2014

Recap and a Look Ahead to 2015

By Victor Sperandeo with the Curmudgeon

Introduction:

Victor briefly recaps the markets and suggest what we

might expect in this new year. The

Curmudgeon reflects on the biggest surprises of 2014:

·

50% drop in crude oil prices in last 6 months

·

Much lower (rather than higher) global

intermediate and long term interest rates

·

Incredibly disappointing global economic growth

- 5 1/2 years after the recession ended and with over $10T in bond buying by global

central banks (that's money being created out of thin air) since then.

·

Banner year for mergers and acquisitions with ~3.5

Trillion worth of deals- best in 7 years

·

Gold prices failed to advance, despite so many

geopolitical risks and central bank money printing.

·

SPE cyber-attack was a watershed event for

corporate/government IT departments and poses a future threat to critical U.S.

infrastructure

Victor’s 2014 Recap:

Stocks:

The year ended up in for the sixth year in a row. That was the second longest period of up

years since the creation of the S&P 500 in 1926. [The longest was the bull market of

1982-89].

The primary reason for this move was of course the Fed. It

is mentally numbing to believe the Fed is keeping rates at zero going on

"7 years" with a balance sheet rolling over on $4.5 Trillion dollars

vs its 2009 balance sheet of only $800 billion. Not mentioned is the huge

increase in repo's adding to the money supply, and off budget spending, while

not seeing the elephant in the living room.*

*A metaphorical idiom for the obvious truth being ignored.

So this increased distortion, due to malinvestment, expands

the risk greatly when the market declines. What was the "exchange

value" for the increase in risk based on the returns of 2014?

·

Nasdaq Composite +13.4%

·

S&P +11.4%

·

Mid Cap+ 8.2%

·

DJI +7.5%

·

Russell 2000 +4.2%.

The average is 8.9%, excluding capital gains taxes for the

average person.

This bull market is quite old. We are now at 1182 days since the last

correction of 10% which ended (mysteriously) on October 3, 2011.

Meanwhile the gross debt went from $10.8 Trillion to $18.0

Trillion, or an average of $1.2 Trillion per year since 12/31/08.

Lastly, note that we are at the same level of Fed Funds

rate (0 to .1%) as we were when the S&P 500 fell 40% in late 2008. That's when the world was teetering on an

event being compared to the Great Depression!

But we are now into the 6th year of economic recovery? Consider that interest rates have risen in

every recovery but this one. For

example, the 10 year T Note yields just a few basis points over 2%, while it's

50 year average yield is over 6%!

This reminds me of the movie "Moonstruck" where

Cher slaps Nicolas Cage, and says "snap out of it" to bring him back

to reality. The real Janet Yellen's view of the economy (behind the scenes) must be incredibly

horrible, as nothing in monetary policy has changed back to normal after 6.5

years of recovery.

Fixed Income:

The U.S government debt markets on 12/31/14 were yielding:

2 year 0.67%, 5 year 1.65%, 10 year 2.17%, and 30 year 2.75%.

Those low U.S. rates are greatly affected by foreign

interest rates which are trading at lows for the last 200+ years. The 5 year

German Bund trading is at a negative yield!

As are Swiss short term rates.

Bonds are trading on a "relative basis" to one another - not

the normal discounting premise of a recovery in GDP.

The spread of the 10 year TIPS (Treasury Inflation

Protected Securities) versus the 10 year U.S. Treasury Note was a mere 164

basis points low on 12/30/14. That's a

level not seen since 8/27/10, and my estimated average spread since 2010 is 250

basis, which reflects what the inflation rate will be in 10 years as dictated

by the U.S. government. Based on the 12/31/14 close, the spread was set at

1.69% which is the 10 year inflation rate projection.

Gold:

Gold was down 1.55% in 2014 after being down 28.6%% in

2013. Also note Gold was up 6.1% in 2012 and 9.5% in 2011 (after setting its

all-time high of $1,913.50 on August 23, 2011)

Two important points:

1. The Federal Reserve's custodian services for foreign

countries holding gold is at a low since 2000. Countries are wanting their gold

back, but the Fed has generally not delivered (e.g. Germany).

2. The Asia futures on gold (AKA paper gold) occasionally

trade at a discount to spot gold, which implies a shortage of deliverable real

gold.

Greece is a Wild Card:

The 1/25/15 elections in Greece will keep gold in its

basing mode. The election was called because the current President Antonis Samaras failed to be elected by parliament. If the

far left favorite Syriza Party wins they threaten to

pull out of the EU unless the banks write off 50% of the debt of Greece. That

would cause the other PIGS (Portugal, Ireland, and Spain) to want the same deal

and turmoil would likely ensue for the Euro.

A mouth dropping editorial in the Financial Times on

December 30, 2014 is titled "Voters are the Eurozone’s weakest link,"

by Gideon Rachman. Meaning democracy is a problem for

the EU Socialist Commissioners and their leader Jean-Claude Juncker

in Brussels. It's evident they don’t understand that people like to eat and pay

their bills, so consequently vote for these luxuries (?) which ruins the

"Austerity model" (read high taxes and government controls).

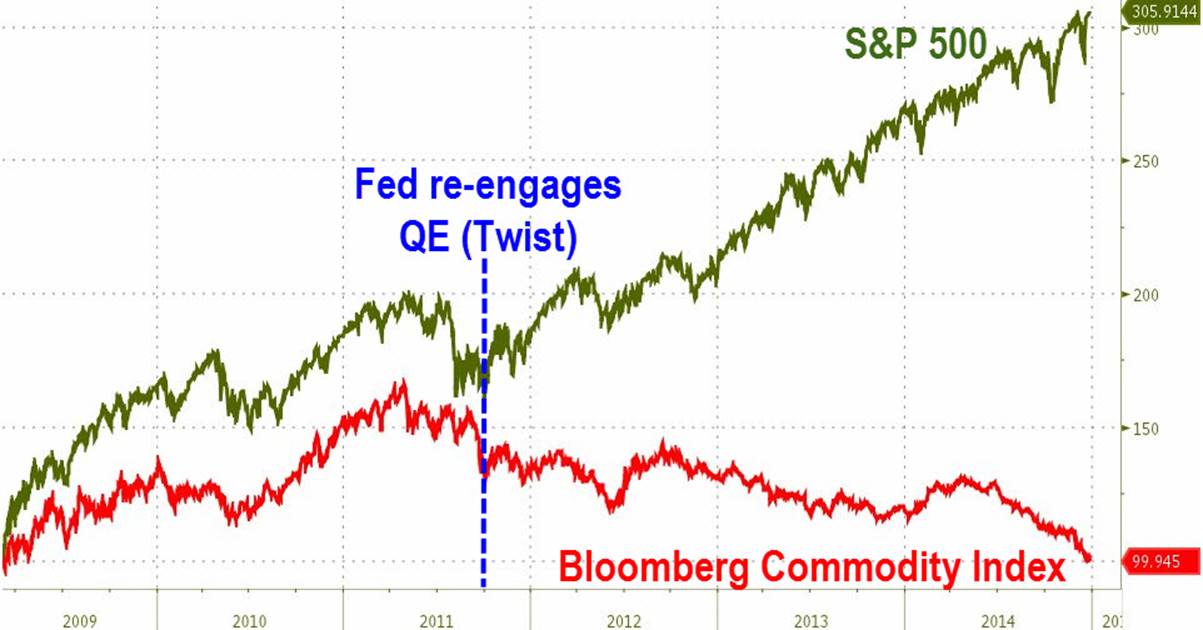

Commodities:

The Bloomberg Commodity Index is trading below the 2008

financial crisis low (see chart).

Commodities down four continuous years at a (-13.17%) compounded

rate using the Bloomberg CI (AKA DJ UBS CI) are clearly the distressed and possibly

undervalued? The recent decline in oil

prices has accelerated this downtrend.

I believe the commodities market is hostage to the current

fiscal and monetary policy of a rising dollar, suggesting weaker economies and

the assumption the U.S. will be first to raise short term interest rates (but

only to 0.25%)!

US Dollar:

The U.S. Dollar Index spot price closed at a new high on

12/31/14 at 90.27 - the highest monthly close since 91.17 in December

2005. It moved above that level on Jan

2, 2015 testing those 9 year highs. The "WSJ Dollar Index” made an 11 year

high going back to 2003 trading levels. Dollar strength is negatively impacting

commodity prices, as most commodities are priced in U.S. dollars.

1976-1980 Period was strikingly different:

It's interesting to compare interest rates in June 1976-to-July

1980. The Fed's discount rate went from

5.25% to 14.0%, and T-Bills returned a 10.34% "compounded" annual

rate from 12/31/76-12/31/80, while the U.S. Dollar index DECLINED from 107.05 to 84.65 (-21%) in the 6/76-7/80

period. The S&P 500 earned a "whopping" 1.14% compounded “inflation

adjusted return" pre-tax from 1976-1980.

The Economy:

The economy has grown in the calendar 2nd quarter at a

4.6% annual rate due to a bounce-back from the down calendar first quarter of

(-2.1%) which was attributed to extremely cold weather.

The third quarter growth of 5% is in large part from a

substantial and continued decline in oil prices and its products. That's an effective tax cut for the average

person which has increased consumer spending and goosed economic activity.

Looking Ahead:

The future looks good if you're long and a bull and poor

if you're a bear. The moral of the story, with so many our government leaders

lying, we must turn to some sage advice from the most enlightened of teachers,

Siddhartha Gautama aka "Buddha" who said:

“Now, Kalamas, don’t go by

reports, by legends, by traditions, by scripture, by logical conjecture, by

inference, by analogies, by agreement through pondering views, by probability,

or by the thought, ‘This contemplative is our teacher.’ When you know for

yourselves that, ‘These qualities are skillful; these qualities are blameless;

these qualities are praised by the wise; these qualities, when adopted &

carried out, lead to welfare and to happiness’ — then you should enter and

remain in them."

Or put into contemporary translated language:

"Believe nothing, no matter where you read it, or who said it, no matter

if I have said it, unless it agrees with your own reason and your own common

sense.”

Happy New Year and good luck in 2015!

Till next

time......

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and the

companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2014 by The Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).