Despite Pledge, Bernanke’s Fed Has a Total Lack of

Transparency

by The Curmudgeon

Ron Paul's 2009 End the Fed called

for abolishment of the Federal Reserve System. In that book, Dr. Paul states that

Fed is both corrupt and unconstitutional. He argues that the Fed is inflating

our currency by creating more and more US $'s. And that was before the massive

QE programs, which went into acceleration mode in Sept 2012 with its $85B per

month of bond purchases. The CURMUDGEON sincerely believes it's time to

dismantle the Fed now and replace it by a more trustworthy government

institution.

Our argument is based on the Fed's irresponsible monetary

policy which have already caused several asset market bubbles; debasement

of our currency (by printing money such that the Fed's balance sheet is north

of $4T); lack of transparency (contrary to Bernanke's objective); and

manipulation of markets. In addition to those complaints, some

pundits say that the Fed has been leaking its policy intentions to the big

investment banks that they claim own the Fed.

Retired SCU Economics Professor Fred Foldvary

believes the U.S. economy would be better off with no Central Bank. He wrote in

an email: "In my judgment, the economy would indeed be improved if central

banking and governmental money were replaced by free-market money and banking,

as analyzed by George Selgin and Lawrence

White." Fred thinks the main cause of suppressed employment is fiscal

policy. "Taxes, mandates such as medical insurance, restrictive

regulations, and excessive litigation make labor more costly to hire, and limit

self-employment," he added.

Let's look at the total lack of Fed transparency.

‘Fed talk’ has been an obsession and the main

driving force for stock and bond markets since Bernanke’s May 22nd testimony

before Congress. Markets have ignored economic reports, valuations, investor

sentiment, etc. as they weigh every word from Bernanke's speeches, minutes of

Fed meetings, Beige Book releases, and hints from individual Fed governors.

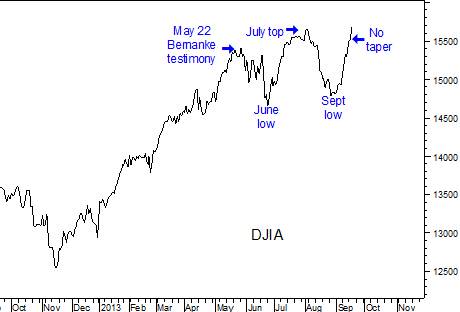

The chart below (courtesy of Street Smart Reports) shows

Bernanke's effect on the DJI average (DJIA):

The key points on the chart are as follows:

1. Bernanke’s first warning - a total surprise- of perhaps

tapering QE as early as June but certainly by September. That was in his May

22nd testimony before Congress. Result: a stock and bond market plunge.

2. Bernanke's panicked rush to calm markets at the June low,

with assurances he didn’t really mean the Fed would scale back bond

purchases/QE right away. A sharp rally to new highs.

3. The market peak at the end of July when the hints from the

Fed began again, this time that tapering might begin at the September meeting.

Result: a market plunge.

4. At the September low, assurances from the Fed that any

tapering would be only a baby step. A big rally.

5. The Fed's Sept 18th announcement that it

had decided not to taper at all produced another surprise reversal to the

upside, with the DJI, S&P 500, and Russell 2000 closing at new highs and

the NASDAQ at a 13 year high.

Closing Comment:

Think about the turning points in the chart above. Fed

Chair Bernanke has repeatedly said it wants the Fed to provide

guidance to avoid surprises and calm markets. Was such

transparency and guidance evident anytime in the past four months?

Another point to ponder: Was the stock market's September

rally BEFORE yesterday's "no taper" announcement due to leaking of

that decision to big banks on Wall Street (who may say own the Fed)?

If so, that's equivalent to massive insider trading.

How about auditing the investment bank proprietary trading desks to see when

they increased their long equity positions?

Till next time.....................

The Curmudgeon

ajwdct@sbumail.com

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.