Will the

Fed Keep Interest Rates Higher for Longer?

By the

Curmudgeon with Victor Sperandeo

Introduction:

The 10-year U.S. T-note interest rate closed Friday at 4.33%,

which it also hit on Aug 21, 2023. That is the highest level since 2007 when

the U.S. 10-year rate averaged 4.63%.

The 2-Year U.S. T-note yield rose seven basis points to close

the week at 5.04%. That’s the highest

yield since July 2006 when it was a smidgen higher at 5.122%. It’s hard to believe that the 2-year yield was

a measly 0.123% at year-end 2020.

Bets that intermediate U.S. interest rates would decline due

to a serious recession, or at least a slowing economy, have failed. U.S. bond investors (like the Curmudgeon)

have lost money for the second consecutive year.

However, the longer interest rates stay elevated the greater

the risk of an economic downturn and lower rates down the road. There are now more signs of consumer stress

as higher borrowing costs and weaker hiring start to erode household

spending.

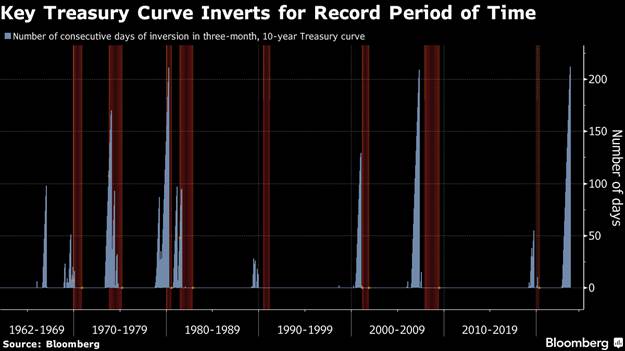

Record Duration for Inverted Yield Curve:

The inverted yield curve (shorter term rates higher than

longer term rates) continues to forecast that the U.S. economy is veering

toward a contraction. For 214 straight

trading days, 10-year yields have held below 3-month yields. Such an inversion telegraphed the last eight

recessions. On Thursday, the U.S. Treasury market surpassed the 1980 record to

hold that way for the longest consecutive daily stretch since Bloomberg’s

records begin in 1962.

“This cycle has been an odd one, because when the yield curve

originally inverted, most expected we were on the verge of a downturn,” said

Phillip Wool, head of research at Rayliant Global

Advisors. “The surprising strength of the US economy makes the odds of a soft

landing much better than they were a year ago. But it’s nowhere close to a

guarantee.”

Source: WSJ Markets

“There is a question mark around whether the economy is

transitioning to a soft landing or does the labor market weaken towards a more

recessionary outlook,” said Roger Hallam, global head of rates at Vanguard

Asset Management.

No Rate Hike at FOMC Meeting September 19-20, 2023:

The Fed is widely expected to leave its (Fed Funds) policy

rate unchanged next week at 5.25% to 5.5%.

That’s after lifting it by 25 bps in July for the 10th time in an

aggressive hiking cycle that began in March 2022. The Fed is also seen as

significantly raising its forecast for economic growth in its next Summary

of Economic Projections (SEP)

report.

According to the CME Fed Watch Tool, there’s a 98% probability

of no rate change at next week’s FOMC meeting.

However, there’s a ~40% chance that rates will be 25bps to 50 bps higher

at the conclusion of the Fed’s December 2023 meeting.

2024 Interest Rate Outlook:

Along with the Fed Funds futures market, many economists

think the Fed will be cutting its key policy rate in 2024. The Fed’s June SEP report envisaged the Fed’s

favorite inflation measure, the core PCE [1.], easing markedly next year to

2.6%, which is within range of the Fed’s long-run 2% target rate (see Victor’s

comments below why that won’t be achieved).

Other economists believe inflation will be sticky until

unemployment increases significantly and GDP contracts.

Note 1. The Personal

Consumption Expenditure (PCE) price index, released each month in the Personal

Income and Outlays report, reflects changes in the prices of goods and

services purchased by consumers in the United States. Quarterly and annual data

are included in the GDP release.

Source: Hoya Capital

….……………………………………………………………………………………….

Victor’s Comments:

We all should question the paradigm change the U.S. is now

going through. Historically, huge budget

deficits have occurred during recessions and wars - not economic

expansions.

The current U.S unemployment rate at 3.8% is

considered to be “full employment” and GDP has increased in each of the

last six quarters. Yet we have record

U.S. budget deficits and national debt with NO BUDGET to slow government

spending in the future. Incredibly,

people who call for a decline in government spending are referred to as extremists?

The facts show the Fed’s arbitrary target of 2% annual

inflation is a fantasy of the highest order. Under this political fiat scheme, the U.S.

central bank monetary system will never change.

Let’s look at the CPI, which has a longer history than the

PCE, over various time periods.

l From January 2, 1914, when the Fed was created till when the

U.S. went off the international Gold Standard on August 15, 1971, the CPI

(which is UNDERSTATED) increased at 2.45% compounded annual rate over

those 57.67 years.

l From January 2, 1914, to date (110

years and 8 months), the CPI increased at a 3.17% rate.

l From 1971 to date (52.67 years), the CPI increased at 3.96%.

How does the Fed think it will bring inflation down to a 2%

annual rate in the long run? It has been under 2% for only a few minor time

periods in U.S. history. More

importantly, Milton Friedman proved that growth in the money supply-not

higher interest rates- is the major factor in controlling inflation!

As an example, Argentina’s Inflation rate just hit 124%,

while its sovereign interest rate is 118%!!! Why did the astonishing 118%

interest rate not stop inflation from hitting an all-time high? The reason is

that Argentina’s M2 increased at 87.8% YoY as of June 2023.

If U.S. government deficit spending (which has been

monetized) is not stopped … America will become a mini-Argentina.

The multi-decade high in the 10-year U.S. T- Note yield is

implying the U.S. is headed for Argentina’s hyper-inflationary dark territory.

Conclusions:

The U.S. economy has continued to defy recession predictions,

which has surprised many economists and the Curmudgeon. That’s despite the fastest and largest ever

percentage increase in rates, historically long inverted yield curve, 16

consecutive monthly declines in the Conference Board’s Leading Economic

Indicators.

As of September 14th, the Atlanta Fed’s GDP Now estimate for 3Q-2023 seasonally

adjusted annual GDP is 4.9% (or 1.23% for the quarter). That’s certainly not indicative of a

recession.

If the U.S. economy continues to grow, and inflation remains

above the Fed’s 2% target, the FOMC could hold rates higher for longer.

End Quote to Keep in Mind:

“Stock market bubbles don't grow out of thin air. They have a

solid basis in reality, but reality as distorted by a

misconception.”

….……………………………………………………………………………………………..

Be well, success, good luck and till next time………………

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever changing and arcane world of markets, economies, and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2023 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).