Strong

Earnings Power Stocks Rapid Rise in 2018…or Maybe Not?

by the Curmudgeon

The S&P 500 gained 1%

this past week, 5.1% this year and was only marginally down in two of 14

trading days in 2018. The NASDAQ

Composite is up 6.3% while the Russell 2000 (+1.3% on Friday) is up 4% in the

first three weeks of 2018. Those are

respectable gains for an entire year, especially when inflation is averaging only

~2% and valuations are near or above all-time record highs (e.g. DJI price/book ratio=12.93 (IBD

Jan. 22, 2018 pg. B6), Russell 2000 trailing P/E=141.63, S&P 500 Shiller

P/E=33.9, median Leuthold 3000 trailing P/E = 24.3x (now higher) which is ABOVE

the previous all-time high recorded in March 1998).

A WSJ Podcast I heard Sunday morning attributed the gains to “strong

corporate earnings reported this week.”

Is that really true? Are analyst’s forward earnings estimates too

high?

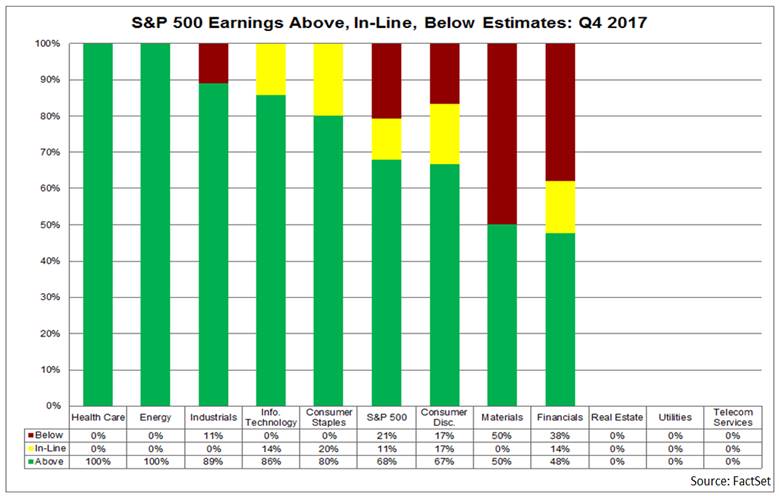

1. Excerpts of FactSet’s Earnings

Update (January 19, 2019):

To date, 11% of the companies

in the S&P 500 have reported actual results for Q4 2017. In terms of

earnings, fewer companies are reporting actual EPS above estimates (68%)

compared to the five-year average. In aggregate, companies are reporting

earnings that are 53.0% below the estimates, which is well below the five-year

average.

The blended (combines actual

results for companies that have reported and estimated results for companies

that have yet to report) earnings

decline for the fourth quarter 2017 is -0.2% today, which is much lower

than the (forecast) earnings growth rate of 10.0% last week.

Looking at future quarters,

analysts currently project earnings to grow at double-digit levels through

2018. The forward 12-month P/E ratio is

18.4, which is above the five-year average and the 10-year average.

Source:

S&P 500 Earnings Season Update: January 19

………………………………………………………………………………………………

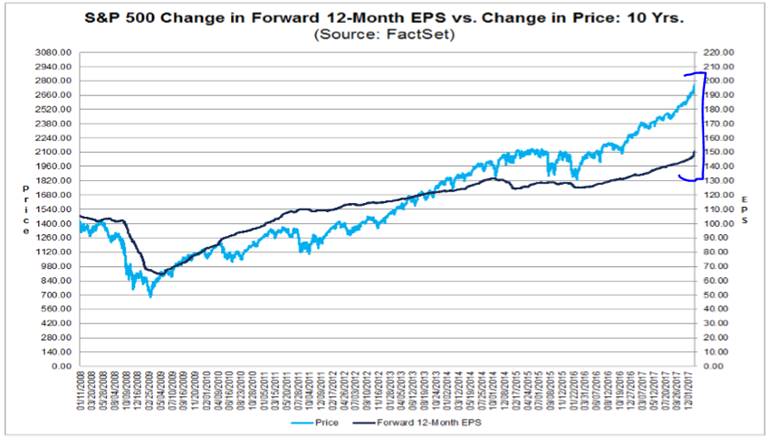

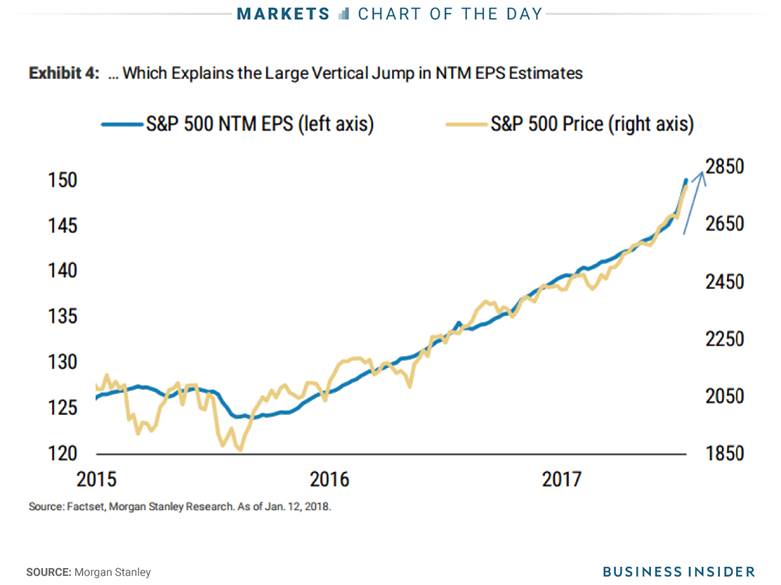

2. The chart below from Business Insider (subscription

required) shows the steep rise in analysts EPS estimates (which have proven to be

way too high as per FactSet note above) are tracking S&P 500 stock prices

rather than actual earnings.

………………………………………………………………………………….

3. Here’s an analysis by Societe

Generale Bank from a note to clients last week:

*

S&P 500: price rise due mainly to P/E expansion:

Since Trump’s election, the S&P 500 is up by 33% (now higher). As we highlight in our 2018

Equity Outlook, this move has been mainly driven by valuation expansion in

anticipation of the impact of tax reform and accelerating US GDP growth

expectations (Bloomberg consensus forecast for 2018 has been revised up from

2.1% to 2.6% since the election).

Indeed, 2018 S&P500 EPS expectations have been flat since

November 2016 (at $145) and the 2018 P/E ratio has jumped from 14.4x to 18.6x.

*Are

US companies delivering strong EPS growth?

US companies have not yet delivered any impressive numbers since

Trump’s election. It is true that 12-month trailing earnings are up by 13%, but

this is mainly a catch-up effect from companies that were loss-making in 2016

(c.5% of the S&P500 index earned a loss in 2016, mainly oil companies but

also some tech names). The chart below compares the MSCI US EPS calculation

(which takes into account the losses) with the DataStream

U.S. EPS calculation (which puts losses as nil profits), and the picture is

very different over the recent period.

According to DataStream, US EPS calculations are only up by 6%,

well below the eurozone earnings growth number (9%).

*We

remain wary of the S&P500:

Given the asymmetry in the market (lots of good news on prices,

underestimated risk, etc.), we remain wary of the expensive US equity market.

……………………………………………………………………………………………………

Closing Comments:

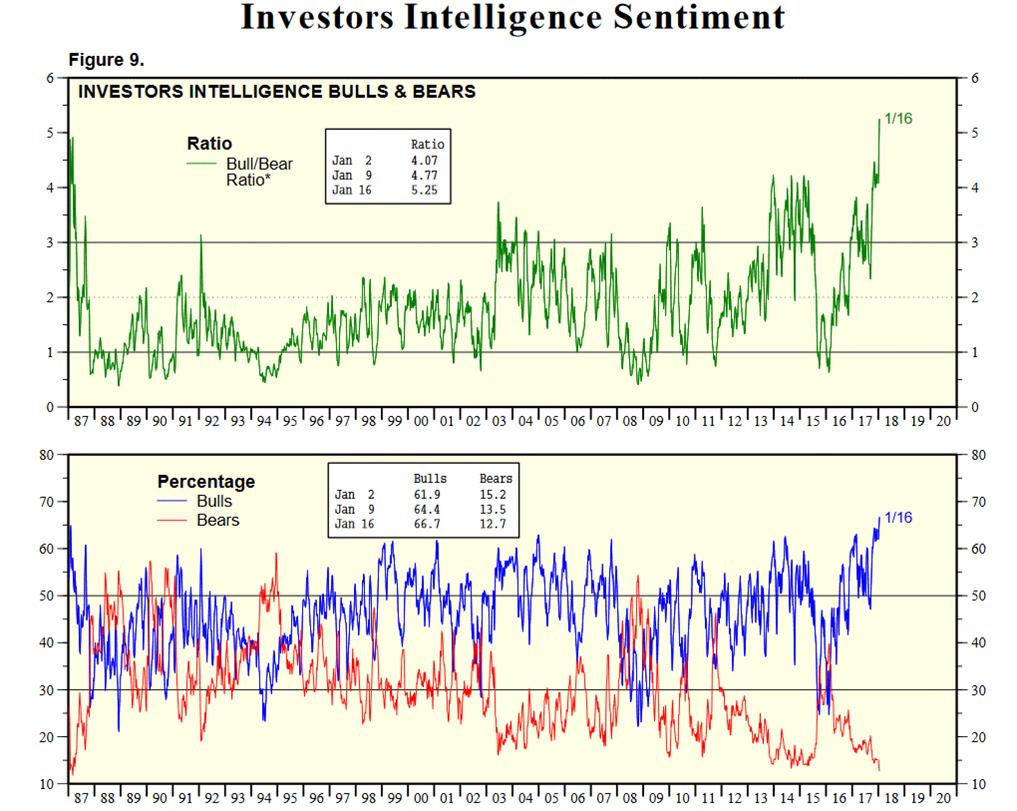

1.

Few

have reported the incredibly bullish sentiment numbers from Investors Intelligence. As of their

January 17, 2018 survey, there were 66.7% bullish advisers and only 12.7%

bearish advisers. That puts the

Bull/Bear ratio (normally a contrary indicator) at an all-time high of 5.25 as

per this chart:

Source: Yardeni Research Inc.

2.

Since

Trump was inaugurated in January 2017, there’s been a huge disconnect between

strongly rising U.S. stock prices and a falling U.S. dollar. The U.S. dollar index (DXY) has declined

for six consecutive weeks and is down over 10% in the last year.

If

investors are so optimistic about U.S. economic growth and increased corporate

profits, you’d expect the dollar to rise- not fall- during the same period as

stocks were marching ever higher (without even a 3% correction since November

2, 2016). That’s even more true as U.S.

interest rates have risen to multi-year highs with the 10-year T Note closing

Friday at 2.66% and the 5-year T Note at 2.053%. Those rates are considerably

higher than foreign government sovereigns with the same maturities. A falling U.S. dollar feeds domestic

inflation, which is already rising. That in turn squeezes profit margins and

reduces real earnings growth.

So,

who is right – stock market bulls or U.S. dollar bears?

Good luck and till next

time...

The Curmudgeon

ajwdct@gmail.com

Follow the

Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and

received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2018 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).