Inflation

too High? BLS to Change CPI Calculation;

Central Banks to Meet

By the Curmudgeon with Victor Sperandeo

Introduction:

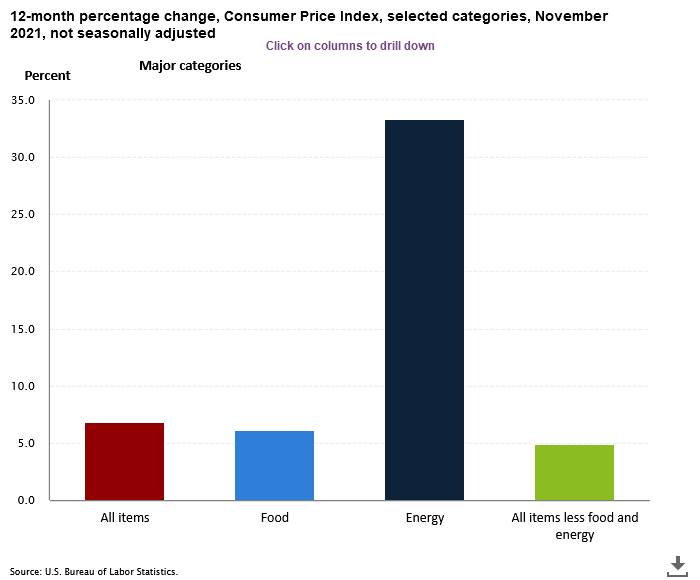

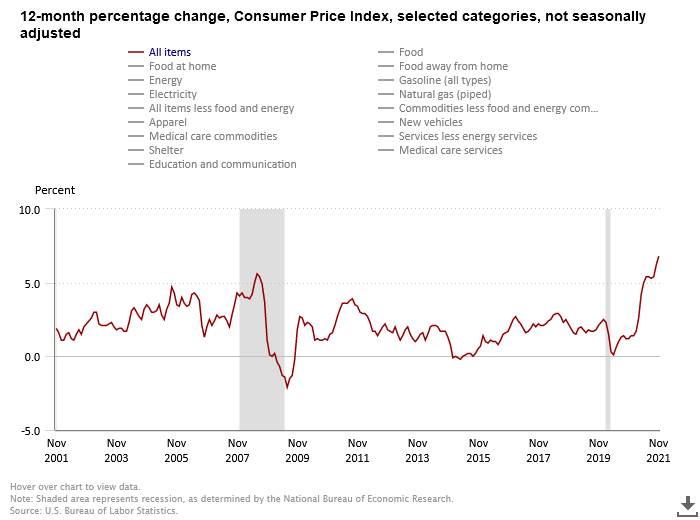

The Bureau of Labor Statistics (BLS) reported on Friday that

"the all-items Consumer Price Index (CPI) rose 6.8%

for the 12 months ending November, the largest 12-month increase since the

period ending June 1982.”

The spike in consumer prices could spell trouble for

officials at the Federal Reserve and the White House, who are trying to

calibrate policy at a moment when the labor market has yet to completely

recover from the pandemic, but price increases are proving more persistent than

policymakers had expected (Thank goodness that the term “transitory” inflation

has been retired).

We take a close look at actual vs reported inflation and the

new CPI adjustments starting next month.

There’s pressure on the Fed and the Biden administration to act. Will they?

Finally, Victor weighs in with his thoughts on this

troublesome topic along with his market comments.

CPI in Charts:

………………………………………………………………………………………….

Analysis:

In reality, the CPI is much

higher than reported by the BLS. For

example, the CPI calculation was changed in 1987 to substitute rent for house

price inflation. Home price pressures

have been swept in the purposefully nebulous Owner-Equivalent Rent. Furthermore, the reflected rent prices may be

out of date, because the BLS CPI

Housing survey collects rent data from each sampled unit every six months.

If today's CPI included house prices in its measurement, that

would surely push the headline CPI (and core CPI) to double-digit gains.

ShadowStats’ John

Williams had this to say:

Worst Inflation Since

Harry Truman Was President -- Consistent with the Methodologies of Pre-1980

Headline CPI Reporting, the November 2021 ShadowStats Alternate CPI Annual

Inflation at 14.9% Was the Worst CPI Reading Since 17.6% in June 1947,

Just Topping the 14.8% Peak of March 1980.

Consistent with Post-1980

Headline CPI Reporting Methodologies, Current Headline November 2021 Consumer

Price Index Annual Inflation Jumped to a Four-Decade High of 6.8%, Highest

Since 7.1% in June 1982 and the Days of Runaway Inflation.

The October 2021 Producer

Price Index, Finished Goods Commodity Inflation, Jumped

to a New 41-Year Peak of 12.5%, While October Annual PPI Final-Demand

(FD) Goods Inflation, and Annual and Monthly Construction Inflation Readings

Set New Historic Highs in the FD-Series Created in 2009.

BLS to Adjust CPI Calculation in January 2022:

The gap between real inflation and the reported CPI will

surely widen in coming months. That’s

because the BLS

will adjust the weights in its Consumer Price Index basket starting next month. No details were provided other than this

statement:

“Starting in January

2022, weights for the Consumer Price Index will be calculated based on

consumer expenditure data from 2019-2020. The BLS considered interventions but

decided to maintain normal procedures.”

We bet dollars to donuts that post-revision reported

inflation will decrease, because of the yet to be disclosed “adjustments."

A chronology of historical CPI calculation changes can be

found

here.

What Happens Next?

Fed officials have become increasingly concerned about

inflation, both because the uptick has lasted much longer than expected and

because it shows signs of broadening to areas less affected by the

pandemic. That raises the risk that

rapid price gains could become entrenched and create an “inflationary

psychology” that will be difficult to reverse.

“It just keeps the pressure on Fed officials,” said Kathy

Bostjancic, director of U.S. macro investor services at Oxford Economics.

As costs rise across a wider array of goods and services, the

Fed is growing more worried. In past

years, they would’ve stopped QE and raised rates months ago.

“Generally, the higher prices we’re seeing are related to the

supply-and-demand imbalances that can be traced directly back to the pandemic

and the reopening of the economy, but it’s also the case that price increases

have spread much more broadly in the recent few months,” Fed chairman Jerome

Powell, said during congressional testimony late last month. “I think the risk

of higher inflation has increased.”

Economists expect the Fed to announce a plan to slow down its

monthly bond purchases so that the latest QE program ends sooner than it

originally planned. Fed officials have

been clear that they would prefer to finish buying bonds before raising short

term (Fed funds) interest rates, which are set near zero, so that their policy

tools are not working against one another.

Alan Detmeister, a senior economist

at UBS and former chief of the wages and prices division at the Fed Board in

Washington, thinks the Fed will accelerate their reduction of bond

purchases. “It seems pretty clear that

they’re going to speed up the taper,” he

said.

Did the Fed Learn Anything from its Mistakes in the

1960s-1970s?

In the 1960s, the U.S. central bank failed to take decisive

action to tamp down rising prices. Inflation soared, rising to double-digit

levels during the 1970s, and Paul Volcker, then the Fed chair, pushed interest

rates up sharply to get inflation under control in the early 1980s. The hit to demand caused a painful recession

before it brought price gains to single digit levels. That mistake, and its

aftermath, has haunted central bankers ever since.

Yet the Fed seem to be more interested in keeping stocks and

other asset prices up (via QE and ZIRP induced liquidity) than in taming

inflation.

Biden Administration Takes Notice:

Inflation is also a political liability for the White House,

because it’s making day-to-day life more difficult for many Americans,

especially those (like the Curmudgeon) who rely on savings held in relatively

low-risk investments like savings accounts or certificates of deposit. Those

people are seeing the value of their holdings decrease and their future

purchasing power decline sharply.

President

Biden said in a statement on Friday:

“Today’s numbers reflect

the pressures that economies around the world are facing as we emerge from a

global pandemic — prices are rising. But

developments in the weeks after these data were collected last month show that

price and cost increase are slowing (?), although not as quickly as we’d like.”

“Even with this

progress, price increases continue to squeeze family budgets. We are making progress (?) on pandemic

related challenges to our supply chain which make it more expensive to get

goods on shelves, and I expect more progress on that in the weeks ahead.”

Curmudgeon asks: Who’s

kidding whom?

Victor on the “new” CPI:

So instead of the Fed raising rates, the BLS will simply

change the calculation of inflation to make it appear lower than it really

is?

Instead of adjusting to the citizens’ desire for lower

prices, the U.S. federal government tries to fool the people by changing the CPI

metrics?

→ I don’t believe that trick will work. The public will feel the bite of higher

prices no matter how the BLS calculates the CPI.

Several scenarios are possible:

1. Things continue

under an attempted cover-up of reality, which goes on longer than imaginable.

2. The Fed does

nothing but talk and threatens, while manufacturers hoard their production as

inflation accelerates exponentially while the U.S. dollar crashes as

hyperinflation begins.

3. The Fed stops lying and jawboning and ends QE, and then

quickly raises the Fed funds rate.

→ It’s critically important for the Fed to decrease

money supply growth to 6% annually. Note that Inflation was not stopped by

raising rates in the 1970’s …it was stopped by Fed Chair Paul Volker cutting

the growth of money supply in the 1980’s.

Victor’s Market Comments:

The S&P 500 closed at an all-time new high Friday (at

4,712) on lower-than-average volume (2,117,224,000 vs 3,163,982,187,

respectively). No other stock market

index is close to its all-time high. That’s a huge divergence, especially after a

non-stop rally of 20.9 months or 627 days (from 3/23/20 to 12/10/21). During that time, the S&P increased

111.74% without any intermediate corrections!

What about valuations?

·

The current S&P 500 Shiller P/E of 39.53 is the second

highest in history and way above its 1929 and 1987 pre-crash highs.

·

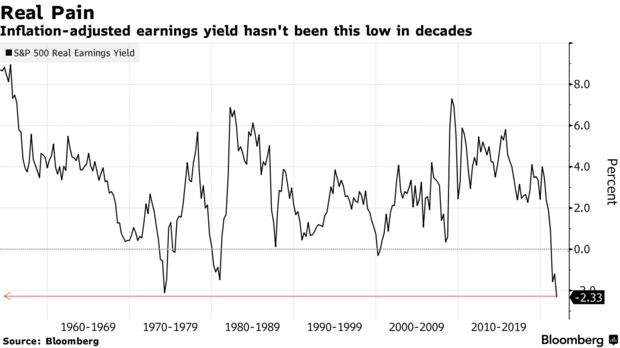

The S&P 500 Index

currently has a real earnings yield of

-2.9%, meaning that without continued growth in company earnings, investors

would lose 2.9% when adjusted for inflation, B of A strategists led by Savita Subramanian wrote in a note on

Wednesday. “The last time the real earnings yield was this negative was 1947.”

20 Central Banks Meet Next Week:

The Fed meets along with most of the world’s central banks

will meet next week. In the must read

article, “Twenty

Central Banks Hold Meetings as Inflation Forces Split,” Bloomberg says that

the Fed will confirm a quicker withdrawal of stimulus than planned just a month

ago. Fed chair Powell might even hint at being open to

raising interest rates sooner than expected in 2022 if inflation persists.

Bloomberg Economics says:

“Rising global inflation, higher commodity prices and weaker

currencies likely synchronized rate movements in emerging markets this year. Tighter

U.S. monetary policy will probably provide another global force for more rate

hikes next year.” Ziad Daoud, chief

emerging markets economist.

Closing Quote:

Perhaps this insight by a world class money manager is

sobering:

“The object is to recognize the trend whose premise is FALSE;

ride that trend and step off before it’s discredited.” George Soros

………………………………………………………………………………………………………………

Stay healthy, enjoy

life, success, good luck and till next time….

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever changing and arcane world of markets, economies and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2021 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).