Inflation versus the Fed; AI Unicorns in 3Q-2021; a Flipping Home Fiasco

By the Curmudgeon

Introduction:

We

first look at persistent U.S. inflation vs potential Fed interest hikes. Next, our ongoing bubble watch examines

the mania in AI start-ups (perhaps the biggest bubble of them all – rivalling

the 1998-2000 dot com boom/bust). Finally, a major home flipping fiasco by one

big real estate iBuyer (a real estate company that buys and sells properties

through technology such as the Internet accessed via high speed computers).

CPI

vs the Fed:

Core

CPI soared in October, up 4.6% yoy with a broadening of price pressures. High

prices are eating away at wage growth with real wages still negative for most

workers. Last week’s 6% headline CPI

reading pulled rate hike expectations forward some more, but the market expects

only 2 or 3 hikes in each of the next two years, driving Fed Funds to

1.5%.

B

of A believes that Fed Funds could go higher than that. The double-whammy of a cost and wage push into

prices is likely leaving the Fed uncomfortable. The risks of earlier hikes –

next summer, if not before – are on the rise.

First,

with higher inflation the Fed needs to hike more to get to a neutral real rate.

Second, hiking late should mean hiking more in order to combat the additional

overheating in the economy. Third, problematic inflation will make it harder

for the Fed to stop hiking even if growth weakens.

Looking

at the last two cycles isn’t much help as the Fed took a gradual approach and

more recently, stopped raising rates as inflation and growth deteriorated. This

time around if inflation stays high and comes in above the planned overshoot,

the Fed will need to become much more hawkish and either accept a market

correction or deliberately induce such a correction. Different situation in

Europe, where B of A thinks the ECB could prematurely pull back on asset

purchases.

Source: BoA Global Research

.............................................................................................................

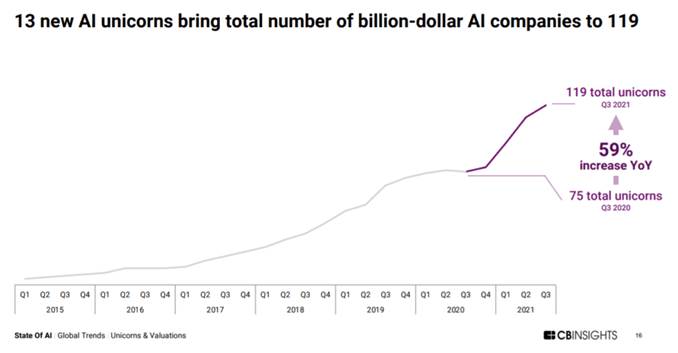

New

High in Global AI VC Funding in 3Q-2021:

AI

(Artificial Intelligence) startups notched another big quarter in a

record-breaking year for global funding, mega-rounds, unicorns, exits, and

more. CB Insights reports

that AI private market activity rose to dizzying levels in 3Q-2021.

Note: Before

we drill down deeper, note the cover story on this month's IEEE Spectrum (the

flagship publication of IEEE- the world's largest tech non-profit which

standardized WiFi, Ethernet and many other technologies). "Why is AI so

Dumb?"

Here's an excerpt:

AI has suffered numerous, sometimes deadly, failures. And the

increasing ubiquity of AI means that failures can affect not just individuals

but millions of people. Increasingly, the AI community is cataloging these

failures with an eye toward monitoring the risks they may pose.

“There tends to be very little information for users to

understand how these systems work and what it means to them,” says Charlie

Pownall, founder of the AI, Algorithmic and Automation Incident &

Controversy Repository.

“I think this directly impacts trust and confidence in these

systems. There are lots of possible reasons why organizations are reluctant to

get into the nitty-gritty of what exactly happened in an AI incident or

controversy, not the least being potential legal exposure, but if looked at

through the lens of trustworthiness, it’s in their best interest to do so.”

Part of the problem is that the neural network technology

that drives many AI systems can break down in ways that remain a mystery to

researchers.

“It’s unpredictable which problems

artificial intelligence will be good at, because we don’t understand

intelligence itself very well,” says computer scientist Dan Hendrycks at the

University of California, Berkeley.

....................................................................................................................

CB Insights: What you need to know about AI venture in

Q3-2021:

·

New record: $17.9B in global

funding for AI startups across 841 deals in Q3-2021. This marks an 8% increase

in funding and 43% increase in deals QoQ.

·

At $50B, 2021 YTD funding has

already surpassed 2020 levels by 55%. 75% Growth in megarounds

YTD.

·

The number of $100M+

mega-rounds has reached a record-high 138 in 2021 YTD.

·

There were

45+ mega-deals in each of the first 3 quarters in 2021 — the highest quarterly

numbers ever.

·

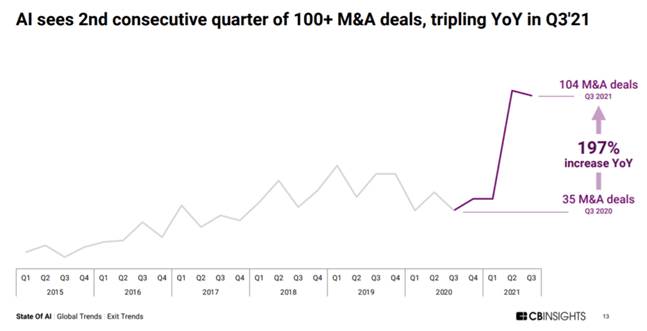

100+ AI acquisitions.

Quarterly M&A deals have surpassed 100 for 2 consecutive quarters, putting

total M&A exits at a record 253 in 2021 YTD.

·

Annual IPOs and SPACs are

also up this year. In Q3-2021, there were 3 SPACs and 8 IPOs.

·

The largest M&A deal of

Q3-2021 was PayPal’s acquisition of buy now, pay later startup Paidy for $2.7B — 370% bigger than the next largest deal. Paidy uses machine learning to determine consumer

creditworthiness and underwrite transactions instantly.

·

43% QoQ

increase in median US deal size. In Q3-2021, global markets saw strong QoQ growth in the median size of funding rounds: 43% in the

US, 64% in Asia, and 67% in Europe.

·

Across regions, median deal

size was $7M, while average deal size reached a record $33M.

....................................................................................................................

Is

Zillow's Home-Flip Fiasco a Warning Sign?

Zillo reports

that it’s stuck with roughly 7,000 homes it must sell below cost — a

loss that might total a half-billion dollars!

Zillow will quit the buy-quick-sell-quick business, sell off its homes

and cut a quarter of its staff. Wall Street wasn’t happy. It slashed Zillow’s

stock value by roughly one-third — around a $9 billion markdown.

Zillow made a massive bet its high-performance computers

could help it buy high and sell higher as an “iBuyer”

— making thousands of quick cash offers on homes in hopes of profiting from

fast resales.

Since Zillow’s a publicly traded company, the buying mistakes

they made throughout 2021 had to be disclosed to its shareholders. Not every

real estate investor — iBuyer or not — has similar

obligations to admit to such transgressions, if committed so we really don’t

know how many home flip failures have occurred this year.

However, Investors trying to make a swift buck may be badly

overpaying for homes. At a minimum,

Zillow — arguably the most aggressive homebuyer — has left the game. It’s a

good bet other investors will learn from Zillow’s missteps and be more

cautious. That means fewer highly

motivated buyers, which could cool housing’s feeding frenzy — both in how many

bids are made for homes and how much money is in those bids.

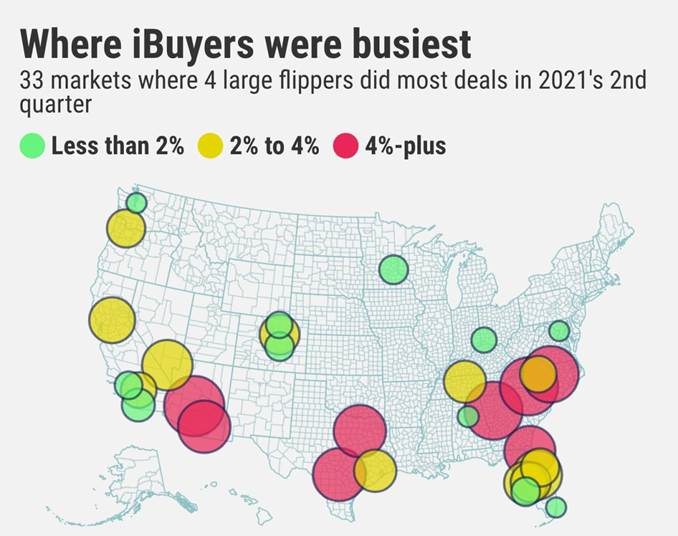

Zillow produced a study

earlier this year suggesting these quick-buy-sell investors in 2021’s second

quarter were focusing on mid-range homes in more “affordable” Southern and

Southwestern markets.

The Zillow report, tracking big four iBuyers

— Zillow Offers, Opendoor, Redfin and Offerpad— showed Sacramento was their favorite California

market, grabbing 3.3% of all purchases.

That’s the 11th biggest share among 33 markets tracked. iBuyers paid a median sales price of $513,000, 5% below the

overall market median.

Author Jonathan Lansner doesn’t recall seeing such

a level of over zealousness by a home buying speculator in in any previous real

estate cycle. The liquidation will involve Zillow’s entire 18,000-home

inventory. Buyers will likely be large investors scooping up homes in bulk and

converting them to rentals. So, listing-starved house hunters won’t likely see

any wave of “for sale” signs anywhere soon.

Zillow’s fall is a clear warning sign that some things don’t

change. “Buy high, sell higher” is a dicey concept.

End

Quote:

“What

we do know is that speculative episodes never come gently to an end. The wise,

though for most the improbable, course is to assume the worst.” John Kenneth

Galbraith

......................................................................................................

Stay healthy, enjoy life, success, good

luck and till next time….

The Curmudgeon

ajwdct@gmail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a historian, economist and financial innovator who has re-invented himself and the companies he's owned (since 1971) to profit in the ever changing and arcane world of markets, economies and government policies. Victor started his Wall Street career in 1966 and began trading for a living in 1968. As President and CEO of Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and development platform, which is used to create innovative solutions for different futures markets, risk parameters and other factors.

Copyright © 2021 by the Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing article(s) written by The Curmudgeon and Victor Sperandeo without providing the URL of the original posted article(s).