Historical

Bubble and Bust Pattern

By Victor Sperandeo with the Curmudgeon

The overvaluation of investment objects (AKA bubbles) has a very long history. They always end badly and violently. The decline after the bust starts, takes only 20% of the time of the appreciation.

If you recall, a typical historical bull/bear stock market cycle was four years up and one year down. The bear initially produces a huge swipe downward with its claws, but then eats you alive. It is short and swift.

A bubble is a function of price and is never a value dynamic. When the market is appreciating, because of the fear of "missing out on profits" regardless of the assumed reason for the appreciation, it is in a bubble and no one can be sure (other than a central banker) when it will burst.

Review of Current Stock Market:

It's been six years since the last major stock market low in March 2009 and 1244 days (from 10/3/11 to 3/2/15) without a 10% correction. The fundamentals have been steadily deteriorating for stocks, which were manipulated higher by every central bank in the world, and by companies buying back their own stock instead of investing the money in growing total earnings (not rising earnings per share by reducing the float).

GE is a recent startling example. It’s selling its

financial portfolio (its bank) formerly known as GE Capital. The sale and

repatriation of $36 billion overseas will result in GE paying $6 billion in

taxes. The company plans a $50 billion

stock buyback program and "up to $90 billion to be returned to

shareholders over the next few years."

That boosted GE's stock price +11% on Friday. But does that really help the company?

Does shrinking the company help the economy?

Note that buying GE common stock at these levels is

certainly not "buying low," even if it looks good in the short run.

Indeed, it will be a smaller company in the guise of raising the share

price. I've repeatedly said that

burdensome regulations are killing the banking business so the spin-off of GE

Capital might be good for GE after all.

Stock Market Valuation:

Let's look at U.S. stock valuations vs. GDP growth.

· The S&P 500 12 month trailing earnings had a P/E one year ago of 18.12 (x's earnings) and today it's 20.55.

· The S&P 500 industrials P/E was 18.96 one year ago and today it's 21.40 (as per 4/13/2015 Barron’s).

That's in the context of real GDP increasing by only 2.39% from the previous year and 2.22% the year before. First quarter GDP is likely to be flat to down this year.

If you recall, all the P/E projections were supposed to be declining due to "increasing earnings" (which imply increasing GDP growth). The calls were for a P/E of 16 on the S&P indices. That projection was largely based on the Congressional Budget Office (CBO) estimates of GDP.

In the CBO February 2014 "Budget and Economic Outlook," the projection was for a 3.1% GDP increase for 2014 and 3.4% for 2015. That was way off the mark! 2014 GDP was 2.39% and this year the projections by the Fed are as low as 2.6%. [As the Curmudgeon and I have repeatedly stated, reported real GDP is overstated due to inflation being significantly higher than reported by the government.]

Meanwhile, the Fed may put off the first interest rate

(Fed funds) increase in nine years, because economic growth is fading. Under those conditions is it logical for

P/E's to expand?

Here are some additional facts of interest:

· Calls on S&P futures two months out, and 10% above the market, trade for $17.50.

· Yet puts 10% below the market two months out are $525.00.

That is rare indeed, and shows the many investors are worried about a market decline. Although money managers want to be long to not lose performance and thereby increase AUM in a rising market.

Hard or Soft Landing?

It's not going to be a "soft landing" when the brightest, most politically correct men in the investment business are very cautious. JP Morgan CEO Jamie Dimon and ex-PIMCO co-CEO Mohamed A. El-Erian are indirectly talking about financial bubbles. I certainly agree!

Mohamed El-Erian has his "own money invested mostly in cash" as per an interview titled: "Life after PIMCO: Mohamed El-Erian on economics, politics and his hope for a Sputnik moment." by Margot Roosevelt. In that interview, El-Erian says: "…most asset prices have been pushed by central banks to very elevated levels....there is a massive gap right now between asset prices and (economic) fundamentals."

El-Erian is writing a book on Central banking with a working title of "The only game in town: The rise and Possible Fall of Modern Central Banking and what it means to you."

I would add another game: monopoly, which is more transparent than central bank monetary policies.

Jamie Dimon, CEO of JP Morgan/Chase bank discussed the consequences of bubbles without mentioning the word in today's Financial Times (on line subscription required).

Dimon's timely message about financial fragility:

".....he warns that the next crises will see the banking sector no longer able to respond, sapped of flexibility by years of tightening regulations."

He ends by remarks that should spark the reader to take a bigger position in gold...

"The next one (financial crisis) will be different and Mr. Dimon has suggested that when it comes banks like his will not be organizing a rescue mission. If he is unable, and governments unwilling, the next panic could find ordinary investors well and truly on their own."

This is truly a "come to Jesus" comment by Dimon. Not only do we have a huge bubble, purely fabricated, but a warning that the "Fed Put" will be gone when it's needed the most (during the next recession). His point is that the U.S. government now has put itself into a position that it can't and won't do another "TARP."

Conclusions:

Markets that form into bubbles are not based on fundamentals, but on "mass psychology." We suggest readers study "The Crowd: A Study of the Popular Mind," by Gustave LeBon, rather than "The Intelligent Investor" by Ben Graham.

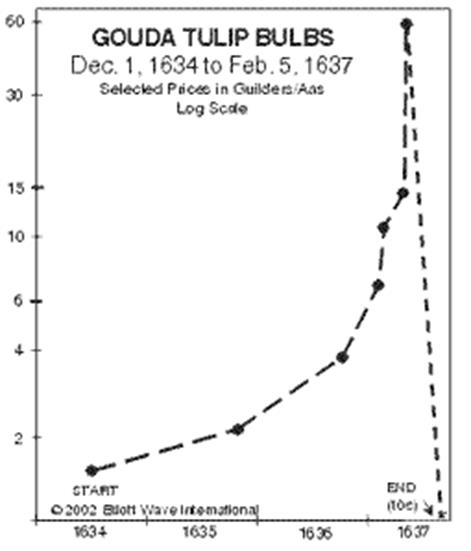

One of the most famous bubbles was the Tulip Bulb mania in 1637, which was

explained very well in Charles Mackay's "Extraordinary Popular

Delusions and the Madness of Crowds," first published in 1841. Mackay only devotes about seven pages to the

Tulip Mania, but his account provides an excellent perception of the

event. During that mania

"speculators from all walks of life bought and sold tulip bulbs and even

futures contracts on them." The end

was not pretty as depicted in the chart below:

Here's a great Tulip Mania quote and a comment on same by Jarod Kintz:

“My favorite flower is the tulip. I’m crazy like

Holland about them. I’ll even pay as much as $1,637 for one.”

― Jarod

Kintz, “At even one penny, this book would be

overpriced. In fact, free is too expensive, because you'd still waste time by

reading it.”

Is the current stock market in Tulip Bulb mania territory? Hedge fund manager Boris Marjanovic clearly thinks so - This Stock Market Bubble Will Burst Like An Overinflated Balloon.

We’ll let the reader be the judge.

Good luck.

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2014 by the

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).