Margin Debit is a Double-Edged Sword

by The Curmudgeon

On May 24th,

the New York Stock Exchange (NYSE) reported margin debt statistics for April

2013. As expected, April's margin debt

hit a new high at $384.37B -- a 1.3% gain from the previous month, a 29% rise

from the same month last year, and above the previous all-time high

in June 2007 of $384.10B. NYSE

member brokerage firms report the levels of margin debt held against client

accounts monthly. The data can be found here.

The rising

level of margin debt is seen as a measure of investor confidence, as

speculators are more willing to borrow to make (or maintain)

"investments" when share prices are rising. In effect, they have more

$s worth of financial assets in their portfolios to borrow against. The latest

rise has been fueled by record low interest rates and a 17% year-to-date

stock-market rally (with flat to down corporate profits and GDP limping along

at <2%). In essence, greed is feeding

on itself as speculators take on more leveraged long positions.

Given the stock

market had very strong gains in May, we are almost certain that current margin

debt has reached a substantially higher all-time high. But there's more, much more......

·

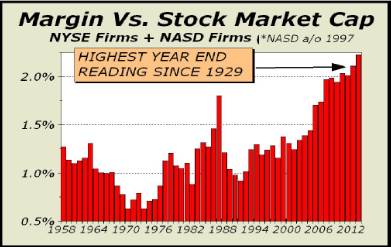

According

to Alan Newman of Cross-Points: "When measured versus GDP, margin debt is

at the same levels the market reversed and collapsed in 2000 and 2007. But even

those comparisons pale in the face of the chart below, showing margin debt

relative to total stock market capitalization."

Chart Courtesy of Cross-Currents

·

Total

NYSE volume has dried up considerably since the last market peak in Oct 9,

2007. For example, total NYSE volume on

Oct 19, 2007 was 2,625,101,750 shares traded.

Contrast that to this year, where an average of ~1T shares has been

traded each day (Source: NYSE).

That's over a 40% decline in average daily volume on the NYSE! It means that less trading has been driving

stock prices up, but that can work in reverse too.

·

The

NYSE Margin - to -Volume ratio in April 2013 is more than 2 1/2 times what it

averaged in October of 2007. This

implies that in a down market, it will take much fewer shares traded (than in

2007) to cause forced selling due to margin calls. [Note that forced selling can also come from

mutual fund redemptions, since mutual fund cash has been consistently

below 4% of assets- even as assets increased due to rising stock prices].

·

FINRA

reported

that the sum of all Debit Balances in margin accounts (the amount of

money margin account customers owe the brokerage firm) also made a new high in

April, reaching a staggering total of $408.677B. Compare that with the bear market low in

March 2009 when that number was only $21.8B!

·

More

startling was that FINRA's Free Credit Balances in customers' margin

accounts hit a new low for this year in April, at $191.719B! When you subtract that number from April's

Debit Balances you get $216.958B of net leverage- another all-time high!

·

In a

somewhat academic report

on this topic, Alhambra Partners states: "Banks and brokers can “create”

cash out of nothing, through margin balances. The relative comparison between

cash in brokerage accounts and margin usage reveals more depth to investor

sentiment. In the big picture, extremes in cash vs. margin match up

extremely well with market inflections (major highs or low in stock

prices)." There are some very

interesting historical charts within that article, which illustrate previous

extremes in cash vs. margin debt led to market inflection points.

What's not

known today is how much margin debt has been used to purchase leveraged

securities that trade on the NYSE, like ultra-long ETFs and leveraged closed

end funds. Other types of speculation

are also possible. An advisor quoted in

the WSJ said "he advised a client to use margin debt to help finance

flipping houses, since the client could borrow money more quickly on margin

than he could by taking out a different type of loan."

Another huge unknown

is how much margin is used in so called "black pools," which trade

off the exchanges, e.g. HFT and investment bank to investment bank computerized

trades. We are concerned that during a

severe market decline, off exchange trading will all but cease, which would

exacerbate any sell off.

Closing

Comment: Any way you want to look at it, leverage

being used today is staggering. Has

everyone forgot what happens when speculators get a "margin call" due

to falling prices of the securities they own using borrowed money? There now seems to be little margin for error

(pun intended) in a down market, before forced selling is required. That could

create a downdraft that might spin a healthy pullback into a more significant

correction, a mini-crash, or even a protracted bear market.

Till next time.....................................

The Curmudgeon

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.