Avago-Broadcom

Deal Ignores Risks of Debt Propelled Acquisitions

by the Curmudgeon with Victor Sperandeo

Analysis of the Avago-Broadcom Deal:

“We have seen a slowdown in top buying (economic) growth

rates. So one of your options to at least generate growth on the bottom

line is to do accretive deals..... This deal could mark the start of a new

string of mega-mergers in the tech industry,” said Christopher Rolland of FBR &Co. Of course, he was referring to Avago Technologies proposed $37 billion

buyout of semiconductor heavy weight Broadcom. "Money is still cheap. So those dynamics

are sort of coming together to cause this consolidation," Rolland added.

Broadcom, based in Irvine, Calif., was founded in 1991 by

Henry Samueli, PhD - an electrical engineering professor at the University of

California, Los Angeles (UCLA) and Henry Nicholas III (Samueli's

PhD student) who left the company in 2003. Mr. Samueli, the owner of the

Anaheim Ducks hockey team, is Broadcom’s chairman and chief technology

officer.

Broadcom's revenues last year were nearly twice the size of

Avago’s. The acquisition would take

Avago into new semiconductor markets, including cable modems, TV set-top boxes,

Wi-Fi and data center switching systems. Broadcom is by far and away the leader in Ethernet

switch chips for equipment in both premises and cloud based data centers as

well as telco and campus networks.

“This is a landmark day in the history of the industry,”

said Scott McGregor, Broadcom’s 58-year-old CEO, during a conference call on Thursday.

"Today's announcement marks the combination of the

unparalleled engineering prowess of Broadcom with Avago's heritage of

technology from HP, AT&T (Microelectronics), and LSI Logic in a landmark

transaction for the semiconductor industry," Avago CEO Hock Tan said in a

statement. "Together with Broadcom, we intend to bring the combined

company to a level of profitability consistent with Avago's long-term target

model."

Avago Technologies plans to finance its $37 billion purchase

of Broadcom, with $15.5 billion of new

syndicated term loans. Financing

will come from Bank of America Merrill Lynch, Credit Suisse, Deutsche Bank,

Barclays, and Citigroup, sources said.

The issuer expects to refinance $6.5 billion of existing debt facilities

and raise $9 billion of new money. A $500 million revolver would be undrawn at

closing. The transaction would leverage Avago at roughly 2.7x, giving full

credit for $750 million of synergies. Net of $1.3 billion of cash on hand,

adjusted leverage would fall to 2.5x, according to an investor presentation.

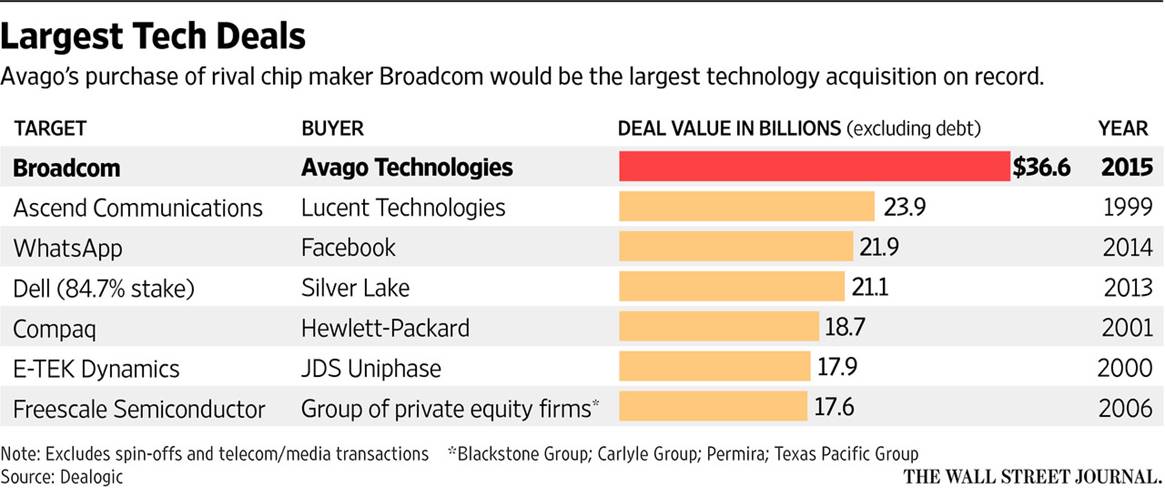

The value of a combined Avago-Broadcom would be approximately $77 billion. The new company (which is to be called Broadcom Ltd) will have annual revenue of approximately $15 billion. It's the largest tech deal ever, as shown in the chart below:

…..........................................................................................

A Company Built on Debt Fueled Takeovers:

Avago has used takeovers and mergers as an engine for

economic growth and increased market capitalization. Some analysts have

compared the company to Valeant Pharmaceuticals, a drug maker whose

meteoric growth has been powered by serial acquisitions. Avago's relatively short company history

is truly amazing and one for the record books.

·

In 2005, private equity firms KKR and Silver

Lake Partners acquired Agilent’s Semiconductor Products Group (SPG) for

$2.66 billion. (Agilent was spun off by

HP). In December of that year, Avago

Technologies was established, creating the world’s largest privately held

independent semiconductor company.

·

From 2007 to its IPO on August 6. 2009, Avago

acquired the fiber optic component and Bulk Acoustic Wave businesses from

Infineon (formerly Siemens Microelectronics) and then Nemicon

to complement its motion control product line. When AVGO went public in 2009, it seemed like

a modest player in the semiconductor industry with a market value of just $3.5

billion. But few anticipated its future

growth through debt funded deal making.

·

Since Avago became a public company in 2009, its

management team has pursued a half-dozen acquisitions. The biggest of which was

its $6.6 billion takeover of the LSI Corporation (formerly LSI Logic), a

networking and storage chip manufacturer, in late 2013. It was funded by a $4.6

billion leveraged loan which was ~70% of the price paid for LSI. The purchase price for LSI was more than six

times Avago’s cash on hand at the time.

·

Note that LSI had previously acquired Agere (formerly AT&T Microelectronics, then part

of Lucent Technologies, IPO in March 2001) which at one time had a market cap

of > $10 billion!

·

Early this year, Avago struck a $606 million

takeover deal for Emulex.

·

Aiding Avago’s acquisitions are several rare

factors, including a roughly 5% tax rate that comes from being based in

Singapore and ready access to low-cost debt financing. Note that Singapore is the company's

headquarters ONLY for tax reasons. Neither

the original company nor any of its acquisitions were ever based there.

AVGO went public August 6, 2009 at $15 a share. The

stock closed Friday at $148.07. That's

an increase of 987.13% and triple its value of December 2013. Evidently, Avago's aggressive acquisition

strategy has paid off big time for its shareholders.

…..........................................................................................

Other Debt Fueled Deals:

Avago's acquisition of Broadcom is not the only one taking

advantage of unparalleled access to cheap debt. FedEx has made a series of

acquisitions in recent months, most recently (April 2015) a $4.8 billion deal

to acquire TNT FedEx

executives cited the strong dollar, as well as signs of improvement in Europe,

as among the reasons for the deal. In January 2015, FedEx paid $1.4 billion for Genco Distribution Systems Inc., a

third-party logistics provider that specializes in the product-returns

business. In December 2014, it said it acquired Bongo International, a

provider of services for international e-commerce orders and shipments.

This

March, NXP Semiconductors NV agreed

to acquire Freescale Semiconductor Ltd.,

an Austin, TX based chip company (formerly Motorola Semiconductor), for about

US$11.8 billion in cash and stock. Freescale was taken private before the

financial crisis and, while it now has publicly traded shares, it’s 64% owned

by private-equity companies including Carlyle Group, TPG Group Holdings and

Blackstone Group. NXP, the former semiconductor arm of Koninklijke

Philips NV (earlier known as Signetics), was also

taken private and returned to the market in a 2013 IPO.

The NY Times reports

that Intel is close to clinching a takeover of FPGA chip maker Altera

for more than $15 billion, a person briefed on the matter said on May 29th

. It's yet another sign of massive

consolidation in the semiconductor industry.

Intel is expected to pay about $54 a share for Altera, whose

specialized chip designs would help Intel expand beyond chips for personal

computers, this person said. An agreement could be announced as early next

week, though this person cautioned that talks are continuing and might still

collapse.

S&P Rating Services - Large U.S. Takeovers are Bad for Credit Quality:

In a startling September 2013 report titled: The Credit

Cloud: Large U.S. Takeovers Are A Bad Omen For Credit

Quality, the analyst/authors wrote:

"Roughly half of the U.S. companies rated by Standard

& Poor's Ratings Services that have completed major strategic acquisitions

since 2000 now have lower (credit) ratings, and a third have ratings

that are at least two notches lower than when the deal was originally

announced. Numerous studies have been done in recent years suggesting that

corporate acquisitions frequently hurt shareholder value. Standard & Poor's

research suggests that major acquisitions also often contribute to a slide in

credit quality."

Apropos to the current free money Fed policies (bold font

added where deemed relevant): “Companies will often take advantage of strong

credit markets (ultra-low interest rates) to increase their financial

leverage to fund an acquisition, thus weakening their balance sheets and

credit metrics.”

According to S&P, another important contributor to the

long-term credit quality erosion of a significant number of acquirers, is that

“the rationale driving acquisition strategies is the desire to counteract

slowing or declining profitability as their business matures. However, large

scale acquisitions often do not produce sufficient benefits to offset the loss

of momentum in the acquirer's existing business. Large companies that have strong core growth

momentum usually have limited need for major acquisitions--and often avoid

them--because of their potential business and financial pitfalls.” We wonder if Avago has read the above report. Or maybe they're the exception to the rule

that credit quality and financial strength deteriorates after large acquisitions.

Victor on Economic Growth via Stock Buybacks and Mergers:

Historically, the growth of a company was to build a product

and grow it, so as to create greater long term value. Coca Cola was built that way. So were IBM, GE, and many other large

companies.

In the late 1960's, conglomerates became the vogue. Gulf & Western City Investing, Ling Temco-Vought (LTV), Litton Industries, ITT, and Teledyne

are just some of those companies of that decade. As you may have noticed, none are around

today.

The main problem for the conglomerate companies was the

inability to manage all the different areas of the business and to repay the

debt they created buying them through earnings. This was the way to show a

growth in earnings without building anything, merely buying companies with

creative financing to capture their earnings stream. This led to the "Junk

Bond" method of making money using “creative financing.”

The junk bond craze began in the late 1970's led by Michael

Milken, who worked at Drexel Burnham Lambert. The concept took off in the mid

1980's and accelerated from the mid-1990''s till 2000. From 1995-1999, the S&P 500 had the

greatest five year appreciation in history at +28.5% compounded. Financiers then got into mortgage backed

debt to help everyone own a house, whether they could afford to or

not!

Fast forward to today and we are back to debt to finance

acquisitions and share buybacks, due to the irresponsible and unpredictable

Central Bank policies of QE and ZIRP.

With the economic outlook so uncertain, few companies invest in their

own business as they don't see a good enough return on investment (ROI) to

justify the risk. Therefore, companies are buying back their own stock, often

with borrowed money (e.g. Qualcomm and Apple).

Some are buying other companies (as the Curmudgeon notes above) to

increase earnings and also to increase their company's stock price.

Certainly the goal of a CEO is to help increase the value of

the company's stock for its shareholders. The question is how they do it. Is it a "pyrrhic victory" they

seek, or a long term gaining market share and increased revenues and earnings

through stable, consistent economic growth?

GE under Jack Welch was a different company than GE under

Jeff Immelt, even though the name of the company is

the same. GE started in 1889 and has gone through many changes and

transformations since then. It took on a

lot more debt under Immelt that caused its financial

division to crater during the 2008-2009 financial crises.

The debt being created by the U.S. Federal Government is

mind boggling. The majority is held by

China at $1.2244 and Japan at $1.2237 trillion, as of the end of February 2015

(Japan now holds more U.S. debt than China, as of April 15, 2015).

“The debt will

never be repaid, but inflated away," according to Dr. Pippa Malmgren who was interviewed by "Real Vision

TV" (subscription only).

Ms. Malmgren was special assistant to President George W

Bush and is currently President of Principalis. She

specializes in quantifying risks on geopolitics to markets. Her father Harold,

served in the Kennedy, Johnson, Nixon, and Ford administrations. She holds a PhD from the London School of

Economics. Dr. Malmgren has many credentials and high end contacts. Her book

"Signals" has received many accolades from noted people. When Malmgren

talks, she is not “whistling Dixie.”

Therefore, her remark that “the U.S. will not repay its debt" is a

monster statement from a former DC insider.

Dr. Malmgren says China knows the US will inflate the debt

away, and is shortening the maturity of its U.S. debt holdings to 2 year

maturities while also buying Gold.

Apropos to this comment, an explanation of these obvious

tactics from the movie "Under Siege: Dark Territory," goes

like this: In Guanghou China a chemical weapons plant

is posing as a fertilizer plant. The U.S. knows this. The Chinese know we know,

but make believe we don't know, and the Chinese make believe we don't know-but

know that we know. Everybody knows!"

The morale: as always, debt

will kill the goose!

If the U.S. debt gets inflated away the corporate sector

will feel the effects as well and cause markets to be deeply affected. Rates will rise, bonds, and stocks will

decline, and cash flow will be cut.

That's the worst of all worlds for the buyback M&A strategy of

today!

The National Bureau

of Economic Research (NBER) has done a number of excellent studies on debt.

For example, "Private

Debt Kills the Economy Too Much Government Debt Hurts the Economy … But Too

Much Private Debt Kills It," September 09, 2012. That paper analyzed 138 years of economic

history in 14 advanced economies. It

proves that high levels of private debt cause severe recessions. As summarized by Business Insider:

“Through a series of tests run on a sample of 14 advanced

economies between 1870 and 2008, Mr. Taylor establishes a link between the

growth of private sector credit and the likelihood of financial crisis. The

link between crisis and credit [i.e. private debt] is stronger than between

crises and growth in the broad money supply, the current account deficit, or an

increase in public debt. Over the 138-year timeframe Mr. Taylor finds crisis

preceded by the development of excess credit, as in Ireland and Spain today,

are more common than crisis underpinned by excessive government borrowing, like

in Greece. Fiscal strains in themselves do not tend to result in financial

crisis."

"The study shows that excessive private debt is a much

more accurate and consistent predictor of financial crisis than the amount of

public debt. However, high levels of public debt exacerbate the problems caused

by massive private debt, since governments which are already “in the red” have

little ammunition left with which to help out the economy.”

“The NBER study validates what Steve Keen has been saying

for years: excess private sector debt is the main driver of deep recessions and

depressions. And yet Ben Bernanke and all other mainstream economists literally

believe that the amount of private debt doesn’t matter and isn’t even important

to quantify.”

American Private Debt [was] 310% of Gross Domestic Product

in 2008. That was the highest since

1929, the last Great Depression when Private Debt was 240% of GDP.

Victor’s Closing

Comments:

This has happened over and over again through history yet

governments ignore it to stay in power. It’s politics as usual. Who will be blamed this time for the next

economic bust?

[Note that the 2008-2009 "mortgage meltdown" was

blamed on the banks, whereas it was our government’s decision to let Lehman

Bros fail just months after they saved Bear Stearns (via JP Morgan

buyout). The latter caused AIG to

believe Lehman would also be saved by the feds.

However, our government officials didn't do it and later blamed

unchecked “capitalism,” not themselves for the financial fallout.]

Corporate debt is a musical chairs game. You run up the

debt, cash out, and pass the debt onto the next CEO with a good luck wish. Ogden Nash summed

this up beautifully:

"Some debts are fun when you are acquiring them, but

none are fun when you set about retiring them."

Good

luck and till next time...

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development platform,

which is used to create innovative solutions for different futures markets,

risk parameters and other factors.

Copyright © 2014 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).