High

Valuations for IPOs and Private Tech Firms Imply This Time is Different

By the Curmudgeon with Victor Sperandeo

Where's the Bubble Now?

Did you buy the New Year’s dip? If not, you're missing out on yet another V

shaped bottom - with a sling shot up move to new highs. That's guaranteed! Or

maybe not?

For quite some time we've opined that the stock market has

been manipulated. We can't believe that

the big institutional players and hedge funds hang on every Fed word spoken or

ECB pledge to "do whatever it takes," while not really doing

anything. History shows V shaped bottoms

are very rare, yet they've occurred regularly in the U.S. stock market since

the October 2011 (mysterious) bottom. That's not how markets work! There is usually basing or a testing of the

lows before a solid advance to new highs.

A manipulated market is not a bubble or Tulipomania. It's something more pernicious, which we've

discussed many times in previous Curmudgeon posts (based on anecdotal

evidence).

That said, we don't think that all stocks are in a

bubble. But we do believe that many tech

stocks are in a bubble and that almost all tech IPOs/private companies are

in huge, inflating bubbles if they are in these areas: "cloud

(computing & storage), social (media/networking), mobile

(apps/games/e-commerce), and big data (analytics)."

2014 was a banner year for IPOs:

According to research firm Renaissance Capital,

2014 measures up as the most active year since the turn of the century with 273

U.S. IPOs through December 17th. The $85

billion in IPO proceeds marked a 55% increase from a year ago thanks largely to

the $22 billion raised by Chinese e-commerce giant Alibaba.com.

With 293 companies going public, 2014 saw the most U.S.

IPOs since 2000, when there was a dot-com boom. The IPOs raised $95.9 billion,

which is also the greatest volume seen since 2000, when $104.6 billion was

raised, according to Dealogic.

Technology was the sector that saw the most volume, partly

due to Alibaba, with 57 IPOs raising $39.3 billion. Healthcare saw the most

IPOs, with 107 companies going public in 2014, due to a biotech boom. Finance

also came in strong, with 45 IPOs raising $17.7 billion.

David Ethridge, Sr. Vice President and Head of the Capital

Markets Group at NYSE Euronext, said, "Nothing is really

threatening investor confidence right now."

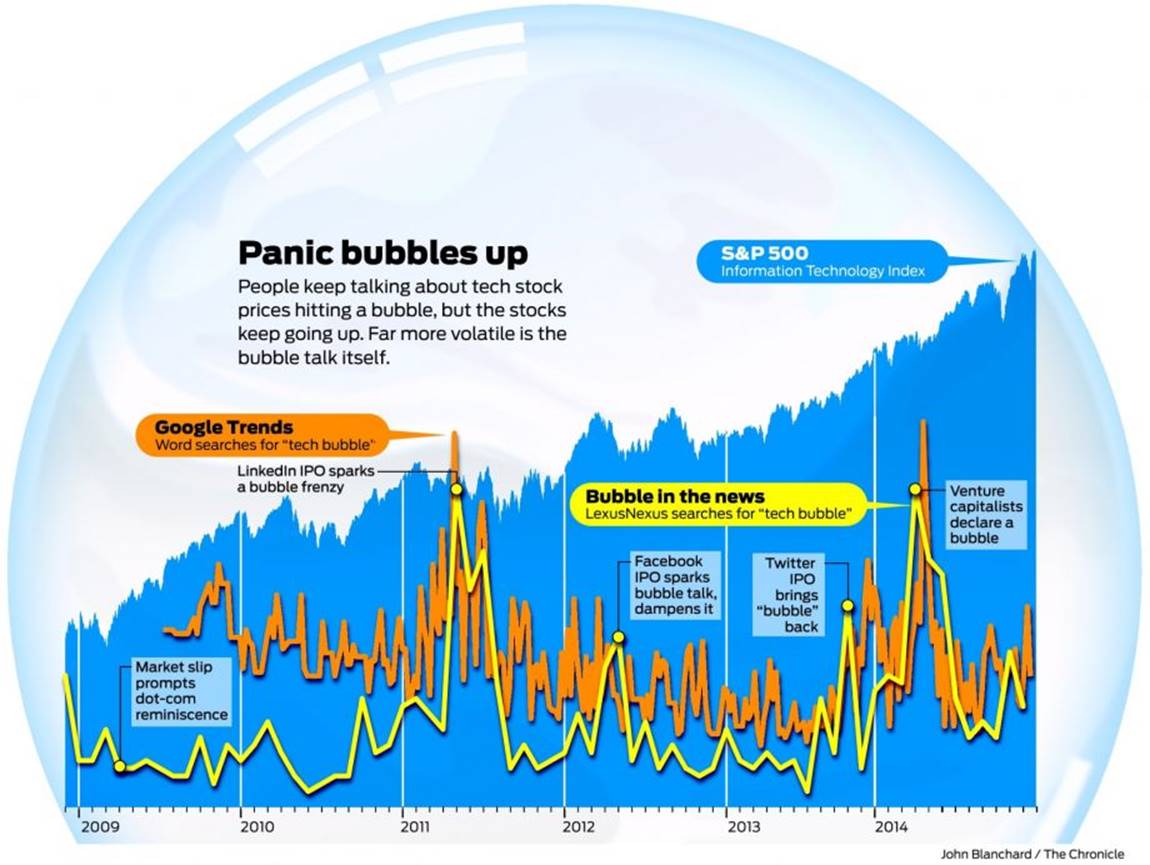

SF Chronicle Bubble Talk Study:

The SF

Chronicle tracked mentions of the phrase “tech bubble” both

in news media and Google searches during the past five years and found that

tech bubble anxiety tends to increase around major IPOs and acquisitions. The newspaper found that such chatter has

little to do with broad tech stock performance.

In the first few months of 2014, major tech companies went

on a buying spree. Google and Facebook announced deals worth more than a

combined $24 billion, scooping up high flying companies like Oculus VR (virtual

reality), WhatsApp (mobile messaging) and Nest (connected

thermostat).

Bubble chatter reached the levels surrounding LinkedIn’s

2011 IPO. A tech sell-off then hit Wall Street, and prominent venture

capitalists sounded the bubble alarm. Marc Andreessen tweeted that it was “the

weirdest tech bubble ever.” Greenlight

Capital’s David Einhorn sent a letter to clients that he was betting against

tech stocks. Twitter co-founder Biz Stone countered that there is no tech

bubble. Really?

Yet the S&P 500 Information Technology stock index

outperformed all popular market indices, closing 20% higher in 2014.

Barron's/Bates Research Study:

Barron's (on-line subscription required) asked Greg Kyle,

a senior securities analyst at Bates Research Group in New York, to do a study

which analyzed 80 Internet and technology infrastructure companies that have

gone public in the past three years. They carry a collective market value of

$380 billion. Fifty-five of them, or 69%, are posting losses.

The total operating profit of today’s 80 newly public

companies was $1.6 billion in the most recent quarter, though it’s important to

note that Facebook (FB) accounts for the bulk of those profits. Exclude

Facebook, and the companies’ operating profit totals $178 million.

As of September 2014, the median late-stage venture-capital-backed

company was valued at $250 million1, a record high and far larger

than in the bubble days, when the median private-company valuation peaked at

$89 million.

1according to Dow Jones Venture Source

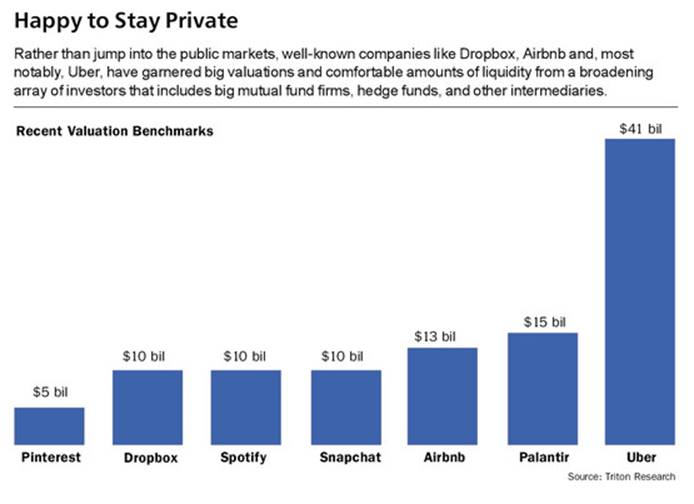

Private Firms worth $1 Billion or More:

There are 60 private companies that carry valuations above

$1 billion, according to Bill Hambrecht, a pioneer in technology IPOs and the

founder of WR Hambrecht - a San Francisco–based technology boutique.

“Those 60 companies would have been public in the ’90s,” Hambrecht said, citing

the new start-up trend to stay private for a longer period of time.

Jacques

Financial says there are nearly 70 worldwide startups now worth more

than a billion dollars. Adjusted for inflation, that's twice as many as during

the original tech bubble in 1999 and 2000.

VentureSource says there are 48 VC-backed firms in

the U.S. that are worth $1 billion or more.

That's compared with 10 at the height of the dotcom bubble. According to Venture Source, venture capital

firms raised more than $32 billion in 2014, up 60% over the prior year.

Here's a very revealing chart on the most expensive

U.S. privately held companies:

China Joins the Private Tech Equity Party:

As noted above, the mega Alibaba IPO fetched $22

billion. There are more Alibaba

wannabe's in China's IPO/private equity pipeline.

Last week, Chinese smartphone maker, Xiaomi,

officially became the world’s priciest startup with a round of funding that

valued the company at $46 billion. Only Facebook fetched a higher valuation

when it raised money from private investors in 2011. Xiaomi's phone is only sold online,

eliminating the middleman and thereby keeping the phone cost low (about $300

for a smartphone). Marketing was nearly all word of mouth.

Wanda E-commerce, which hopes to position itself as

a rival against Alibaba, has raised one billion RMB (about $161 million)

in funding from investment funds Shengke Limited and Hong Kong Xu De Ren Dao

E-commerce Investment Co. Wanda E-commerce says this quadruples its valuation

to 20 billion yuan (about $3 billion).

Curmudgeon's Analysis and Assessment:

For sure, private tech companies are benefiting from a

giant pool of money flooding into Silicon Valley as VC's and institutional

investors search for returns amid near-zero interest rates. The trouble is most

of those companies don't make any physical products but have captured the

interests and imagination of venture capitalists, private equity firms, angel

investors, and even mutual funds! Many of them are "one trick ponies,"

with only one product or service and no business plan to diversify.

Today, many more institutional investors are buying into

private technology firms, alongside VC funds. Unlike in 2000 the firms they

invest in already have scale (e.g. Uber’s gross sales are expected to hit a $10

billion annual rate by late 2015, according to the Economist.)

The bubble in private firms could have ramifications for

everyday investors as well. Traditionally, startups were exclusively funded by

venture capital firms, but 2014 saw an increasing number of mutual funds join

the start-up funding frenzy by making private investments in many early stage

tech companies.

Commenting on the new tech bubble, a revealing Economist

article is titled: Frothy.com

"A banker warns that successful funds’ recent run of

profitable exits is encouraging them to take “lottery ticket” bets. Among the

most recent tech firms to debut on stock markets with huge share-price “pops”

are Lending Club, a peer-to-peer lending platform, and New Relic and

Hortonworks, two “big data” software firms."

Even the venerable Wall Street Journal acknowledged

the tech start-up bubble in an article titled Start-up

Values Set Records.

Adjusted for inflation, the current roster of 70 “billion

dollar” startups globally is nearly twice as large as the number during the

boom years 1999 and 2000, according to the article.

Surveying the unprecedented valuations in the private

market, “I have trouble drawing a parallel,” said Ted Schlein, a general

partner at venture-capital firm Kleiner Perkins Caufield & Byers,

adding that his firm is trying to exercise “aggressive restraint” as it looks

for new investments.

Many start-up companies, like messaging service Snapchat

and online scrapbooking site Pinterest, have barely started making

money. Investors are betting those companies can capture audiences that will

eventually translate into big money, à la Facebook.

Perhaps, more astonishing than the start-up valuations was

how fast they were achieved. In November, investors paid $1.2 billion for a

stake in Uber Technologies Inc. That valued the five-year-old

car-hailing service at $41.2 billion - almost 12 times the price set by venture

capitalists last year. The valuation of Pure Storage Inc., a vendor of

data-storage equipment, tripled to $3 billion in April after less than a year. Slack

Technologies Inc. was valued at $1.1 billion in October only a year after

releasing its popular workplace-collaboration tool which they refer to as:

"a platform for team communication: everything in one place, instantly

searchable, available wherever you go."

Such valuations in private, early stage companies are in

tulip mania territory, IMHO. There's more (indirect) evidence of the Silicon

Valley Tech Start-up bubble in this article: Sand

Hill Road2 office sale may set new national price record.

2Sand Hill Road in Menlo Park, CA is home for

most VCs in Silicon Valley.

Meanwhile, VCs won't fund traditional engineering

companies that make real products, e.g. semiconductors, modules, circuit cards,

network/test/storage equipment, compute servers, or other hardware. Today's mantra for IT is "run open

source software on commodity hardware" wherever possible and

"software defined networking, storage, and data centers." Or use cloud resident "software as a

service." And remember that there's

a (mobile) app for everything!

In summary, 2014 was the year tech sector (software and

service) start-ups went ballistic and into hyper-drive mode.

Victor's Comments & Key Messages:

The event of high/over valuations with perceived new

inventions and innovations are present in some form in almost every bull

market. For example, in the 1920's

"auto companies" were the "Dot Coms" of that decade.

Hundreds of auto companies came and went.

Speculation is part of capitalism (i.e. economic freedom)

and failure is helpful to the end result of gleaning out the worthy

survivors. The process should educate

those who invest to do diligent research and act prudently. They should also limit exposure and potential

loss on any one investment.

The value and price of an IPO is all psychological. The sizzle often entices institutional

investors who may get stuck with a big loss (e.g. the Facebook IPO). This is

obvious, as the company founders and insiders that raise money on overvalued

start-ups usually cash out of 10%+ of their shares on the IPO.

Most traders are not in an IPO for the long term, but for

the initial market move upwards. The current owners of these stocks are mostly

sellers at some point. They're certainly

not Warren Buffett types.

With this is mind you can understand why stocks go down

faster than they go up. Cashing out is easy, as the stocks were bought to

sell - not to hold. Profit, while it exists, is the indicator of the buy/sell

decision process. Let's look at a

gambling analogy.

Like a run at a dice table, the winning player continues

to roll the dice until the roller craps out. A 20 minute run is very profitable

indeed, accompanied by lots of yelling, cheering, and screaming from the people

at the table. At the point when the roller ends his streak, the table becomes a

ghost town and everyone leaves as the game is over.

This is the trading model of what are now called

"Social Media" stocks, as no real assets exist. The model

calls for giving an idea away for free to users, and then "peddlers,"

acting as advertisers, hope to sell products to the users of the free

offer. If the economy turns down and

people stop buying, the peddlers stop advertising and the company dies with

virtually zero assets to sell.

Nothing will be more sensitive to the success of such

"advertising for revenue" companies than the economy. Marketers (like

politicians) have a way of rationalizing why they are never wrong and why you

should never sell a stock - a founder’s Holy Grail.

In the late 1960's and 1970's it was the "nifty

fifty" - large cap growth stocks (traded on the NYSE) that were said to be

immune from economic cycles ...and would always grow (even in a

recession)! Stocks like Polaroid,

Eastman Kodak, IBM, International Flavors & Fragrances, Avon Products, S.S.

Kresge, Sears, Digital Equipment, Xerox, etc.

The long bear market of the 1970s that lasted until August 13, 1982

caused valuations of the nifty fifty to fall to low levels along with the rest

of the market, with most of these stocks under-performing the broader

market averages.

Permit me to digress with a true story that has an

important message for those involved in today's hot IPOs.

In 1971, I started a stock options firm called "Ragnar

Option Corp." (Ragnar was a character in Ayn Rand’s novel Atlas

Shrugged). We became extremely

successful and in 1973 (a bad year for most in the stock market) we had one of

the few Wall Street Christmas parties. We made 600 T-shirts with Ragnar on the

front and back with over 500 people in attendance they were all gone. The crowd was so large because we hired the

famous Motown girl group "The Shirelles," which had major successes with their #1 hits

"Tonight's the Night" and "Will You Still Love Me

Tomorrow." Their general manager

and announcer ("Ronnie") began by saying something that has stuck

with me as somewhat of a guide to actions:

"Have a time, while you got the time, cause time is

running out." Those words should be on the minds of those who buy and own

the stocks that are discussed in this week's Curmudgeon post. The bottom line is to enjoy the ride while it

lasts…before time runs out!

Till next

time......

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2014 by The

Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).