Will

the Fed’s New Monetary Policy Stimulate the Economy and Inflation?

By Victor Sperandeo with

the Curmudgeon

Summary of Fed’s Policy Shift:

Federal Reserve Chairman Jerome Powell announced a major monetary policy shift on Thursday, August 27th at the Fed’s annual (vacation) conference in

Jackson Hole, WY. Changes in the Fed’s

methods for inflation targeting and measuring maximum employment are contained

in Federal Open Market Committee (FOMC) approved updates to its Statement on Longer-Run Goals and Monetary Policy

Strategy. That document articulates its approach to

monetary policy and serves as the foundation for the Fed’s policy actions.

The most significant change was a shift to “average

inflation targeting.” The U.S.

central bank will be more inclined to allow inflation to run higher than the

standard 2% target before hiking interest rates, especially if inflation had

previously been below 2% for an extended period of time.

The revised Fed statement says that "following

periods when inflation has been running persistently below 2 percent,

appropriate monetary policy will likely aim to achieve inflation moderately

above 2 percent for some time." No quantification of the “moderately above 2

percent” inflation rate or time period above 2 percent

were given.

The Fed believes that inflation that is too low can

weaken the economy. When inflation runs well below its desired level,

households and businesses will come to expect this over time, pushing

expectations for inflation in the future below the Fed’s longer-run inflation

goal. This can pull actual inflation even lower, resulting in a cycle of

ever-lower inflation and inflation expectations.

Of course, the opposite is also true—high inflation

expectations result in still higher (often accelerating) inflation. But that

was the story in the 1970s and early 1980s.

Inflation may return, which will be a surprise to many. But not to those who’ve

forecast hyperinflation in coming years.

In addition to the inflation change, the Fed shifted

its approach to gauging employment.

The FOMC said that its policy decision on “maximum employment”

will be informed by its “assessments of the shortfalls of employment from its

maximum level.” The original FOMC document referred to "deviations from

its maximum level." Again, no

number given for what the Fed considers to be “maximum employment,” which for

most of the 20th century was considered to be

~4% of the work force.

The updates to the Fed’s strategy statement

explicitly acknowledge the challenges for monetary policy posed by a persistently

low interest rate environment. In the United States and around the world,

monetary policy interest rates are more likely to be constrained by their

effective lower-bound than in the past.

The reason for that constraint is that the Fed (and

other central banks) can’t cut interest rates to fight

a recession if they are already ultra low, zero, or

negative!

Victor’s Comments:

Will the Fed accomplish its goal— this time? The question is did

they really mean what they said?

The Fed often deceives the public for political

gains. One example of such deception is driving up stock prices via a surge of

Fed created liquidity (from the purchase of financial assets with “money

created out of thin air”). That does

nothing to grow the real economy, but instead enriches politicians and

corporate executives, while widening income inequality.

Another example of deception, discussed in item 1. below, is paying interest on Fed member

bank reserves, which has resulted in a crash of money velocity to all-time

lows. That aids the banks, but weakens

the real economy as explained below.

Victor’s Prescription: The Fed could do two things to stimulate the economy and

increase inflation to above 2 percent:

1. The Fed,

working together with the U.S. Treasury, could drive the U.S. dollar back down

to 72.70 (May 2011 low) from its current 92.27 (on the DXY September futures

contract). That would necessitate direct

intervention in foreign exchange markets, something which is almost never

discussed or publicized.

2. Stop paying

banks interest on their free (excess) reserves [1.] and instead, pay the

banks 1% for every dollar they loan out.

Even though the current rate is only 10bps (see Note 1. below), it would

show some integrity from the Fed.

Note 1.

Interest on Bank Reserves:

The Financial Services Regulatory Relief Act of

2006 authorized the Federal Reserve Banks to pay interest on balances held

by or on behalf of depository institutions at Reserve Banks, subject to

regulations of the Board of Governors, effective October 1, 2011. The effective

date of this authority was advanced to October 1, 2008, by the Emergency

Economic Stabilization Act of 2008.

The Fed pays interest on BOTH required reserves and

excess reserves. The current rate is 10bps (0.10%) on each class of

bank reserves.

…………………………………………………………………………………………………...

When the Fed failed over 8+ years to achieve its 2%

inflation target, it was truly deception to the nth power! Paying member banks interest on reserves

(IOR) was, and is in effect, a mandate for banks to

“NOT loan money.” With decreased

commercial and personal loans, money turnover (velocity) declined and the

economy didn’t grow.

Any first-year student of economics knows, it is the

“velocity” of (paper) money that creates inflation! A pile of fiat currency that just sits (as

reserves in a Fed bank vault) does not cause inflation, no matter how big it

is! Instead, the Fed needs to stimulate

bank lending [2.]

Note 2. Fed

Member Bank Reserve Ratio reduced to 0%:

The Fed has taken one step to stimulate bank

lending. As the COVID-19 pandemic

started to shut down the U.S. economy, the Fed reduced reserve requirement

ratios to zero percent effective March 26, 2020. This action eliminated reserve requirements

for all depository institutions. Prior

to that change, reserve requirement ratios on net transactions accounts

differed based on the amount of net transactions accounts at the depository

institution.

With no requirement to maintain reserves for dollars

loaned, banks have an incentive to loan more of their capital.

………………………………………………………………………………………………..

Clearly, there’s no

inflation NOW with the coronavirus lockdowns pushing prices lower. The CRB Commodity Index made a 25+ yearly low

on 4/21/20 which reflected a - 42.8 % DECLINE for the year. That sharp drop was

aided by oil going into a unique negative price on the May futures

contract. However, that may change

if the U.S. dollar continues to weaken (most commodities are priced in

dollars).

……………………………………………………………………………………………..

Classic Examples of Inflation:

In 1920 Weimer Germany the velocity of their money

supply was 1.5. (For comparison, M2 in the U.S. is currently 1.1; down from 1.4

at the beginning of the year).

By 1923 inflation in Germany was +29,525.71%

in one month, as velocity increased to “12.”

This means the money supply in 1923 Germany turned over 12 times a year,

up from 1.5 times a year in 1920.

Source: “When Money

Dies” -Adam Fergusson

It should be noted 1946 Hungary holds the

inflation record 1.295x10 to the 16th power or 129,500,000,000,000,000% in one

month. Prices doubled every 15.6 hours.

This is why the Modern Monetary Theory (MMT) proponents never

want to use government “printing money” in their explanation of what MMT theory

does. Instead, they euphemistically say government “spending.” It’s all about

selling/marketing their MMT proposition rather than the actual reality of the

inflation that would result if it were to be implemented. This seems to be really

simple to understand, but how many people get the message?

Victor’s Conclusions:

1. The Fed’s inflation targeting deception made it

look like it wanted to see moderate inflation (by setting a goal of 2%). However, they created a policy, where it

could never hit that goal.

Why? Because the Fed wanted the equity and bond

markets up, citing the “wealth effect” which it “believed (?)” would

increase GDP growth. As we now all know,

that did not happen, i.e. GDP growth has been below trend since the 2008-2009

recession ended and the subsequent 11 year economic “recovery” was the weakest since

World War II.

Remember, the secret owners of the Fed (a

private corporation) – those unnamed individuals or financial institutions that

get a guaranteed 6% dividend each year with no risk – own large amounts of

shares in U.S. stocks. So when the Fed props up the stock market, its owners

directly benefit!

2. It is my observation that anywhere you look, the

rule of law has been discarded and abandoned. That includes: the FBI, DOJ, CIA, STATE DEPT

and even the Supreme Court (under Chief Justice John Roberts et al). Just two examples:

·

Fed buying Corporate Bonds

and Bond ETFs is illegal according to the 1913 Federal Reserve Act.

·

The forced closure of

businesses in most states due to the COVID-19 pandemic is also illegal without

a referendum as per the constitutions of those states, e.g. California. The pandemic has been cited as a “Force

majeure” event for the state or local government to shut down their economies

and impose additional restrictions on companies.

Closing Quotes:

John Locke was a major inspiration to the Founding

Fathers. His writings are especially

timely now, with the rule of law being ignored.

These words, written by John Locke, philosopher, in

1689, begin a proposition around which all of us are reminded that we are under

“the sovereignty of the law.”

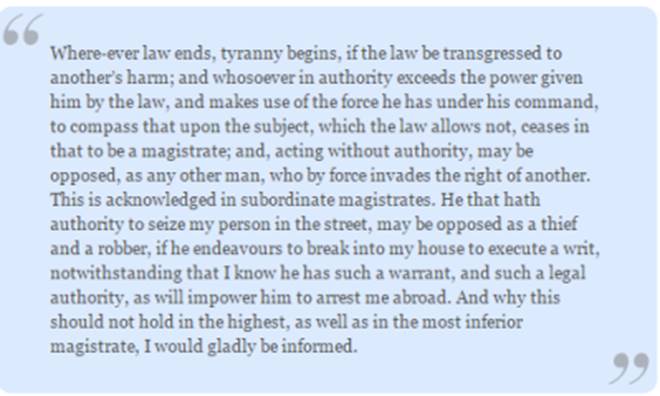

“Wherever law ends, tyranny begins.”

“It is by the customs and practices of the law that we all live and thrive, and

just societies need the rule of law for justice and order to prevail. This

usually arises by the state ensuring that the judiciary are independent of its

work, such that government can also be held accountable for its actions,” blog

post by James Wilding.

……………………………………………………………………………………………………………

Be well, healthy, and safe. Good luck and till next

time……..

The Curmudgeon

ajwdct@gmail.com

Follow

the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been

involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor

Sperandeo is a historian, economist and financial innovator who

has re-invented himself and the companies he's owned

(since 1971) to profit in the ever changing and arcane world of markets,

economies and government policies.

Victor started his Wall Street career in 1966 and began trading for a

living in 1968. As President and CEO of Alpha Financial Technologies LLC,

Sperandeo oversees the firm's research and development platform, which is used

to create innovative solutions for different futures markets, risk parameters

and other factors.

Copyright © 2020 by the Curmudgeon and

Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating,

copying, or reproducing article(s) written by The

Curmudgeon and Victor Sperandeo without providing the URL of the original

posted article(s).