Real Estate Rebound Won’t Survive Without Fed’s QE

by The Curmudgeon

For many months, we've argued that the Fed's QE experiments have been counter-productive. They've inflated financial assets without meaningfully lowering unemployment or increasing economic growth, wages or standard of living. However, we do acknowledge that the Fed-produced artificially low mortgage interest rates have encouraged refinancing while making housing more affordable by lowering monthly mortgage payments. That has resulted in a residential real estate recovery that has increased home prices as well as overall economic activity.

Is the housing market now in danger of being derailed as a result of the run up in mortgage interest rates (which many have attributed to Ben Bernanke's remarks about the end of "tapering," i.e. cutting back on the Fed's $85B per month of bond purchases)?

This May, housing starts came in at an annualized 914,000 units, which was below the Briefing.com estimate of 925,000, but above the 856,000 in April. Building permits came in at an annualized 974,000, in line with Briefing.com estimates, but falling short of the more than one million in April. We think that might be a temporary top!

The interest rate on a fixed-rate 30-year mortgage has been trending up since hitting an all-time low of 3.47% late last year. The trend accelerated after Bernanke's May 22nd statement about possible QE tapering and again this week after the Fed Chairman‘s press conference. Rates were quoted as high as 4.5% on Friday June 21st.

In a recent WSJ blog

post, Phil Izzo wrote:

"The biggest initial negative macroeconomic impact

from higher rates is likely to come from slowing refinancing activity.

Historically low rates and rebounding house prices have enabled thousands of

homeowners to lower their monthly mortgage payments, freeing up more cash to

spend elsewhere. Refinancing activity has already slowed and the higher rates

go, the more it will dry up."

"But as long as rates don’t shoot up too far too fast, they aren’t likely

to seriously damp the housing market."

The post concludes by stating, "The key to the

equation is the speed at which rates move. If they climb higher at a measured

pace, a stronger housing market will likely absorb it and continue to grow. But

if there’s a swift move up, all bets are off."

The CURMUDGEON is not that confident in housing's continued recovery; because we believe the increase in rates has already reached a tipping point. We think the economy is likely to slow further, because of the incipient slowdown in the housing market.

Analysis and Conclusions:

There's evidence that a large number of participants in the residential real estate market have been "professional" cash and speculative buyers, rather than people who will actually live in the homes they purchase. (We see advertisements for home flipping seminars all the time.) That speculative activity may slow down or come to a dead stop with the sharp rise in rates that's already taken place.

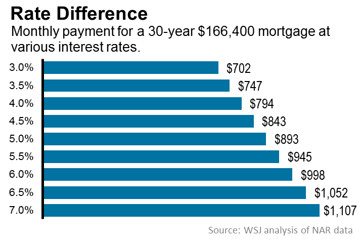

If you are not a "professional" home flipper and

want to buy a house in the US and you need a conventional mortgage, and if you

are not a speculator and want to live in dwelling, your costs have now risen

substantially as shown in the table below:

The CURMUDGEON believes that the higher interest rates will also slow the resolution of the foreclosure document mess at the big mortgage banks. The housing finance mechanism in the US is not fixed and won't be anytime soon. In fact, it's becoming more imbalanced with the Fed buying ever more MBS' each month. And that comes on top of the U.S. government majority ownership of FANNIE MAE and FREDDIE MAC, which makes the U.S. government the indirect owner of most mortgages in this country! (One friend claims that this is just one of several examples of the U.S. turning into a socialist country. Excess regulation is another, but that's a story for another time).

Housing, finance, mortgaging, and the recovery in the US

will see a setback. How severe that setback will be remains to be seen. One result might be a decrease of several

hundred thousand single-family housing starts a year. Another might be a large decline in sales of

existing homes. Home prices are not

likely to continue to advance as they have for most of the last 12 months.

Uncertainty and risk to the glacially slow economic recovery are now higher than they were just a few weeks ago. This is partially due to the Fed's failure to clearly communicate its QE tapering intentions, which have led to higher interest rates on all fixed income securities. But more significantly, it's due to the financial markets heroin- like addiction (stronger than crack-cocaine) to easy money. The negative withdrawal symptoms of that addiction were readily apparent late last week with the global bond and stock sell-off after Bernanke's June 19th press conference.

The CURMUDGEON's longtime friend and colleague Victor Sperandeo said, "Bear in mind that the Fed is using "Moral Persuasion" to talk the markets down. They haven't yet sold any of the MBS's or Treasuries they've purchased in recent years. So "good news is bad news" and vice versa. If the U.S. economic numbers decline from here, interest rates will follow and also decline."

Financial market uncertainty is likely to drive interest rates up further in coming weeks and months, which will dampen economic activity.

Going forward, the policy options available to the Fed will become much more difficult. They have boxed themselves into a corner and have no silver bullets left to fight the next housing bust or recession. They already have distorted financial markets, created misallocation of capital, global imbalances, and the potential huge problem of unwinding its bond purchases when inflation starts to pick up again. But that's the day after tomorrow's problem, isn't it?

Till next time......................................

The Curmudgeon

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.