Eurozone Recession Could Cause Big Banks to Fail and

Trigger “Bail-Ins”

by the Curmudgeon

Overview of Eurozone's Sputtering Recovery:

Most knowledgeable people are aware that the U.S. has

experienced the weakest economic “recovery” in the post WWII era. Last Saturday's Wall Street Journal lead

story (on line subscription required) said the pace of the U.S. economic

expansion has been by far the weakest of any since 1949. But few Americans know that the Eurozone’s

“recovery” has been equally weak!

On August 1st, the Associate Press reported

(via the San Francisco Chronicle) that the Eurozone, which is made up of 19

countries that use the Euro single currency, suffered a sizable slowdown in the

second quarter despite a number of extraordinary stimulus measures that the

European Central Bank (ECB) has engaged in. Eurostat, the EU’s

statistics agency, said that 2nd quarter growth across the Euro

currency bloc eased to a quarterly rate of 0.3% from the previous quarter’s 0.6

percent. The Eurozone’s growth was equivalent to the 1.2% annualized rate also

reported Friday for the United States.

Most forecasters think Brexit will weigh to some degree

on growth over the coming months, especially if the discussions around the exit

drag on. Few think annual growth will be much more than a modest 1.5 % this

year and next. As a result, many economists think the ECB will back a further

stimulus package at its next policy meeting on September 8th.

“The weakening in economic growth, together with the

downward revisions in expectations for the outlook are setting the scene for

more stimulus measures,” said Danae Kyriakopoulou, managing economist at the

Center for Economics and Business Research in London. Ms. Kyriakopoulou says that the ECB will

probably expand its bond-buying stimulus program rather than further cut its

interest rates, which has the potential to undermine banks profitability.

The Curmudgeon has repeatedly claimed that such QE/debt

monetization/ bond buying has been counter-productive to economic growth while

pumping up and hyper inflating financial assets to unbelievable levels.

Message to ECB Prez Mario

Draghi: Continuing to do what doesn't

work is the definition of insanity!

European Banks Under Stress?

Let's suppose that current and future ECB stimulus fails

and the Eurozone collectively sinks into recession (some European countries

have been in a recession for years). How

would European banks hold up, especially in light of their continued non performing/bad

loans with no interest rate cushion to boost profits?

Last Saturday's NY Times analyzed that situation in an

article titled: “Stress

Tests Find Some Big European Banks Wanting.” The article starts by stating that “European

regulators announced that new stress tests found that a handful of the region’s

biggest banks would struggle in a severe economic downturn or in the next

financial crisis.” The latest European

stress tests examined the balance sheets of 51 European banks, representing

about 70% of the region’s banking industry.

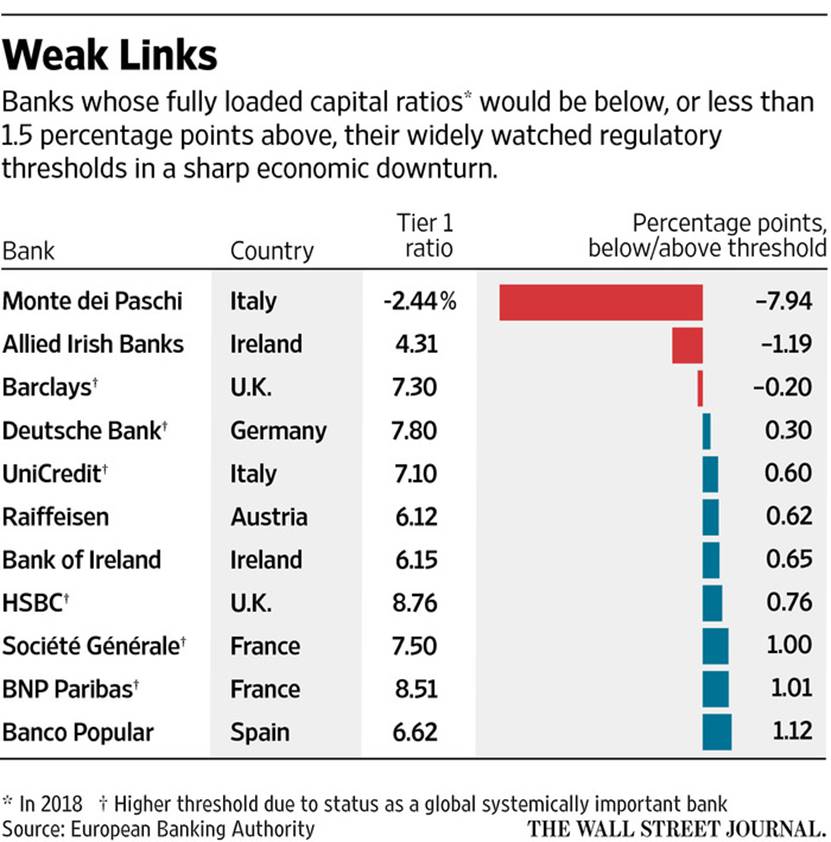

Banca Monte dei Paschi di Siena, Italy’s oldest and third largest bank, was the worst

performer in this year’s stress tests. Its capital fell to negative in a crisis

situation modeled by the European Banking Authority, which regulates

lenders in the European Union. Allied

Irish Bank and the Royal Bank of Scotland were among the other banks

with so-called Tier 1 capital ratios that declined sharply in the tests. And

among the region’s larger banks, the Tier 1 capital ratios of the Italian big

bank UniCredit, Barclays of Britain and

Deutsche Bank of Germany would all fall below 8% in the hypothetical

economic crisis that was modeled by the European Banking Authority. Please refer to the table below, courtesy of

the Wall Street Journal.

Under this year’s simulations, bank balance sheets were

tested against the impact of a macroeconomic downturn over three years, in

which real gross domestic product would decline by 1.2% in the European Union

in 2016, fall by a further 1.3% in 2017 and recover slightly in 2018.

The

biggest impact came from credit losses; banks across the region suffered

cumulative losses of €349 billion. The results also forecast market risk losses

of €148 billion and a cumulative loss of €105 billion from so-called conduct

risk.

The

European Banking Authority examination also found that the average return on

regulatory capital for banks in the test sample was 6.5% at the end of 2015,

which is below the cost of equity and return on equity that banks consider

sustainable long term, the regulator said.

“This data shows that profitability remains an important

source of concern and a challenge for the EU banking system, in a context of

continued low interest rates, high level of impairments linked to large volumes

of nonperforming loans, especially in some jurisdictions, and provisions

arising from conduct and other operational risk related losses,” the European

Banking Authority said in its report.

Italy's Troubled Banks:

As Victor pointed out in item 8. of a recent Curmudgeon post, concern

is mounting about the ability of Italy’s banks to deal with hundreds of

billions of euros in problem loans. As

noted above Banca Monte dei Paschi

is among the most troubled of Italy's banks with UniCredit

not far behind. It's important to note that smaller Italian “banks on the

brink” were not covered by Friday's stress tests, even though they're

struggling with 360 billion euros ($400 billion) in loans gone bad.

The size of nonperforming loans on the books of Italian

banks come to €360 billion (Source: NY Times article referenced above). According to the Bank of Italy, about €210

billion of those loans are held by insolvent borrowers, and an additional €150 billion

are loans that are considered unlikely to be repaid, past due or in breach of

an overdraft ceiling. Some of those loans could ultimately be repaid.

Fixing the banks is crucial for Italy and the wider

Eurozone, because financially weak banks are more reluctant to lend out money

to households and businesses, stifling the potential for economic growth needed

to create jobs. Also, saving banks has in the past overwhelmed some Eurozone

states' public finances, such as Ireland in 2010. With Italy ranking as the

third-largest Eurozone economy, any crisis of confidence over the state's

financial health has the potential to rekindle concerns about the overall

currency's integrity.

European Bail-Ins:

New European rules, adopted after the 2008-2009 financial

crisis, require bondholders to take much of the losses before a

government-backed bailout can be put in place.

Such a process is known as a “bail-in,” which we've covered in several

Curmudgeon posts last year.

The key new rule is that no bank can be bailed out with

public money until creditors accounting for at least 8% of the lender’s

liabilities have stumped up. So-called bail-ins typically mean wiping out

creditors’ investments, slashing their value or converting them into shares in

the bank. Uninsured depositors could get caught along with professional

investors.

The threat of “bail-ins” could have a major impact on the

confidence of investors in Italy, as many small investors there hold bank

bonds.

Hugo Dixon of Reuters wrote a superb

analysis of “bail-ins” earlier this year.

Here's an excerpt:

The theory is that

shareholders should take the first hit because they know they are risking their

money. If that isn’t enough to stabilize the bank, subordinated bondholders

should step up because they too should know such investments are risky. Next in

line are senior bondholders and, finally, uninsured depositors – which, in the

EU, means those with more than 100,000 euros in their accounts. The small

depositors should not be touched.

Unfortunately, bail-ins are

harder in practice than in theory. A big test came during the Cypriot crisis of

early 2013. The euro zone’s initial instinct was to tax all depositors, big and

small, to fill the gap in bank balance sheets. Although that bad idea was

abandoned, large depositors suffered singeing losses, helping cause a steep

recession.

Other countries do not want to

repeat the Cypriot experiment. No wonder Italy and Portugal rushed to rescue

some of their troubled banks before the tough new regime kicked in at the start

of January.

Not that Rome and Lisbon had a

free hand over what to do. Since mid-2013, the commission has said public money

could only be used to bail out lenders if shareholders and subordinated

bondholders shared the burden. Still, this was not as tough as the new 8% rule,

which could require senior bondholders and uninsured depositors to take a hit

too.

Italy's PM:

Bail-Ins NOT WANTED Here!

On August 2nd (today), Italian Prime Minister

Matteo Renzi said

he wanted to avoid a "bail-in" -- the use of creditor or depositor

money to restructure banks. That was

just two business days after Banca Monte dei Paschi secured a last-minute, privately-funded bailout,

which includes the sale of 9.2 billion euros ($10.3 billion) in bad loans and a

5 billion-euro capital increase.

"For me Italy is totally fighting for avoid bail-in

because also soft bail-in could be a disaster for the credibility and for the

confidence," Renzi said in an interview

with CNBC.

Renzi came under heavy criticism last year when a similar

burden-sharing plan was used to restructure four small banks, because some of

its subordinated bondholders whose money was bailed in were ordinary savers who

did not know their risk. One committed suicide.

Having to use the EU's new bail-in rules now would open

the Italian PM up to political risks he probably does not want to take ahead of

a referendum on constitutional reform later this year that may be crucial to

the survival of his government.

"I will win," Renzi said of the referendum in

the same interview. "But I think people need to understand what

instability will follow."

Summary & Conclusions:

1. The key take-aways from this post are that: the

Eurozone economy is very weak, monetary stimulus is not only ineffective but

counter-productive for economic growth, a few European banks won't be able to

survive a pro-longed recession, and bail-ins would result with many bank

bondholders and depositors taking a “haircut.”

2. The entire financial world is in an Alice in

Wonderland mode of operation, or even worse- a Kafka dream.1 The explosion in global debt

(especially since 2009) undermines economic growth and the world has never been

more indebted. Led by Japan, debt levels

of many countries have reached levels far higher than 90% of GDP.

While there's been a nonstop race to the bottom by the

world's central bankers (the Fed, ECB, BoJ, BoE, etc.) without any meaningful

or effective fiscal policies, the global economy remains incredibly weak --

more than seven years into a so called “economic recovery.” Equally important, many big banks would not

be able to survive a severe recession.

Their failure would trigger bail-ins that no one likes.

…………………………………………………...

Note 1. In Franz Kafka's

short story “A Dream,” the narrator describes a dream in which Joseph K.

is walking through a cemetery. There are tombstones around him, and the setting

is typically misty and dim.

……………………………………………………

3. Trying more of

the same with bond buying (all big central banks), perpetual debt and ETF

buying (BoJ), negative interest rates (ECB, BoJ, etc.) actually wrecks a

nation/regions financial system and puts big banks under much more pressure then they are now with ultra-low (or negative) interest

rates.

We wonder if our great global central banker “friends”

have seen the movie Dumb and Dumber?

End Quote:

In his opening narrative for each TV episode, Rod Serling would say: “Next

stop, the Twilight Zone.” Let's update

that to what today's central bankers might say in their opening remarks: “Next

stop, Helicopter Money2!”

Note 2. Podcast: QE

and Helicopter Money Questions Answered

Good luck and till next time...

The

Curmudgeon

ajwdct@sbumail.com

Follow the

Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has

been involved in financial markets since 1968 (yes, he cut his teeth on the

1968-1974 bear market), became an SEC Registered Investment Advisor in 1995,

and received the Chartered Financial Analyst designation from AIMR (now CFA

Institute) in 1996. He managed hedged equity and alternative

(non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2016 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from

duplicating, copying, or reproducing article(s) written

by The Curmudgeon and Victor Sperandeo without providing the URL of the

original posted article(s).