U.S. Budget Deficit Rising (Should be

Falling); Impact on Borrowing and Interest Rates

by the Curmudgeon

Introduction:

Strong jobs report, initial

unemployment claims at 49 year low, 2nd quarter GDP at 4.1% with

many previous quarters revised up. The

Labor Department’s broadest measure of unemployment, which includes workers

forced to take part-time jobs because full-time positions are unavailable, fell

to 7.5 percent in July, the lowest since 2001. Indeed, the U.S. economy is in the midst of the longest monthly streak of job growth in

history.

One would think the federal

budget deficit should be shrinking with such strong economic numbers. WRONG!

In its latest budget review,

the Congressional Budget Office (CBO) states:

“The U.S. federal budget

deficit was $607 billion for the first nine months of fiscal year 2018. That was $84

billion more than the shortfall recorded during the same period last

year. The CBO estimates that the deficit

for fiscal year 2018 (which ends on September 30, 2018) would total $793

billion, about $127 billion more

than the 2017 shortfall. “

The CBO is projecting that

the deficit will keep rising to $973 billion (4.6% of projected GDP) in fiscal

2019 and just over $1 trillion (also 4.6% of GDP) in fiscal 2020. By 2028 CBO projects that the budget deficit will

hit $1.5 trillion by 2028, resulting in a cumulative deficit of $12.4 trillion

over the 10-year period from 2019 to 2028.

The Office of Management and Budget said

this month that it had revised its forecasts from earlier this year to account

for nearly $1 trillion of additional debt over the next decade — on average,

almost $100 billion more a year in deficits.

The increased budget deficits

are largely due to last December’s GOP tax bill, which introduced a standard

corporate income tax rate of 21%, down from a high of 35% (top rate which few

companies paid) and allowed companies to immediately deduct many new

investments. As companies operate with lower taxes and a greater ability to

reduce what they owe, the federal government is receiving far less than it

would have before the overhaul.

The Trump administration had

said that the tax cuts would pay for themselves by generating increased revenue

from faster economic growth, but the White House has acknowledged in recent

weeks that the deficit is growing faster than it had expected. This

is not at all happening!

“That’s part of the equation

people haven’t been talking about,” said Ian Lyngen,

head of U.S. government bond strategy at BMO Capital Markets. “The notion that tax reforms are going to

pay for themselves is being tested right now.” Really?

Corporate tax-rate reductions

are restraining federal government revenue, because less tax is being generated

for every dollar of household and business income earned. The Treasury

Department said last month that tax receipts fell 7% in June from the same

month a year ago, including a 33% drop in gross corporate taxes.

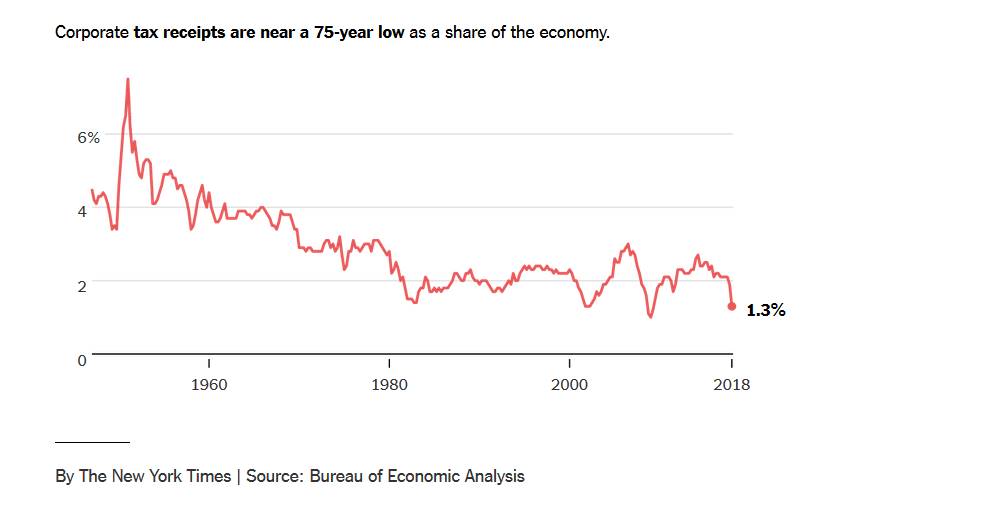

Worse, the Treasury

department data indicated that from January to June this year, corporate tax

payments fell by a third from the same period a year ago. The drop nearly

reached a 75-year low as a share of the economy, according to federal data as

indicated in this graphic:

……………………………………………………………………………………………………………………………

U.S. Trade Deficit

Increases- Who Cares?

Pundits rarely talk about the

ballooning U.S. trade deficit, yet it still has to be

financed (largely by foreign purchases of U.S. Treasury securities and foreign

direct investment). The U.S. trade

deficit in goods and services expanded in June at the fastest rate since

November 2016. It increased 7.3% in June from the previous month to a

seasonally adjusted $46.35 billion, the Commerce Department said Friday.

The U.S. economy has run

overall trade deficits for decades, during both economic expansions and

recessions. Many argue that trade deficits imply that Americans are living

beyond their means and accumulating too much debt (which at some point in time

must be repaid or defaulted on).

Budget Deficit Impact on U.S. Treasury Auctions and

Interest Rates:

The WSJ reported

Thursday August 2nd:

“Rising federal budget

deficits are boosting the U.S. Treasury’s borrowing and could restrain a

fast-growing economy as the cost of credit rises, too.”

The Journal article notes

that Treasury Department would increase auctions of U.S. debt by an additional

$30 billion over the next three months. That included higher sales of two-year,

three-year and five-year notes and the introduction of a new short-term

security with a two-month maturity. In all, the Treasury plans to borrow $329

billion from July through September—up $56 billion from the agency’s April

estimate—in addition to $440 billion in October through December. The figures

are 63% higher than what the Treasury borrowed during the same six-month period

last year.

In addition to the moves with

the notes and bonds, Treasury said it will consider increasing the auction

amount for its Treasury Inflation Protected Securities.

"Treasury will assess

the need to make further adjustments to auction sizes at the next Quarterly

Refunding in November based on projections of the fiscal outlook at that

time," the department said in a statement.

The U.S. national debt is officially at $21.3 trillion, having risen

about $800 billion in 2018. That debt is

financed through additional U.S. government Treasury auctions. Fed officials have privately discussed the

debt issue, and Chairman Jerome Powell on multiple occasions has said the

fiscal trajectory is "unsustainable."

The size of U.S. government

borrowing in coming years is hanging over the bond market. In addition to the

increased spending forecast for the federal government, there is concern about

lower tax revenue. Many analysts and

investors expect these developments will ultimately lead to higher borrowing

costs for the U.S. government.

“Everyone thinks we won’t have a problem financing

trillion-dollar deficits until we have one,” said Brian Edmonds, head of Treasury trading at Cantor Fitzgerald LP.

The effect of increased debt

levels “depends on how many people want to buy your debt,” said Don

Ellenberger, head of multi asset strategies at Federated Investors.

The U.S. has benefited from

“safe haven” demand for Treasury’s from Europe and Asia, which has kept

borrowing costs relatively low. Till

now. What happens next?

Questions to Ponder, Things of the Past or No Worries?

· Whatever happened to the bond market vigilantes? [Bond market institutional investor who

protests monetary or fiscal policies he considers inflationary by selling

bonds, thus increasing yields.]

· And what about the crowding out effect [Increased U.S. treasury

auctions would crowd out private sector borrowing].

· How can the U.S. dollar be seen as a safe haven/flight to quality investment when

it's really a flight to junk? That’s

considering the spiraling U.S. budget deficits and increased national debt that

must be financed by an ever increasing supply of

Treasury securities.

· If the budget deficit is rising

rapidly during strong economic growth with low unemployment/jobless claims,

what will happen to deficit when there's a severe recession? Government outlays always increase during a

recession while tax revenues plummet as profits decline or turn into losses.

· If no recession, but intermediate to

long term interest rates return to their historical average with a real yield

3% above the nominal inflation rate, will the government be able to finance the

increased deficits/national debt at those significantly higher rates? If not, will there be a flight from the U.S.

dollar as a “safe haven” for foreign money?

GDP Growth Not as Advertised, by John Williams of Shadowstats:

Guest

commentator John Williams argues that the lack of U.S. deficit improvement

reflects a less-than booming economy with strong GDP not confirmed by other

metrics. Here’s his unedited remarks:

Purportedly, all is

booming in the U.S. economy these days, yet there are some reasons to be a bit

skeptical. Removing the effects of

inflation, second-quarter 2018 real Gross Domestic Product (GDP), the broadest

measure of U.S. activity, stood 17.4% above its pre-Great Recession peak

activity at the end of 2007. After

fourth-quarter 2007, the GDP began is worst tumble since the Great

Depression. It hit bottom in 2009,

recovered its pre-recession peak in 2011 and has been expanding happily ever

since.

The problem is that no

other major “hard” economic measure confirms that margin of boom, and some

industries, such as manufacturing and housing/construction, still are down

meaningfully, never having recovered their pre-recession highs.

If the GDP is soaring,

so too should be the number of employed people supporting it. The economy is up 17.4% from its prior high,

yet the level of civilian employment is up by just 6.4% in the same

period? The strongest conventional

economic measure other than the GDP appears to be real retail sales, up by

8.8%, but that is bloated, being deflated by understated CPI inflation.

“Soft” economic

measures such as growth in “intellectual property,” “legal and brokerage

services” and “health care services” are higher, but they are not measured

meaningfully and generally do not lead economic activity.

………………………………………………………………………………………………………

End

Quote from the Peter G. Peterson Foundation:

Federal

debt is already at its highest level since 1950 and is projected to nearly

equal the size of our economy by 2028. Debt at such levels is unsustainable.

Unless

policymakers act, CBO concludes that rising debt could jeopardize long-term

economic growth, crowd out critical investments, reduce policymakers’

flexibility to respond to unforeseen events, and raise the risk of a fiscal

crisis.

This

dangerous path of federal debt remains a critical issue for our economy, and

changes to spending and tax policies are necessary to put the nation on a

sustainable path.

………………………………………………………………………….

Good luck and till next time…

The Curmudgeon

ajwdct@gmail.com

Follow the

Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2018 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).