U.S.

Economy is Weakening as Inflation Becomes Stickier

By the Curmudgeon

Notes and quotes this week.

Enjoy!

Stock

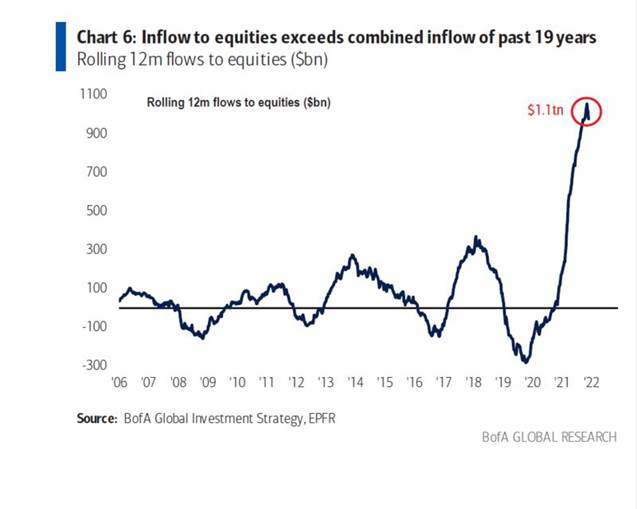

Funds Took in More Cash in 2021 Than Two Decades Combined

Investors have poured almost $900 billion into equity

exchange-traded and long-only funds in 2021 - exceeding the combined total from

the past 19 years - according to analysts at Bank of America Corp. and EPFR

Global. The amount of money

moving into the stock market dwarfed anything else this year. Bond funds

attracted just $496 billion and money market funds received about $260 billion.

It’s a data point that underscores just how extraordinary and

record-breaking this year has been. The combination of cheap money and an

economy roaring out of the pandemic set the stage of an unstoppable rally, with

frenzied retail trading and a lack of other good investment options adding fuel

to the fire.

![]() The rally has left U.S. stocks teetering at record

valuations and even some Wall Street analysts, usually a bullish cohort,

are turning bearish for next year. For investors, the debate continues

to be about how fast central banks will raise rates to combat sticky

inflation, and how badly it could potentially erode economic growth.

The rally has left U.S. stocks teetering at record

valuations and even some Wall Street analysts, usually a bullish cohort,

are turning bearish for next year. For investors, the debate continues

to be about how fast central banks will raise rates to combat sticky

inflation, and how badly it could potentially erode economic growth.

B of A Global Research: Annual inflows to active equity funds since

2013 -Flows into actively managed global equity funds ($bn):

WSJ:

Black Friday Rout Shows Dangers of Margin Borrowing

Friday’s global retreat from riskier assets exposes a

vulnerability of the broad market advance of the past year and a half: the

rising use of leverage or borrowed money.

Borrowings against portfolios of stocks and bonds, broadly

called margin debt, have grown as individual investors have become major

players in the stock market. So too have concerns that debt-fueled buying could

be a sign of overexuberance, setting the stage for tumultuous trading periods

such as Friday’s, when the Dow Industrials posted their largest-ever Black

Friday decline and the U.S. oil price dropped 13%.

Investors who have borrowed heavily to fund investments in a

rising market are more sensitive to such reversals, analysts and portfolio

managers said. At the same time, the Covid-19 pandemic has made investors more

vigilant about reducing risk whenever clear threats emerge and piling into

Treasury’s, which posted one of their strongest rallies during the pandemic era

on Friday.

Margin borrowings in October were up 42% from a year earlier

to $935.9 billion, according to data from the Financial Industry Regulatory

Authority, Wall Street’s self-regulator. Meanwhile a measure of cash holdings

among individual investors fell to 46% of margin balances, said Sentiment

Trader’s Jason Goepfert. That’s the

lowest reading in data going back to 1997.

El-Erian

Says Fed Should Recognize Inflation Isn't Transitory

Allianz SE’s Mohamed El-Erian urged the Federal Reserve to

acknowledge that inflation isn’t transitory and “ease your foot off the

accelerator starting now.”

“I think it’s time for a change in policy at the Fed,” he

said. “I was of the view that this may be easier with someone who hasn’t repeated over and over again that inflation is

transitory. Inflation is not transitory

and it’s really important for the Fed to realize this,” he added.

El-Erian has repeatedly said the Fed is underestimating

inflation risks as the U.S. economic recovery from last year’s pandemic shock

accelerates price increases for everything from energy and food to consumer

items.

The

Fed Must Think Creatively Again, Stephen S. Roach

The transitory inflation debate in the United States is over.

The upsurge in US inflation has turned into something far worse than the Federal

Reserve expected. Perpetually optimistic financial markets are taking this

largely in stride. The Fed is widely presumed to have both the wisdom and the

firepower to keep underlying inflation in check. That remains to be seen.

With inflationary pressures now going from transitory to

pervasive, the policy rate should be the first line of defense, not the final

shoe to drop. In real (inflation-adjusted) terms, the federal funds rate,

currently at -6%, is deeper in negative territory than it was at the lows of

the mid-1970s (-5% in February 1975), when monetary-policy blunders set the

stage for the Great Inflation. Today’s Fed is woefully behind the curve.

My advice to the Federal Open Market Committee: It is time to

up the ante on creative thinking. With inflation surging, stop defending a bad

forecast, and forget about tinkering with the balance sheet. Get on with the

heavy lifting of raising interest rates before it is too late. Independent

central bankers can well afford to ignore the predictable political backlash. I

only wish the rest of us could do the same.

Tweet

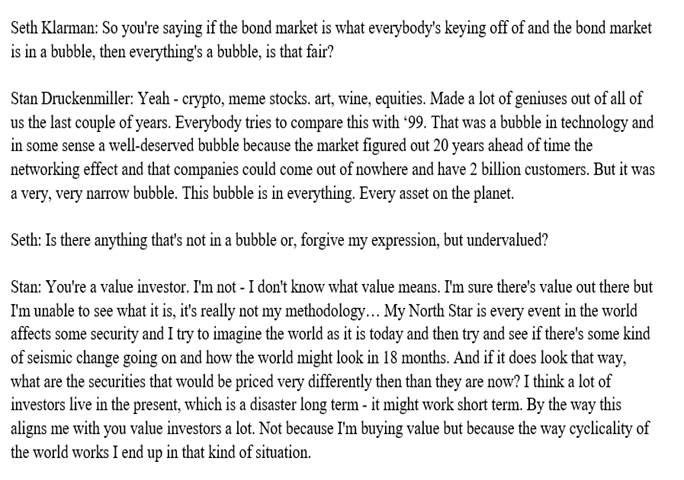

by Cundill Capital about Bubbles and Value Investing

Seth Klarman and Stan

Druckenmiller on bubbles and value investing:

Tweet by Eric Basmajian (Curmudgeon’s Reply via hyperlink)

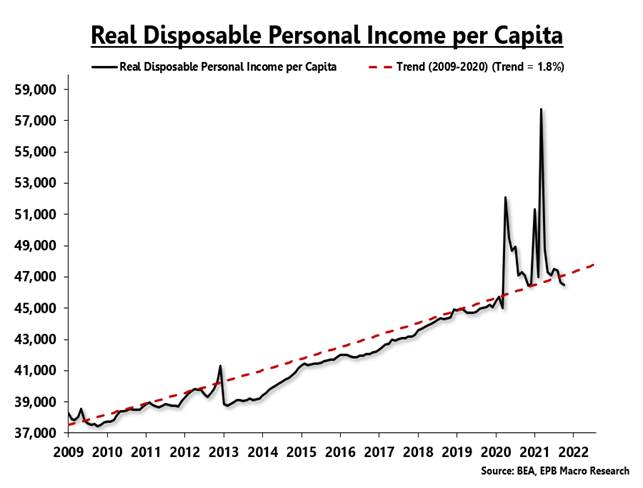

Wage gains? Real disposable personal income per capita

declined in October and is now 1.3% below the (weak) pre-COVID trendline of

1.8%. Over the last 12 years, inclusive

of all the major stimulus, real income per capita is growing less than 1.8%…

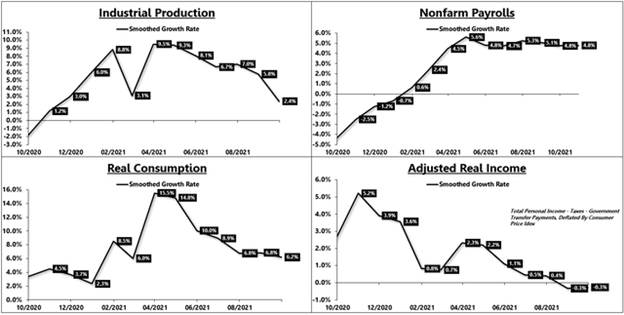

Eric’s Commentary- U.S. Economy is Weakening:

Real economic growth remains in a widespread downturn,

visible across the four major coincident indicators.

The growth rate of the Fed's industrial production index fell

sharply in the September reporting period, registering just 2.4% growth when

measured on a smoothed six-month annualized basis.

Nonfarm payrolls growth, the most lagging of the four

coincident indicators, remains steady at 4.8%, down from a peak of 5.6% in

April.

Real consumption growth has fallen from 15.5% in March to

6.2% in September when judged on a smoothed six-month annualized basis.

Adjusted real income growth, an inflation-adjusted measure of

income that subtracts government transfer payments and taxes from total income,

is negative, which highlights how inflation is outpacing income, creating

restrictive economic conditions.

Coincident Indicators of Real Growth:

Closing Quote and Image, by Hussman Funds

Across four decades of work in the financial markets, and

over a century of historical data, I’ve never observed as many historical

indications of a market peak occurring simultaneously. Noise reduction is

always a process of drawing a common signal from multiple, partially correlated

sensors, even if each individual sensor might be imperfect. The reason that we

follow boatloads of these syndromes is the same reason we base our gauge of

market internals on thousands of securities – uniformity conveys information.

Emphatically – and this is important – my intent here is not

to “call the top” of this bubble. Yes, this is a bubble in my view. Yes, I

believe it will end in tears. Yes, the price investors pay for a given stream

of future cash flows is inseparable from the long-term returns they can expect.

Yes, if this bubble is ever to have a top, this would be

a perfectly reasonable moment to expect one.

......................................................................................................

Stay healthy, enjoy

life, success, good luck and till next time….

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever changing and arcane world of markets, economies and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2021 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).