Fed Ignores Inflation Spike, Panic/Euphoria Index,

Energy Prices, and a Secular Bull Market in Commodities

By the

Curmudgeon with Victor Sperandeo

Introduction:

Once again, we bring you the best from financial and economic

thought leaders via commentaries and charts/tables. Victor’s comments are inserted Enjoy!

WSJ Opinion - Does the Fed Have the Will to Fight

Inflation? By Jason De Sena Trennert

[Please refer to Curmudgeon’s Conclusions below for additional

clarity on this topic]

The Fed’s policy of quantitative easing (QE) injures

middle-class savers. People without financial assets get kneecapped by the

policy known as “financial repression”—purposefully attempting to pay for

government spending by keeping interest rates below the rate of inflation. This

policy has been a boon for the wealthy but a disaster for average people, who

earn no return at all on their savings.

While the Fed has talked about slowing down the pace of its

asset purchases (known colloquially as tapering), it is important to remember

that it is still technically easing. This leads us to wonder whether the Fed

can raise rates again without significant pain and major dislocations in the

global economy.

The sheer size of financial assets today relative to the size

of the economy suggests that the tail may be wagging the dog. Any significant

decrease in the price of securities is likely to damage consumer confidence. A

reported 56% of U.S. households hold common stocks either directly or through

retirement accounts, and the correlation between confidence and stock prices

has grown. Total financial assets in the U.S. now represent 565% of

gross domestic product.

Victor says: With the Biden administration’s $3+ Trillion

spending program in the works, the Fed must print more dollars (QE) to

buy the additional U.S. government debt that will result from increased deficit

spending.

Bloomberg - Stagflation Fear Is Having a British

Renaissance, by John Authers:

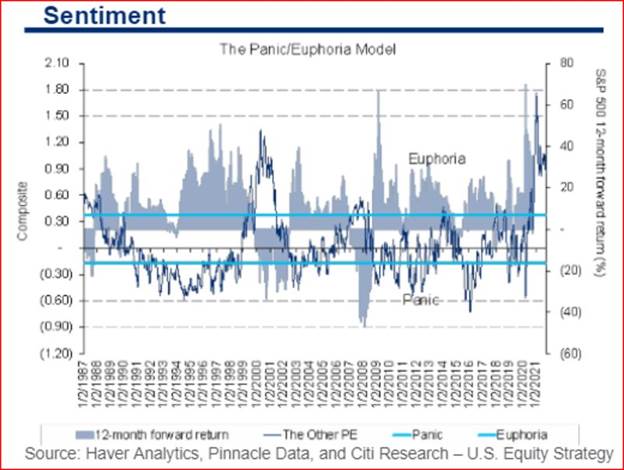

The “panic/euphoria” model, which I have followed

quasi-religiously for longer than I care to contemplate, is the ultimate

contrarian sentiment indicator. You should buy when the market is in panic and

sell when it is euphoric. Here it is, with the levels of the “P/E” over time,

and the subsequent 12-month performance by the equity market:

This was the verdict from last week’s Panic/Euphoria

index, presumably written by a Citi Research analyst: “Panic/Euphoria

declined but remained in euphoria territory this week and is generating a 96%

historical probability of down markets in the next 12 months at current levels.

This week’s Panic/Euphoria was 0.85 compared to an upwardly revised 0.91 in the

prior week. Panic territory is defined as -0.17 and lower, while euphoria is

0.38 and higher…. Nasdaq Volume as % NYSE (though volatile), margin debt, gas

prices, and put/call premiums all contributed to the elevated reading.”

Whether ironically or appropriately, this favored contrary

indicator has been sending some of its most bearish signals ever in the

last few months. This should be taken seriously.

Bespoke

Commentary and Charts (via email):

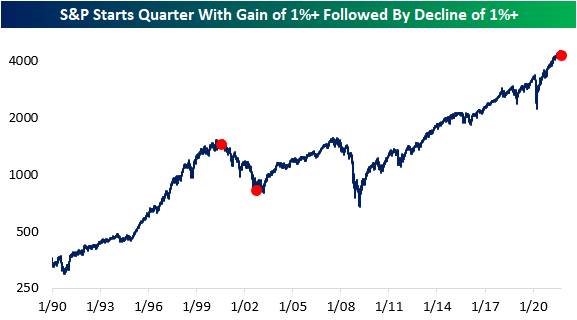

The

S&P 500 started the quarter with a gain of over 1% and subsequently

declined 1% the following day. This has only happened two other times since

1990. As shown below, the first

occurrence came near the peak of the Dot Com bubble, while the second came near

the end of the Dot Com bust.

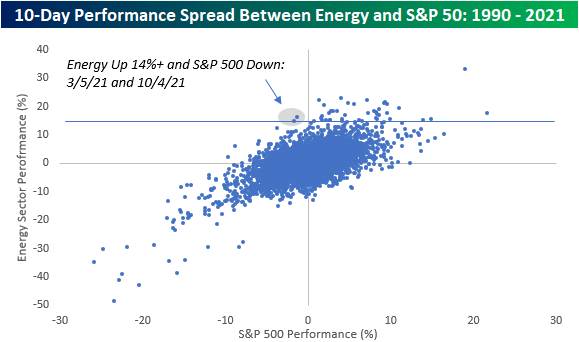

As of October 5th, the Energy sector was up 14% while the S&P

was down over the prior 10 trading days. This is only the second time this

has happened since 1990. The other occurrence was in March of this year. With the Energy sector's weighting in the

S&P 500 now below 3%, it can experience big moves without moving the broad

market hardly at all.

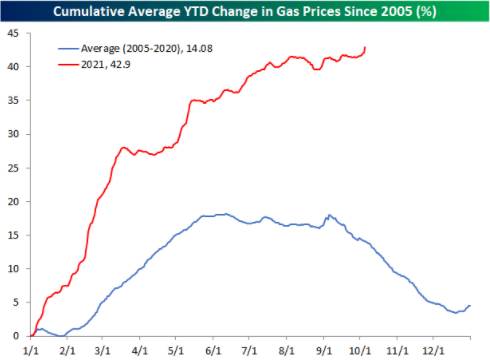

Oil and gas prices remain very elevated relative to where they

started the year, and prices have continued to rise recently which is normally

a time of year when prices begin their seasonal downtrend.

Victor says: Energy prices have been rising at an outstanding

pace this year (+63.4% YTD as of October 8, 2021). Of course, this was to be expected as the

Biden Administration canceled the XL Pipeline in his first week in office along

with federal leases for exploring and developing natural gas.

B of A Global Research concurs: High energy prices are likely to stick, with upside risks

in both the short and medium term. They

are part of a larger "inflation tax" that is slicing roughly 1.5% off

real household incomes.

The energy price increase has been broad based. Oil, natural

gas, and coal account for a large majority of the world's energy consumption.

Of these, Dutch natural gas futures have seen the most dramatic spike as per

this graph (courtesy of BoA Global Research):

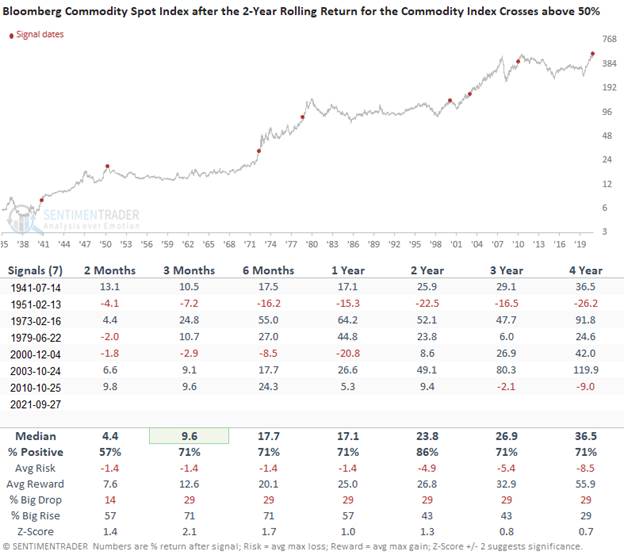

Sentiment

Trader: Did We Just Start a New

Secular Commodity Bull Market, by Dean Christians

The 2-year rolling return for the Bloomberg Commodity Spot Index

recently crossed above the 50% level. If we use history as a guide, should we

expect a new secular commodity bull market? The outlook suggests

commodities have entered a new secular uptrend.

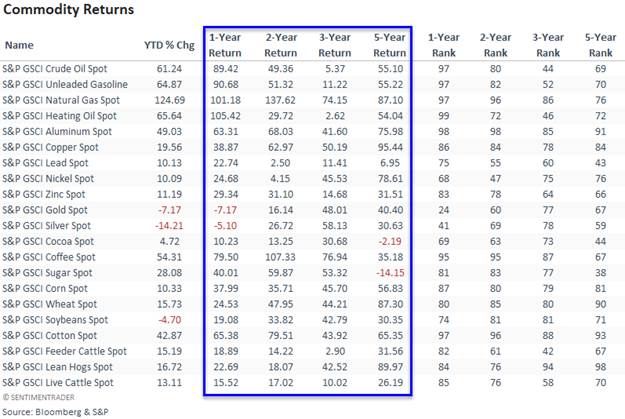

The following table provides the rolling returns for the S&P GSCI

Commodity Spot Indexes. The current uptrend in commodities is an everything

rally. Each component has a positive two and three-year rolling return, and

only two maintain a negative one and five-year return. The rank measures the current rolling return

relative to all other values in history-100 highest to 0 lowest.

The weight-of-the-evidence is building to suggest that we should be

mindful that the current uptrend in commodities may not be a cyclical

phenomenon but rather a new secular trend.

If commodities are indeed in a new secular uptrend, the implications for

portfolio positioning are at a critical juncture. Mind the opportunity.

Curmudgeon Says: Any commodity bull market will be kept

in check by a continued high in the U.S. dollar. The DXY dollar

index made a new 52 week high

this past Wednesday, October 6th at 94.44. It closed the week on Friday, October 8th

down a few ticks at 94.10.

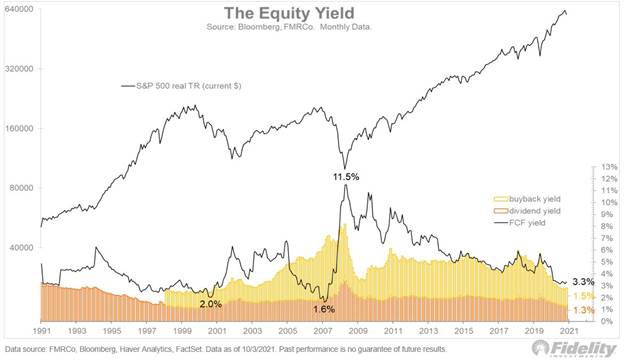

Jurrien Timmer of Fidelity via Twitter:

With the S&P 500 trading at 20x forward earnings (estimates are

almost always too high), cash flows come at a price. The free-cash-flow

(FCF) yield is now a mere 3.3%, with most of that going to dividends (1.3%)

and buybacks (1.5%). Remember, FCF is after capex and before dividends.

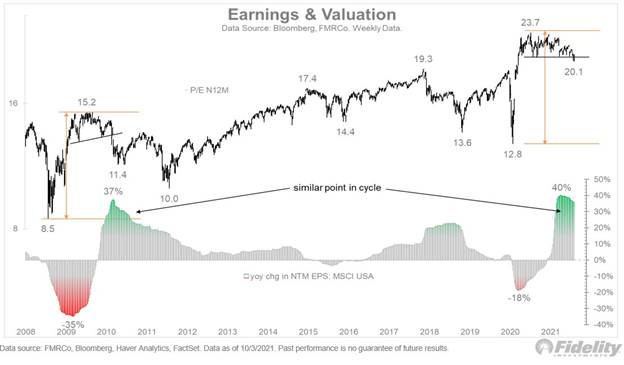

Valuation vs earnings growth: We seem to be

revisiting 2010, a year into the post-GFC bull market, when QE1 ended while

expected earnings growth peaked. That’s what’s happening now. Back then it

produced multiple-compression. We’re seeing that again as per the chart below:

Curmudgeon's Conclusions and Charts:

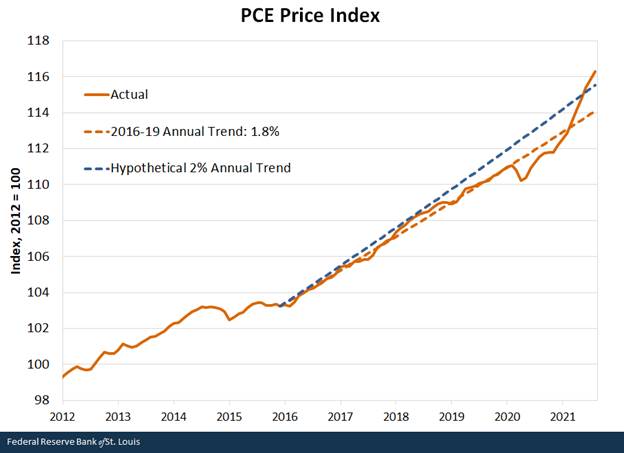

1. It's truly

amazing that the Fed has ignored their favorite inflation guage (PCI) by

continuing QE and ZIRP. A taper announced at the November FOMC

meeting will be too little and too late

to stop inflation from accelerating!

Check out this graph from the St. Louis Fed:

Victor says: Energy prices are going up. At the same time,

the U.S. federal government continues to spend. President Biden seems

determined to keep his ambitious social spending plan close to $3 trillion,

which will increase aggregate demand and result in higher inflation in the

U.S. Hence, inflation will not be

"transitory," as Fed Chairman Jerome Powell has often claimed.

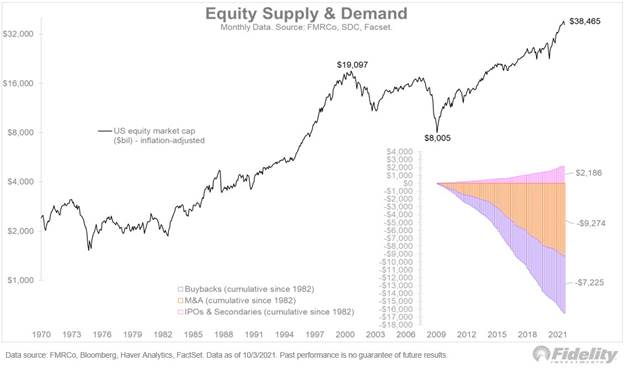

2. Supply and

Demand for U.S. Stocks:

Demand for shares in this 11+ year old bull market came mostly from corporate buybacks/M&A. Since the March

2009 low, $2.2 trillion of supply from IPOs and secondary offerings were more

than offset by $7.2 trillion of buybacks & $9.3 trillion from M&A

activity. That’s an 8-to-1 demand/supply ratio!

Chart courtesy of Jurrien Timmer of

Fidelity:

.......................................................................................................................

Stay healthy, enjoy life, success, good luck and till next

time….

The Curmudgeon

ajwdct@gmail.com

Follow

the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor

Sperandeo is a historian, economist and financial innovator who

has re-invented himself and the companies he's owned (since 1971) to profit in

the ever changing and arcane world of markets, economies and government

policies. Victor started his Wall Street

career in 1966 and began trading for a living in 1968. As President and CEO of

Alpha Financial Technologies LLC, Sperandeo oversees the firm's research and

development platform, which is used to create innovative solutions for

different futures markets, risk parameters and other factors.

Copyright © 2021 by the Curmudgeon and

Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the original

posted article(s).