unexpected, exogenous event causes a reversal in the underlying

psychology. That reversal then reverses psychology from “exuberance” to

“fear.” No one knows what will cause

that reversion in psychology.

By the peak

of a bubble, it’s common for investors to capitulate to the idea that market

valuations/prices “have reached a permanently high plateau,” as Yale economist

Irving Fisher proclaimed on October 16, 1929 (just days before the multi-decade

October 24th stock market crash).

Then when a sharp drop/severe stock market correction occurs, the

mainstream media will say, “No one saw this coming.” Really?

End Quote:

“When

positive feedback develops between the trend and the misconception, a boom-bust

process gets set into motion. The process is liable to be tested by negative

feedback along the way, and if it is strong enough to survive these tests, both

the trend and the misconception get reinforced. Eventually, market expectations

become so far removed from reality that people get forced to recognize that a

misconception is involved. A twilight period ensues during which doubts grow,

and more people lose faith, but the prevailing trend gets sustained by

inertia.” – George Soros

Be well, success, good luck and till next time………………

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever changing and arcane world of markets, economies, and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2024 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).