Oil Price Crash is a Double-Edged Sword

By the Curmudgeon with Victor Sperandeo

Background:

The price of oil plunged by more than 10% to five-year lows on Friday after OPEC decided not to lower its output production target on Thursday. That occurred despite months of falling prices which have battered the budgets of many of the cartel’s member countries.

On Friday, NYMEX Jan 2015 Crude Oil futures settled at $66.15 a barrel and later traded at $65.99 - the low of the trading day. That was the lowest settlement for a front-month oil contract since Sept. 25, 2009, and it brought crude’s monthly losses to 18%, the largest one-month percentage decline since December 2008. For the week, oil futures declined nearly 14%.

The huge oil price drop pushed down energy shares, weakened oil exporters’ currencies and darkened the outlook for U.S. shale producers. It came against the backdrop of a 40% drop in the oil price since mid-June of this year.

Surging U.S. production, which is at its highest in more than 30 years, has combined with OPEC supplies that are well ahead of target and a pronounced slowdown in global demand to create a supply glut. On Thursday, Citibank analysts wrote in a report that global supplies currently exceed demand by about 700,000 barrels a day.

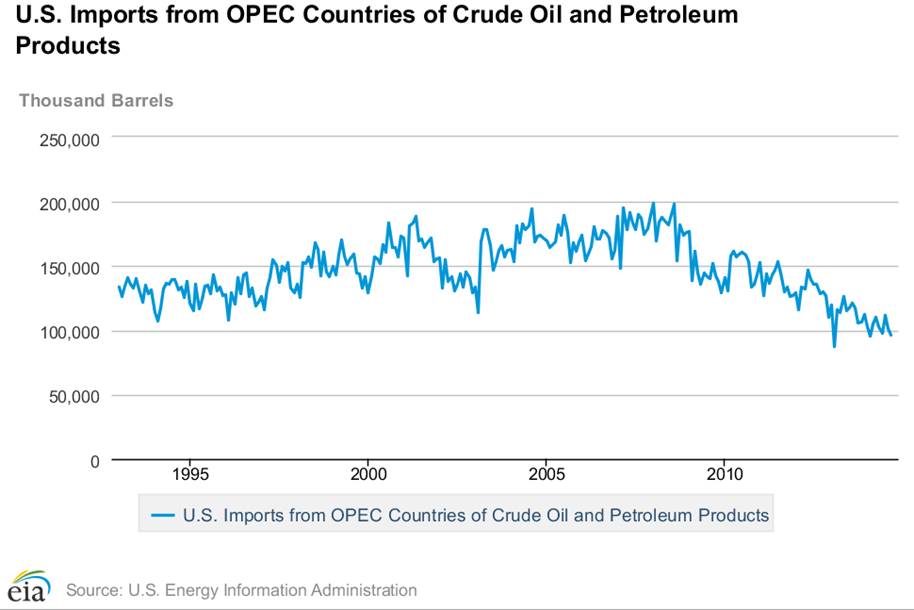

NOTE: The U.S .now imports only 40% of its oil from OPEC - the lowest since May 1985, according to Financial Times analysis of US Department of Energy data. At its 1976 peak that figure stood at about 88%.

U.S. Imports from OPEC countries of crude oil and petroleum products is shown in the chart below. This table shows monthly U.S. imports from Jan. 1993 through Sept. 2014.

OPEC's New Policy: Let the Market Determine the Oil Price:

OPEC's decision to keep its output target unchanged marks a big departure from the cartel’s traditional policy of seeking to prop up prices through production cuts. It suggests that OPEC - especially its largest producer and effective leader, Saudi Arabia - hopes to test the fortitude and staying power of U.S. shale operators and gauge how lower prices might affect output growth.

In its final communique from Vienna, OPEC stated it would maintain output levels in the interest of “restoring market equilibrium.” That's a clear sign it believes the cure for the oversupply is a lower oil price.

The OPEC statement echoed comments by Ali al-Naimi, Saudi oil minister, who said before the meeting that he expected the market “to stabilize itself eventually." When is anyone's guess.

“OPEC faces its greatest threat since the early 1980s,” said Bhushan Bahree, an OPEC analyst at market research firm IHS, before their meeting.

Whither the U.S. Shale Oil Boom?

Oil companies could cut as much as $100bn of capital spending in response to the price drop, imperiling the U.S. shale industry and threatening much Arctic oil exploration. The shale sector has driven U.S. oil production to its highest level in more than three decades, but is now very threatened by oil's low price.

Analysts at Tudor Pickering Holt, the energy investment bank, warned that, with US crude at or below $70, “no basin is safe” from cuts in drilling activity. The Bakken shale of North Dakota and the Mississippian Lime region of Oklahoma would be among the regions bearing the initial brunt of the slowdown, they said.

“I wouldn’t call it a price war but it’s a very aggressive test for U.S. shale,” said Jamie Webster, analyst at IHS Energy, a consultancy. “It’s a new gambit for OPEC.”

Leonid Fedun, vice-president of

Lukoil, Russia’s second largest crude producer, told Bloomberg

that OPEC was trying to turn the US shale oil “boom” into a “bust” for

smaller producers.

Other high-cost sources of oil, such as Canadian oil sands, could be affected. Andrew Leach of Alberta University said that production of bitumen by mining was typically only viable at over C$50 per barrel, the current market price. He added: “If we see sustained low prices [for conventional oil] some oil sand projects will have to stop.”

Arctic exploration could also be hit if crude stays low. Mr. Fedun told Bloomberg he did not expect the development of oil reserves in the Arctic on a significant scale to happen within his lifetime.

Oswald Clint of Bernstein Research warned that the response would be similar to 2009, when non-OPEC capital expenditure, excluding acquisitions, fell by 16 per cent or $100bn after the oil price plunged from record highs.

The Winners and Losers:

In countries that are net oil importers, low energy/fuel prices are welcomed. For years, they've been likened to a tax cut in the U.S. Low oil prices boost economic growth by reducing energy/fuel bills and leaving consumers and companies with more money to spend on other things.

India and Japan are a clear winners as those countries import 90% and 80% of their energy needs, respectively.

Japan has very limited domestic energy resources and meets less than 10% of its own total primary energy use from domestic sources. It is the third largest oil consumer and importer in the world behind the United States and China. Up till recently, the falling Yen has masked the decline in oil, which is priced in dollars.

India's stock market has been soaring since oil prices started to nose dive this July. “The lower the prices, the better for us,” K.V. Rao, finance director at India’s third-biggest state refiner Hindustan Petroleum (HPCL) Corp., told Bloomberg. “We’re currently in a sweet spot,” he added.

While China has signaled tolerance for weaker growth as the government tackles corruption, pollution and debt, the economy needs stable oil prices for a true recovery. Despite holding the world’s largest shale gas reserves, China has remained dependent on imported oil, because progress on extracting fuel trapped in rocks has been much more difficult than expected.

However, OPEC's poorer member countries and other major oil exporters will feel the biggest negative impact. While low-cost oil producers with big foreign exchange reserves, such as Saudi Arabia, are willing to withstand a period of cheap crude oil, Venezuela, Nigeria and Iran need higher prices to balance their budgets.

Venezuela, which depends on oil for 95% of its export revenues, called for an emergency meeting of OPEC to address the steep slide in prices, a move that other members rebuffed in favor of the regularly scheduled meeting that took place this past week.

North Sea oil producers Britain and Norway face a drop in revenues that could balance out the positives of cheaper fuel.

The Russian economy, already hurting due to Western

sanctions over Ukraine and a plummeting Ruble, will weaken further if revenues

from oil exports continue to fall. Those

exports account for ~50% of state revenue.

“If oil prices were to stay in the range they are in now, we’ll see the Russian budget fall into deficit next year; that’s on top of the economic challenges they are already facing from sanctions and the decline in the value of their currency,” said Jason Bordoff, Director of the Center on Global Energy Policy at Columbia University in New York.

Falling oil prices also pose a potentially grave security challenge for Iraq, which is already struggling to finance its fight against the Islamic State through oil export revenues.

“Iraq has its own set of challenges with skyrocketing public expenditure requirements, large public payroll, and food and energy subsidies. They need to rebuild a dilapidated armed forces,” Professor Bordoff added.

Amrita Sen, analyst at Energy Aspects, said: “This is becoming a battle of [who has] the deep pockets and survival of the fittest.”

The Primary Cause of the Oil Price Decline:

We believe the main reason behind the oil-price collapse is a weaker global economy, which we pointed out in last week's CURMUDGEON post.

If global economic weakness continues, it will hurt the U.S. economy by reducing exports, employment and spending. That, in turn, could outweigh the economic benefits of cheaper energy and fuel.

At this stage of the economic cycle (5 1/2 years into a so

called "recovery"), the price of energy and industrial commodities

should be firm and steadily rising due to increased industrial demand (to

expand plant & factories and/or to build new equipment &

buildings). The opposite is the case

now, which shows how weak the global economy actually is. Ironically, global stock markets love it,

because central banks continue their money printing gravy train, which floods

the financial market with liquidity.

Victor's Comments:

The Dow Jones UBS Commodity Index is now down four years in a row at a (-12.34%) compounded annual rate - from April 29, 2011-to-November 28, 2014. However, oil has experienced a very different price pattern.

The West Texas Intermediate crude oil futures contract was actually up +7.87% from 2010 to end of 2013, based on the near term NYMEX crude oil contract. At the November 28th close of $66.30, it's down -32.74% net from the end of 2013.

Moreover, from June 16, 2014 (the near term high of $106.9), oil has dropped 38% in 165 days or about 6.9% a month. Price changes can happen fast and often do in commodities Many have forgotten, but the same is true for stocks (at least it was before the Fed and other central banks banned bear markets).

Aside from all the reasons stated by the Curmudgeon above, a primary reason oil has declined is due to the end of the "war premium." That premium was largely based on a potential Israeli attack on Iran over its nuclear build up. Such an attack would severely disrupt that countries oil exports and cause massive retaliation. There's also the possibility of ISIS commandeering oil fields in Iraq and Saudi Arabia which we've noted in a previous Curmudgeon post.

The estimated war premium ranges from $4 to $20 per barrel, depending on when the threat question is raised and what the nominal price of oil is at that time. The spread of WTI to Brent (oil) prices was a good guide to the war premium as the U.S. is a large producer of oil (and Natural gas) and thereby has less risk than Europe if supplies suddenly shrink. The spread was as high as $28 a barrel in late 2011. Today, it’s only $3.85.

When the Iran nuclear talks failed to reach an agreement by the November 24th deadline and were extended for seven more months, many believed that ended the threat of an imminent Israeli attack on Iran.

The logic is as follows: Israel would make the U.S. irate and U.S./Israel relations would hit a new low, if Israel attacked Iran while the latter's nuclear program negotiations were ongoing. If an agreement was reached that Israeli felt wasn't strong enough, a pre-emptive strike on Iran's nuclear facilities would be more likely.

Israel already suspects that the monitoring and verification procedures to be applied in Iran will be insufficient. Like many other countries, Israel doesn't believe that Iran really declared all its nuclear assets and activities. Based on its past non-compliance with international inspections, Israel is convinced that Iran will not agree to intrusive inspections at all sites within its territory.

With President Obama desperate for some positive legacy accomplishments, he will not stop the Iran talks. That puts Israel in a dilemma, but on hold regarding a pre-emptive strike on Iran's nuclear stockpiles.

Saudi Arabia is an arch enemy of Iran, because of the Sunni-Shia power struggle in the Islamic world. The Saudis want to weaken Iran's economy via a lower oil price. Iran needs high oil prices to support their bloated government budgets and popular subsidies. Without those, there'd likely be mass public protests and civil unrest.

Putin's Russia, of course, is not partying this weekend with oil prices way down and the Russian Ruble at a new all-time low vs the U.S. dollar. It's reported that Russia has budgeted oil at $100 per barrel to pay their bills. What will they do now with oil under $70 per barrel?

At current oil prices, Russia, Iran and others like Venezuela are in extreme trouble. For most of the industrialized world these countries are not being sympathized with at all. But there's a huge risk that no one wants to mention: people that are desperate do desperate things. Russia has 8,500 nuclear warheads. Would they sell some and to whom? Most people would say "no” but this is a very dangerous proposition.

With all the talk of deflation in Europe and Japan, the U.S. not meeting its 2% inflation target, the oil and commodity price declines, and so forth, governments have yet another excuse for more stimulus and central bankers may create more "free money." That would provide impetus for overvalued and extended stock markets to rise further.

Hey, what's not to like? We've asked before, but

can't resist asking again: What can

go possibly go wrong?

Till next

time......

The Curmudgeon

ajwdct@sbumail.com

Follow the Curmudgeon on Twitter @ajwdct247

Curmudgeon is a retired investment professional. He has been involved in financial markets since 1968 (yes, he cut his teeth on the 1968-1974 bear market), became an SEC Registered Investment Advisor in 1995, and received the Chartered Financial Analyst designation from AIMR (now CFA Institute) in 1996. He managed hedged equity and alternative (non-correlated) investment accounts for clients from 1992-2005.

Victor Sperandeo is a

historian, economist and financial innovator who has re-invented himself and

the companies he's owned (since 1971) to profit in the ever changing and arcane

world of markets, economies and government policies. Victor started his Wall Street career in 1966

and began trading for a living in 1968. As President and CEO of Alpha Financial

Technologies LLC, Sperandeo oversees the firm's research and development

platform, which is used to create innovative solutions for different futures

markets, risk parameters and other factors.

Copyright © 2014 by The Curmudgeon and Marc Sexton. All rights reserved.

Readers are PROHIBITED from duplicating, copying, or reproducing

article(s) written by The Curmudgeon and Victor Sperandeo without providing the

URL of the original posted article(s).